Three ways COVID-19 will cause economic divergence in Europe

- COVID-19 is not a ‘symmetric’ shock to Europe’s economy. The economic costs of lockdowns, and the continued social distancing measures that follow them, will be different across countries and regions. And some governments are better able to offset the costs of these measures than others – and to stimulate their economies once the virus is under control.

- We identify three ways in which COVID-19 will be a force for divergence. First, lockdowns in countries with larger outbreaks will last longer. France, Italy, Spain, and the UK have had the worst outbreaks in Europe. Most countries in Europe have imposed comparably stringent lockdowns – and for each month that they go on, around 3 per cent of annual GDP is lost. But lockdowns will continue until the number of infections has fallen to a low level. Our simulations suggest that this will take many weeks longer for France, Italy, Spain and the UK than it will for Austria, Germany and Poland.

- Second, through a new analysis of the impact of lockdowns on Europe’s regions, we show that regions in Southern Europe are likely to suffer larger and more long-lasting recessions than those in the north and east. The manufacturing and tourism sectors are hardest hit by lockdown measures, and tourism will remain limited even when lockdowns are lifted.

- Finally, Southern European governments are less able to offset the costs of COVID-19, and their higher debt levels will weigh on the recovery. We show that consumer confidence has been hit hardest in countries that have enacted less stimulus. And higher debt-to-GDP ratios will probably result in higher borrowing costs for governments. Consequently, with more tax and business revenues being used to finance debt, there will be less capacity for investment. Unless the EU’s fiscal rules are reformed, they will also require Southern Europe’s governments to rapidly cut debt, which will reduce growth over the medium term.

- Further economic divergence is bad in and of itself. But it will also make European politics even more fractious. Slow growth in some regions provides fertile ground for the far right and left, and undermines the appeal of the EU as a ‘convergence machine’.

- During the initial months of the COVID-19 crisis the EU’s richer countries balked at large outright transfers to the worst-affected countries. Now, the Franco-German proposal for a €500 billion 'recovery fund' has the potential to forestall further divergence, if sceptical countries in Northern and Central Europe can be persuaded to accept significant transfers to Southern Europe. Agreeing the details of the fund will be hard, and the sceptics may demand more money from the EU budget in order to sign up.

- The EU’s fiscal rules are too rigid, and mandate the reduction of debt even when economies are weak. Now is the time to reform them: the aim should be to stabilise debt levels once the pandemic is over, and to let growth reduce debt over time.

By agreeing a proposal for a €500 billion EU recovery fund with Emmanuel Macron on May 18th, Angela Merkel broke two rules of Germany’s EU policy: that there should be no common borrowing and no transfer union beyond the existing EU budget. The Franco-German proposal could be a historic step towards more fiscal integration in the EU, but the Northern European ‘frugals’, led by the Netherlands, will have to be persuaded not to whittle down the size of the transfers. So too will Poland and Hungary, who have handled the pandemic well, and will probably refuse to be net contributors to richer countries in Southern Europe. There is every indication COVID-19 will be a big force for further economic divergence within the EU, after a decade of weak growth and political turmoil. If the scale of transfers in the recovery fund are negotiated down by the frugals, the new fund will do little to offset the damage the virus will inflict.

As we noted in the first paper in this series on economic divergence in Europe, even before the pandemic struck, the bloc was failing in its core mission of promoting convergence in living standards across Europe.1 Enlargement had been a success, with per capita incomes in Central and Eastern Europe rising rapidly (though inequality rose too). But between the mid-1990s and 2008, Greece, Italy, Portugal and Spain failed to converge with the richer north-west of the continent, and after the euro crisis this gap widened. Now, there is every indication the south will suffer bigger COVID-19 recessions and weaker recoveries.

In this policy brief, we offer three reasons why the pandemic is likely to be both an asymmetric shock and lead to further long-term economic divergence between Southern and Northern Europe. Lockdowns have enormous economic costs and are likely to last longer in countries that have suffered worse epidemics, such as Spain, Italy and France, which means they will have longer recessions. More regions in Southern Europe are dependent on tourism and manufacturing, the sectors that are worst affected by lockdown measures, than regions in the north and east. Finally, Southern European governments are financially constrained by high debt, and therefore less able to safeguard jobs and businesses and to stimulate the economy when lockdown measures end.

We conclude with a discussion of European economic policy and the Franco-German proposal. The new fund would be a bold step in the right direction: common borrowing, based on the EU budget, with funds disbursed to the most affected regions and sectors. The size of the proposed fund is big enough to make a macroeconomic difference. But opposition will be formidable, and there is every risk it will be watered down – as the Franco-German proposal for a eurozone budget was. Berlin and Paris should stick to their bold proposal, and make clear that such transfers are in the common European interest. And whatever the outcome of the negotiation, the EU should revisit its fiscal rules, in order to allow governments to stimulate recovery once the pandemic is over, and to lower the pace of debt reduction in the medium term. A return to the austerity of the last decade would make the EU even more dysfunctional in the next.

Why some countries will have to maintain lockdowns for longer

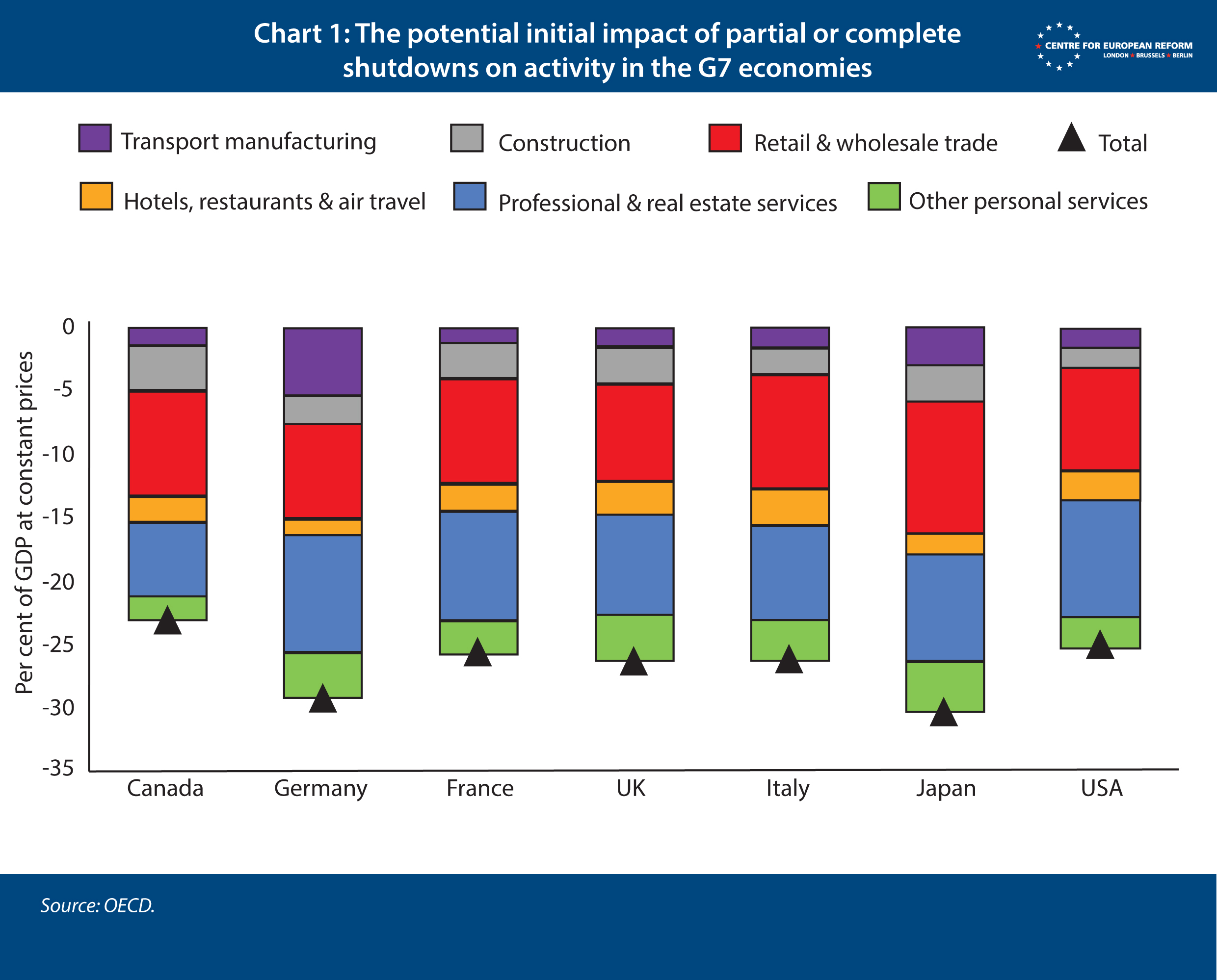

Lockdowns are intended to prevent people from interacting, so it should not be surprising that they entail enormous economic costs. The OECD estimates that economic activity has fallen by between a quarter and a third across the G7 (the largest developed economies, Chart 1). And the Banque de France reckons that every month France is in lockdown annual GDP will fall by 3 per cent.2

This apparent uniformity is because nearly all European governments (with the notable exception of Sweden) began by imposing comparably stringent lockdowns. COVID-19 outbreaks have been worse in Belgium, France Italy, Spain and the UK than elsewhere in Europe, as measured by deaths per capita. There are two views as to why this is the case. The charitable view is that their outbreaks happened first. The uncharitable view is that the worst affected countries were too slow to impose lockdown measures, despite outbreaks having already been observed in several Asian countries.

However, all European countries had ‘community transmission’ (as opposed to cases brought in by travellers) when they locked down, and extreme social distancing has proved to be the only way to reduce the reproduction number, R, below 1. If R is below 1, each infected person on average infects less than one other person, and the number of infections in the community falls. According to an index compiled by the Blavatnik School of Government at Oxford University, lockdown measures were similar across Europe at the end of April, apart from Austria, Bulgaria and the Czech Republic, which had already eased lockdowns somewhat at that time (Chart 2: the index goes from 0 for no containment at all to 100 for the strictest lockdown).

This does not, however, mean that all European countries will see recessions of the same severity. Countries that have had larger outbreaks will have to enact stringent lockdown measures for a longer period of time to suppress the virus. Because every month of lockdown results in a large hit to GDP, France, Italy and Spain will fare much worse than, for example, Germany or Poland.

Countries with larger outbreaks will have to enact stringent lockdown measures for longer to suppress the virus.

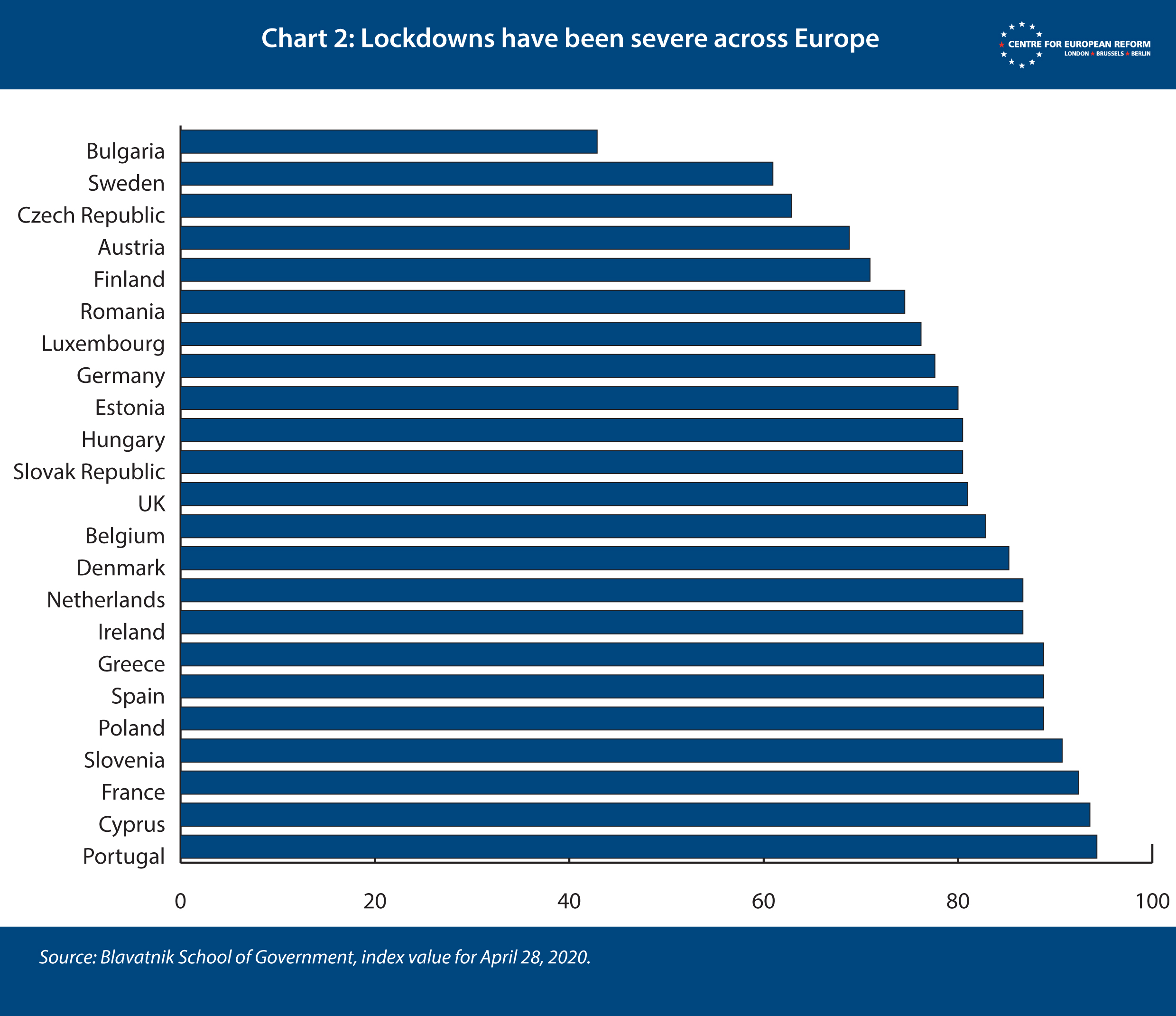

Chart 3 illustrates the results of a simple model that shows why this is the case. At the time of writing, most governments are considering easing lockdown measures, or have started to do so. But most easing will be slow and partial. Governments cannot simply lift all lockdown measures when R falls below 1 without risking a second wave. To get back to (near) normal, they must wait until the number of infected people has fallen to a level low enough that a test, trace and isolate regime can be effective in containing infections. These regimes require mass testing, so that the infected can be identified and isolated, and a contact tracing system, so that people they may have infected can also be tested and isolated. South Korea has shown that a test, trace and isolate regime can be effective, in combination with social distancing measures that are less draconian than full lockdowns. In a recent study, the ifo Institute in Munich found that Germany’s regime could cope with around 300 new infections per day, which is similar to the rate of new infections in South Korea (on a per capita basis).3

The chart makes a rough forecast of how long it could take for larger European countries to reach South Korea’s peak of infections per capita – a level at which a test, trace and isolate system has proven sufficient. The uncertainty in the data underlying the forecast means that the exact dates when countries hit Korea’s peak are probably wrong, but it suggests that countries with larger outbreaks will take many weeks longer to do so. With that health warning in mind, the chart shows that Poland, which has had the smallest outbreak among large European countries, will hit South Korea’s peak at the beginning of June; Germany will do so in mid-June; and Spain, France, Italy and the UK between the end of July and mid-August.

To make the forecast, we estimated infections per capita by multiplying deaths data by the upper bound of the consensus estimate for the infection-fatality ratio (IFR) – 0.8 per cent.4 We then moved the estimated infections per capita data back by one month, because it takes around that long for infected people to die from COVID-19. And we have taken the average rate of decline across our sample of countries since their respective peaks as the rate of decline in infections. This simulation is imprecise, because recorded deaths and the IFR are uncertain, and the rate of decline in infections may change. But several more weeks of lockdown means bigger recessions for Spain, Italy, France and the UK this year.

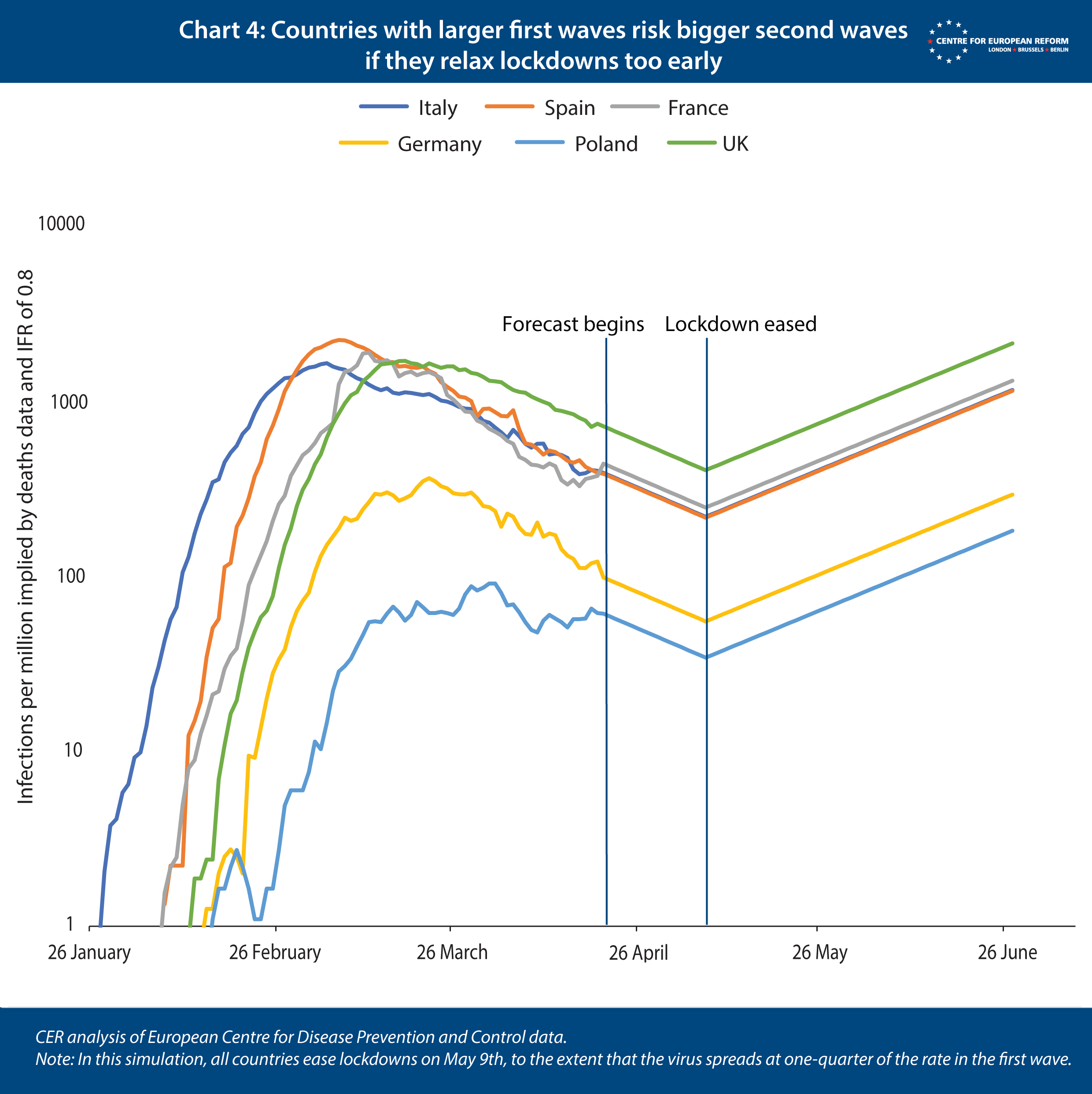

If countries with bigger initial outbreaks relax lockdown measures too early, they will have to be reinstated.

Moreover, if countries that have suffered from big outbreaks relax lockdown measures too early, their healthcare systems will be quickly overwhelmed, leading to measures being reinstated. Because the IFR is uncertain, we do not know for sure the share of the population that has been infected. But an IFR of around 0.5-0.8 per cent suggests that, even in the worst-affected countries, less than a tenth of the population has contracted the virus so far. That means that even countries with big first waves are likely to be far from herd immunity, and if they relax lockdowns too early they risk second waves that are larger than countries with smaller initial outbreaks. Chart 4 illustrates this by showing that the number of infections quickly rises to the peak of the first wave, even if countries ease lockdowns only partially.

In summary, countries that have suffered from larger outbreaks of the disease will have to maintain lockdown measures for longer than other countries, which means they face significantly longer recessions this year. As the next section will show, Spain and Italy have been unlucky: they had big first waves, and the structure of their economies means that lockdowns are more damaging.

Lockdowns impose larger costs on Southern Europe

Physical distancing between workers is easier for some businesses to manage than others. Office workers can more easily work from home, whereas factory, retail, hotel, restaurant and entertainment workers need to work together or in close proximity to their customers. Economic activity in European regions where more jobs are in manufacturing and tourism will be disproportionately affected by lockdown measures.

European regions with more jobs in manufacturing and tourism will be worst affected by lockdown measures.

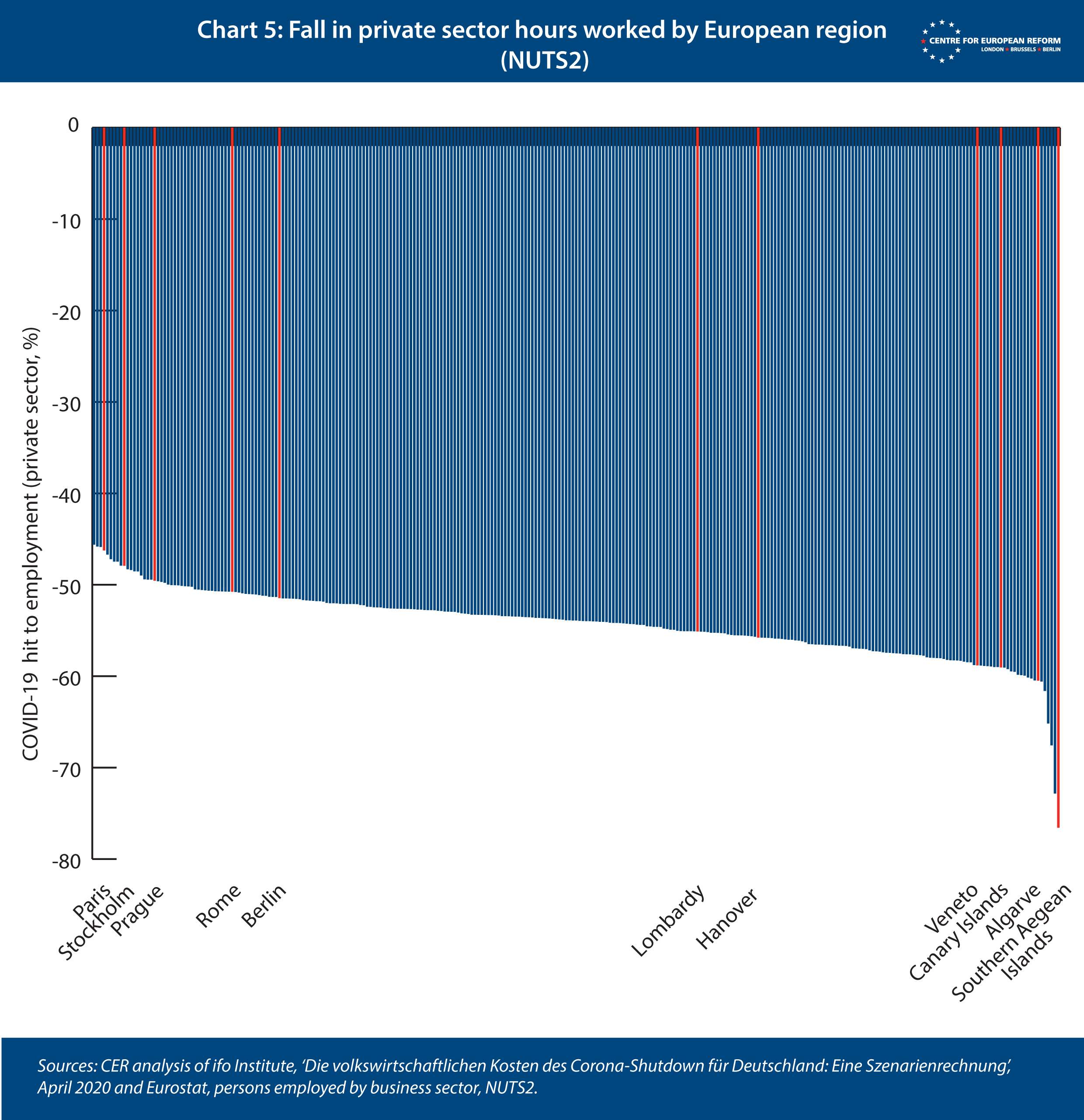

We do not have timely data on COVID-19’s impact on different business sectors. But the ifo Institute has made some educated guesses about activity levels across 63 sectors in a recent paper, and assumes that activity in manufacturing plants is down 80 per cent, there is no activity in hotels and restaurants at all, and business services are down 20 per cent.5 By applying their assumptions to Eurostat’s data on the share of regional employment by business sectors, we can see which European regions are likely to be hit hardest (Chart 5).

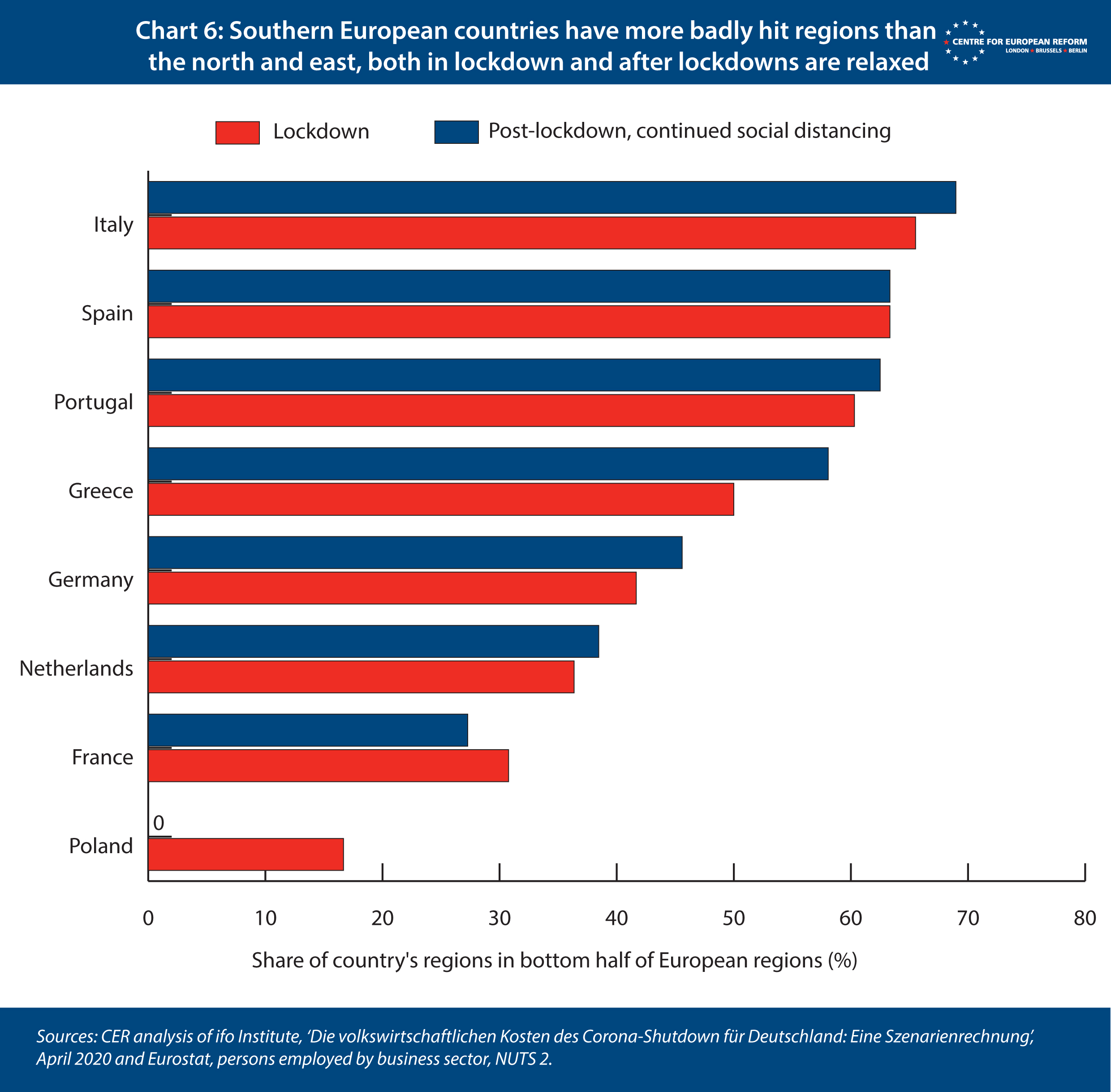

According to these assumptions, most regions have seen private sector activity fall by between 50 and 60 per cent. The precise size of that fall is uncertain, as it is based on assumptions, but the differences between regions are likely to be reasonably robust. As the chart shows, capital cities, which have larger business services sectors, tend to be in the upper half of the league table. Manufacturing centres such as Lombardy and Hanover are in the bottom half, while regions whose economies are dominated by tourism, like Greece’s Aegean Islands, are at the very bottom. Overall, Southern European countries – and Germany – have more regions in the bottom half than other countries, because they have comparatively large tourism or manufacturing sectors (Chart 6).

Even after lockdown measures are relaxed, the south is likely to fare worse than the north. The ifo Institute has also made some assumptions on activity levels between the lifting of lockdowns and the roll-out of a vaccine, with physical distancing measures still in place. An equal recovery is unlikely, because tourism will continue to be badly affected (tourists will stay away, wary of resorts crowded with people from across Europe), while manufacturing is more likely to rebound.

If tourists refuse to travel this summer, the recession will be far worse in the south than the north and east.

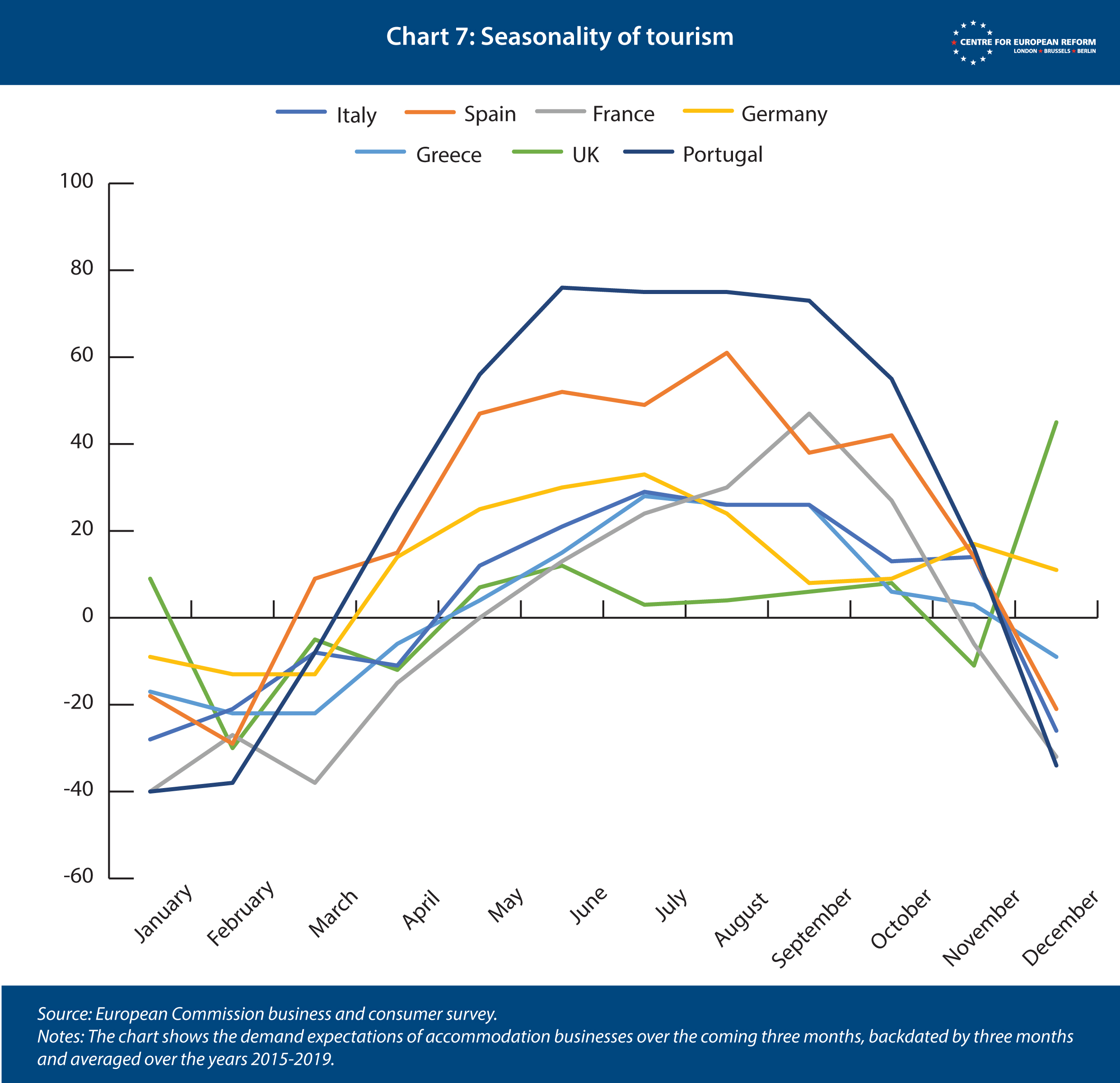

If anything, this regional analysis is likely to understate the scale of the hit. Tourism is, rather obviously, highly seasonal. But it is especially so in Southern Europe, because so many people take their summer holidays there: people tend to visit cities throughout the year. Tourism makes up between 7 and 12 per cent of Southern European countries’ GDP, according to the OECD, and the majority of that income is received in the summer months (Chart 7). If, as seems likely, tourism is restricted by social distancing measures, or tourists refuse to travel this summer, the recession will be far worse in the south than the north and east.

Spain and Italy were unlucky to have had the earliest, and hence biggest, outbreaks in the EU, which will entail longer lockdowns and larger recessions. And the structure of their economies means that they, alongside Greece and Portugal, will fare worse than Northern and Eastern Europe until the pandemic is over. These countries were also hit hardest by the euro crisis, and as we show below they have less fiscal firepower to respond to the COVID-19 shock.

Southern Europe is less able to bear the cost of the pandemic

Countries with higher public debt at the start of the pandemic – and those with lower growth potential – are less able to support the private sector during lockdowns and the continued social distancing measures that succeed them. There are four ways in which that may cause economic divergence in the long run.

Less indebted countries are better able to protect their economies. The effect of this is already visible.

First, countries with higher public debt may be more reluctant to provide support to businesses and workers. This would not only harm their economies, it would also tilt the single market in favour of those countries that provide more subsidy to their businesses through this crisis. Currently, as countries have scrambled to put together support packages, the relationship between debt and the scale of support is not entirely clear. Some measures of fiscal stimulus show a clear relationship: Germany is spending a lot more than Italy. But other measures, which include liquidity support such as guarantees and tax deferrals, and changes to interest rates, show a weak relationship between public debt and the scale of support.

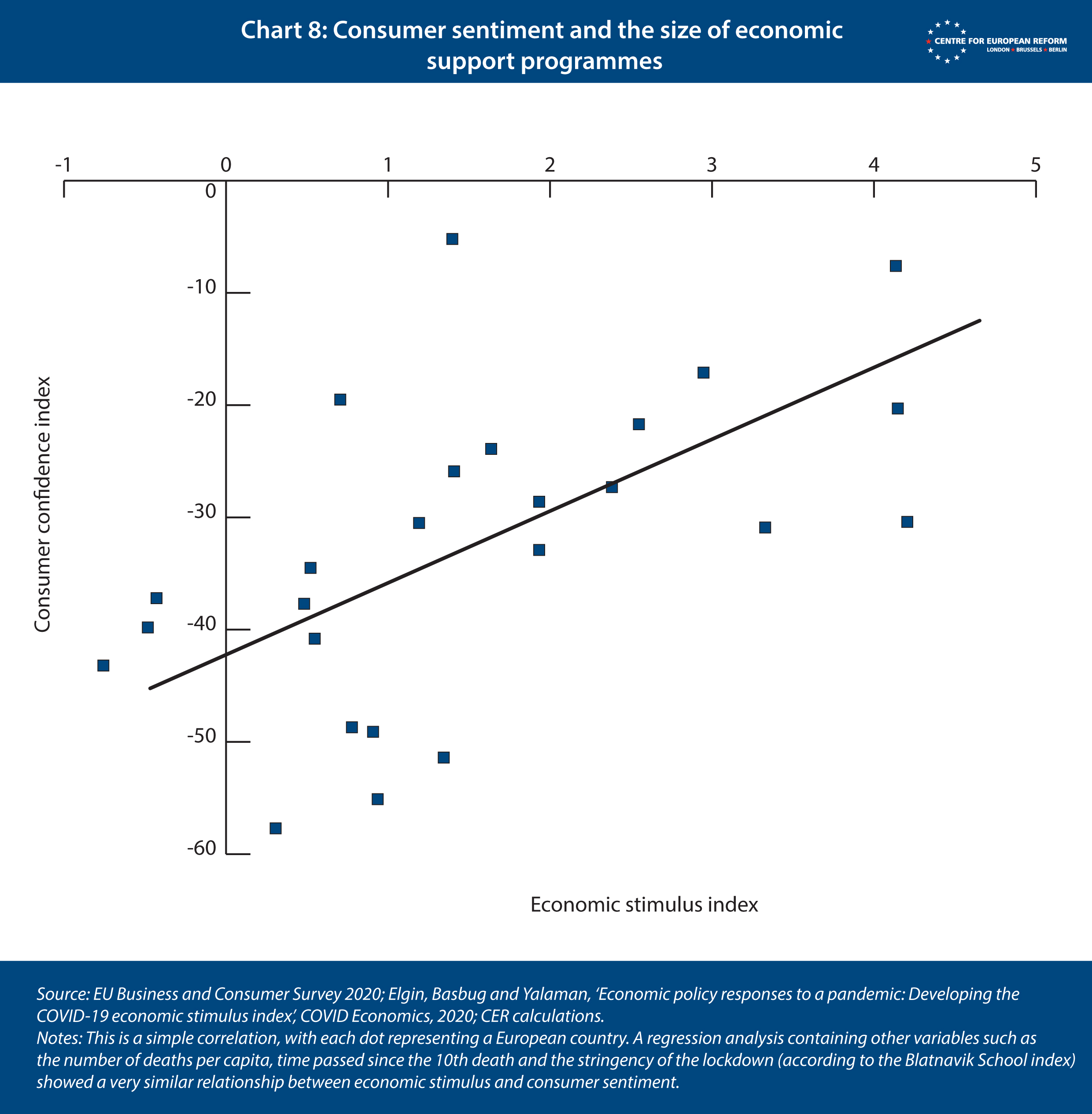

But over time, less indebted countries are better able to protect and then revive their economies. The effect of this is already visible. Consumer confidence has fallen everywhere, but the hit is smaller in countries that score higher on an ‘economic stimulus index’ put together by economists at Brown University. That index includes higher spending and liquidity support measures, as well as other forms of stimulus, such as reducing banks’ capital requirements to encourage them to lend (see Chart 8).

Second, countries with higher public debt will have to pay more to service the additional debt caused by the COVID-19 crisis. It is risky to hold government bonds of highly indebted countries: governments may resort to inflation (if the central bank co-operates) to reduce their debt stock relative to GDP, or may be forced to restructure their debt. And indeed, recent research has shown that rising public debt increases interest rates on government bonds.6 But the relationship between the debt-to-GDP ratio and borrowing costs is not ‘linear’: countries with low debt levels may not see their interest rates rise much at all when they take on more debt, whereas rates may increase quickly in high debt countries. That increase in interest rate has to be paid on the entire debt stock, once that debt stock is rolled over.7

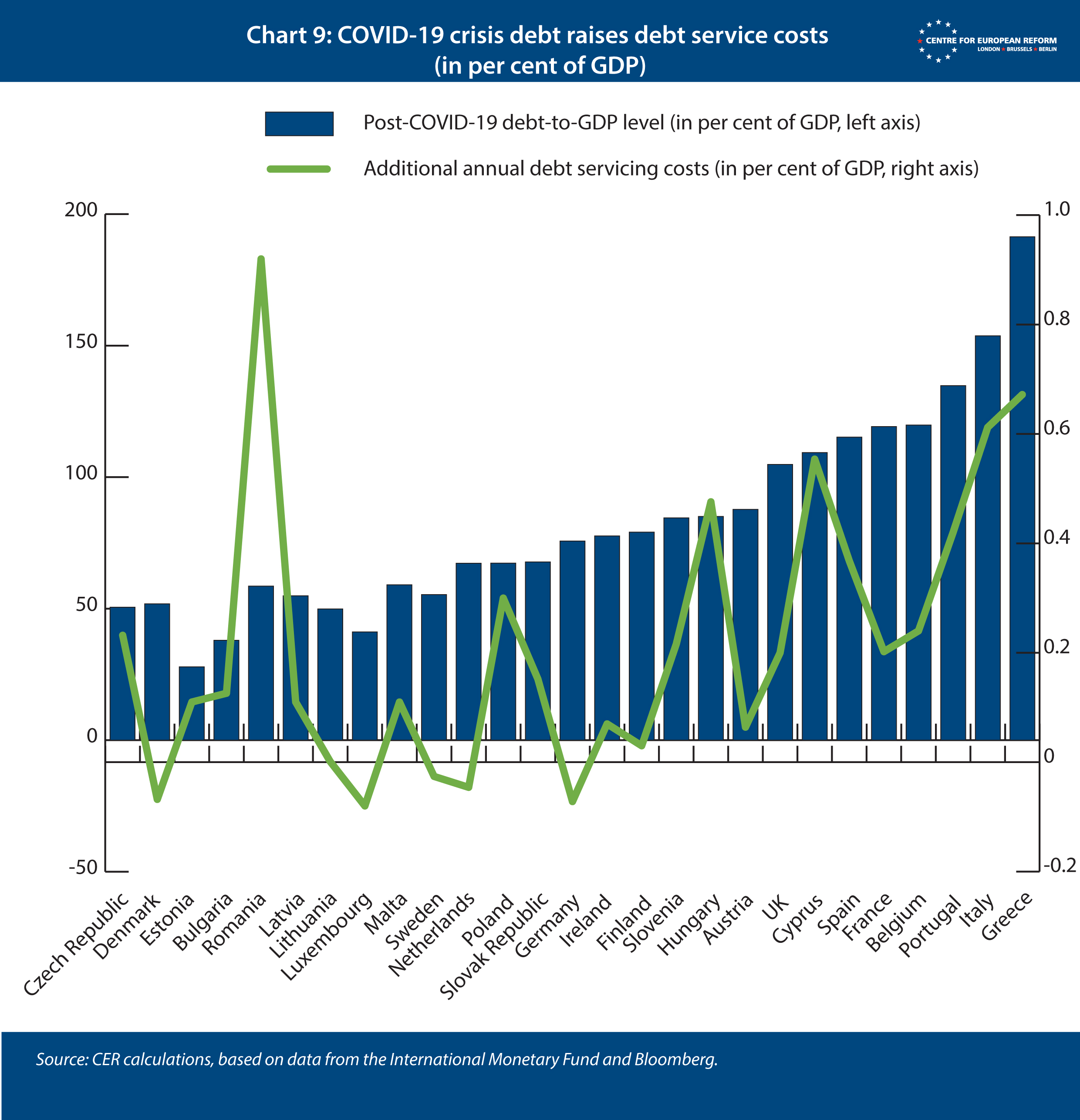

How much might interest rates rise for Southern European governments? Chart 9 shows the results of a simple calculation. We assume that all countries’ public debt increases by 20 percentage points of GDP as a result of the COVID-19 crisis – a conservative assumption, given the analysis above. Based on existing estimates, we further assume that increases in debt that stay below 60 per cent of GDP have no effect on the interest rate; and that changes above 60 per cent add between 1 and 6 basis points (that is, 0.01-0.06 percentage points) to the interest rate for each percentage point increase in the debt-to-GDP ratio.8

The debt servicing costs of Italy, Portugal and Spain then rise by around 0.5 per cent of GDP.9 Germany, Sweden and Austria, however, bear little-to-no additional cost because interest rates on their bonds remain around zero.

Italy, Spain, Portugal and Greece will find higher debt servicing costs harder to shoulder than their northern peers.

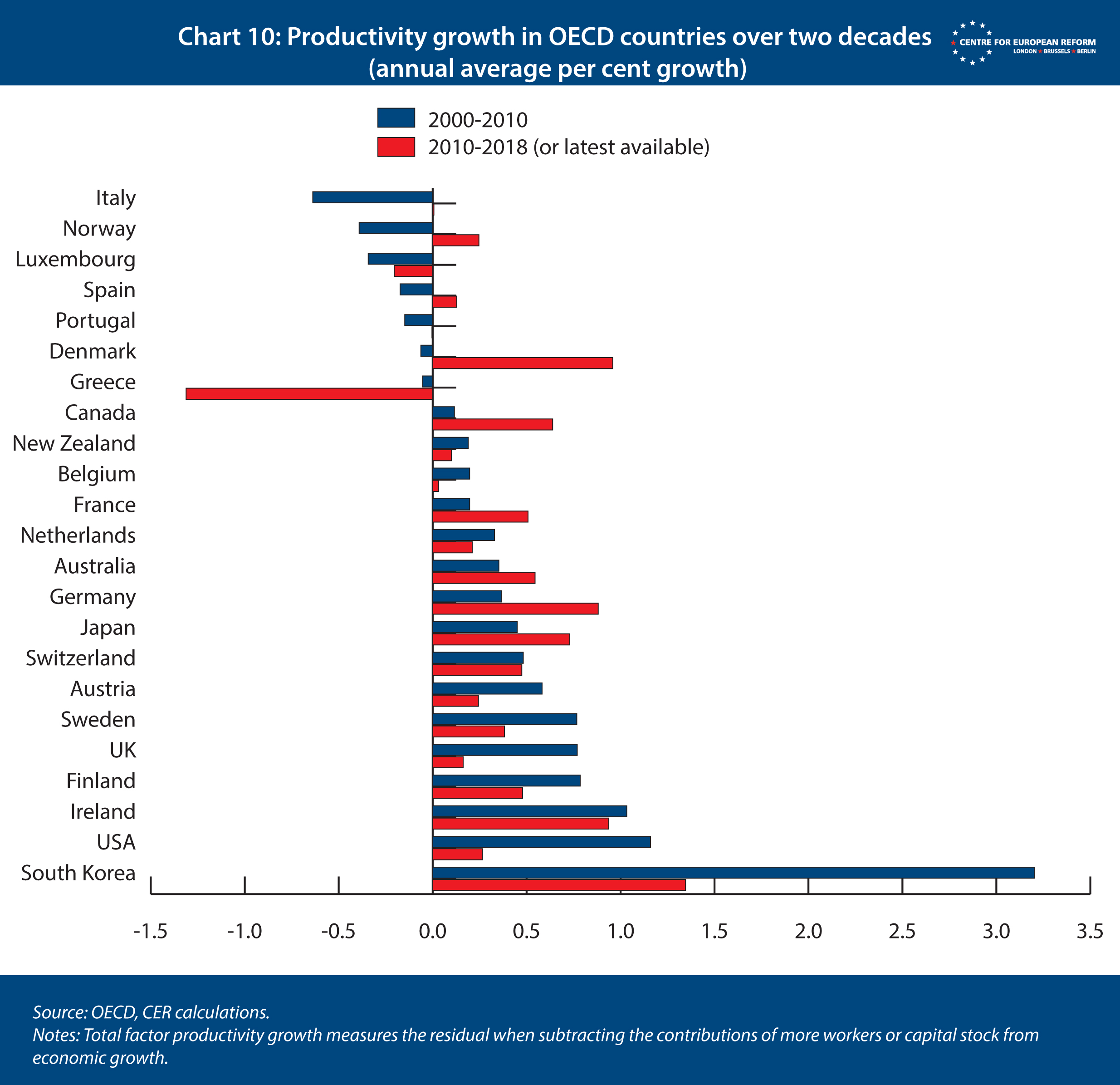

Third, additional debt servicing costs have to be funded with higher budget surpluses, which are politically and economically easier to achieve through growth than increases in tax rates or cuts in spending. But European economies have been growing at different rates over the past 20 years. A growing labour force, for example via immigration, and a larger capital stock can make an economy grow. But the main source of growth in advanced economies is improvements in how we use these inputs into the production process: through better technology, better matches between workers and firms, better management within firms, and policies that promote competition and innovation. And on that measure – ‘total factor productivity growth’ – Europe has been diverging for a while (Chart 10). Over the past 20 years, Italy, Spain, Portugal and Greece have seen almost no productivity growth, or even a decline in productivity. If these trends continue – and the current crisis is unlikely to raise these countries’ productivity – they will find higher debt servicing costs harder to shoulder than their northern peers.

Countries with higher debts will need tighter fiscal policy than their northern peers to comply with the EU’s fiscal rules.

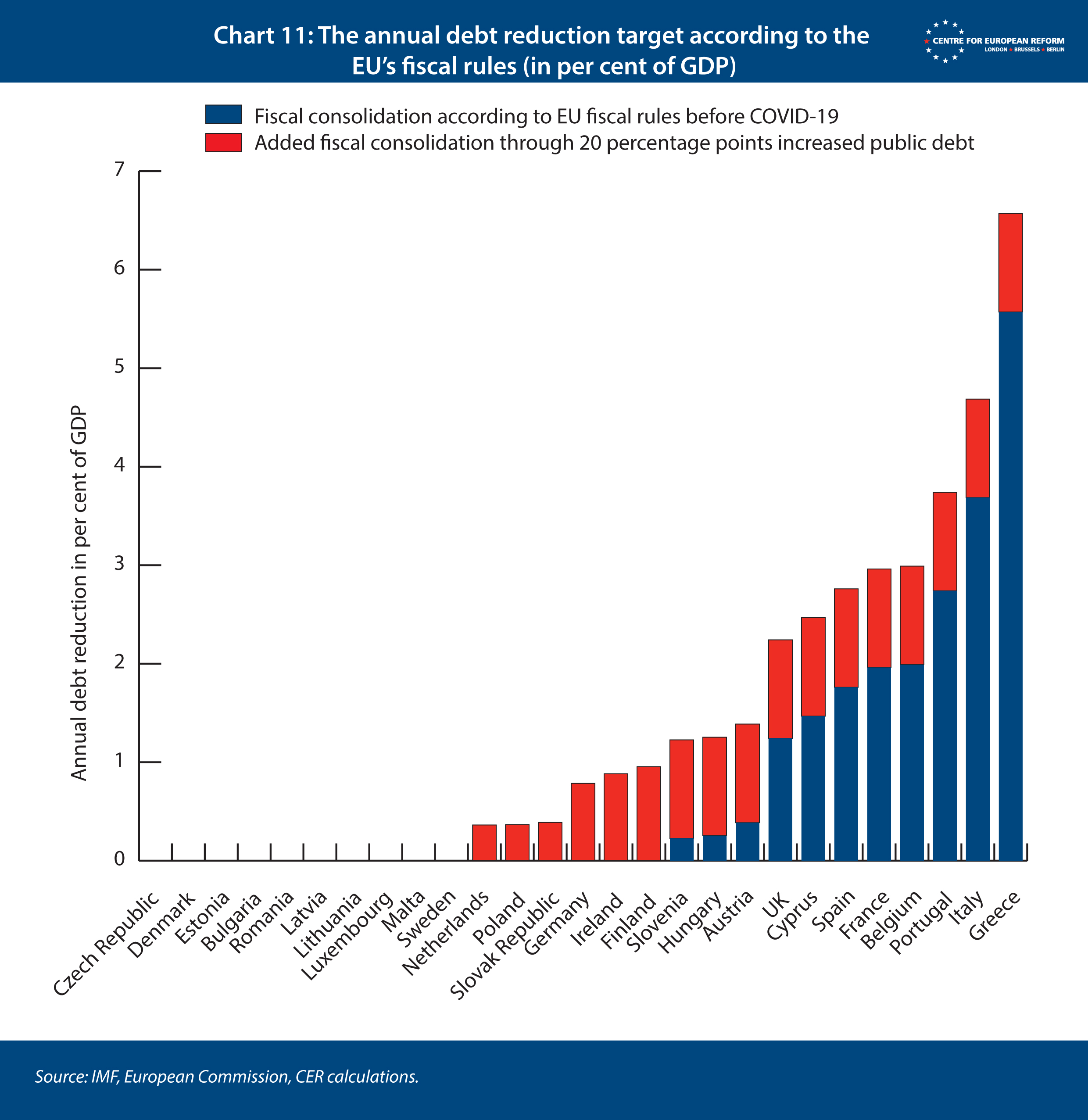

Finally, Europe is governed by fiscal rules (although they are currently relaxed after the EU invoked the escape clause for economic crises that are outside the governments’ control). One of the regime’s main planks is a debt target of 60 per cent of GDP. Many countries were already significantly above this target level, and as Chart 9 shows, the COVID-19 crisis will only worsen the situation. In order to comply with the rules, countries should reduce their debt to 60 per cent of GDP, in steps of 1/20th of the gap per year once the fiscal rules are in operation again. The COVID-19 crisis is likely to reduce growth and inflation, so it is unlikely that Southern European countries will be able to reduce their debt-to-GDP ratios through nominal GDP growth. Nor will finance ministers be able to take advantage of lower interest rates to pay down debt, as rates are already very low and likely to rise for highly indebted countries. Instead, they will have to reduce debt by running budget surpluses. As Chart 11 shows, the high debt countries will need tighter fiscal policy than their northern peers to comply with European fiscal rules – unless these rules are adjusted. That will curb growth further, and hasten economic divergence within the EU.

Conclusion

COVID-19 is likely to reinforce the decoupling of economic performance and living standards between Northern and Southern Europe, unless better-off countries provide substantial financial support to those that are hit hardest. Until Angela Merkel and Emmanuel Macron made their proposal for a €500 billion recovery fund, the richer, more frugal member-states in the north had been unwilling to provide outright transfers to Southern Europe. The recovery fund will have a difficult passage through the European Council. So far, the EU has largely relied upon the following loan programmes:

- All eurozone governments may borrow up to 2 per cent of GDP from the European Stability Mechanism (ESM) to finance health-related expenditures. But borrowing from the ESM has been anathema in Italy so far, with League leader Matteo Salvini campaigning against it, and the sums involved would only provide limited relief.

- The Commission is also offering €100 billion in cheap loans to support national furlough schemes, underpinned by €25 billion of guarantees from the EU budget. This is a useful way to support southern countries, but it will add to their debt.

- The European Investment Bank (EIB) will be provided with more capital to support another €200 billion in lending, which should help firms with liquidity. But if Germany’s initial liquidity support of almost €500 billion (which has since been made unlimited) is any guide, the liquidity needs of all European firms are around €2 trillion, so the new EIB programme is missing a zero.

The proposed recovery fund would entail more sizeable transfers. There is a logic for transfers to take place at the level of the EU, not just within the eurozone, because the high degree of economic integration between member-states means that they are dependent upon each other's economic recovery. The money would be borrowed by the EU, and distributed to the most affected sectors and regions, which, as we show above, will mean that southern member-states will be net recipients. The €500 billion would be repaid by member-states according to their relative levels of prosperity. But the details are yet to be determined.

The fund should be distributed according to two principles. The first should be the size of the drop in output in each region and sector in 2020, compared to previous years. The second should be the likelihood that the region or sector will make a swift recovery without help from the fund, given that some sectors will benefit from pent-up demand (because consumers have postponed purchases) and others may not.10

There is a risk that the scale of transfers will be watered down. The frugal northern countries – the Netherlands, Austria, Denmark and Sweden – have already voiced criticism of the new proposal, and think that loans would be sufficient. Eurozone ‘outs’ will have a point when they argue that high debts in the south are in part due to the mismanagement of the single currency. But with political pressure from Berlin and some concessions on the amount of money that flows back to their own citizens and businesses, they may be persuaded to back the idea. Central European member-states, who have handled the COVID-19 crisis well so far, will also say (again with some reason) that they should not be net contributors to richer member-states in Southern Europe through the new fund. But their concerns could be folded into a more generous EU budget offer – which, after Brexit, is missing a large net payer. With a boost to structural funds, there is little risk that the EU’s eastern member-states would be financially worse off. If the eurozone 'outs' refuse to take part, France and Germany should press for the recovery fund to become a eurozone-only instrument. A debt crisis in Italy may spread to other eurozone member-states, and the eurozone needs a common fiscal stabilisation tool.

Europe also needs to reconsider its fiscal framework, and embolden the ECB to support the recovery rather than restricting the bank’s room for manoeuvre. Even with a generous EU ‘recovery fund’, the national debt levels of all countries will be higher once the crisis is over. But this additional public debt does not need to be repaid. Countries rarely if ever repay their debt: instead, they roll it over, while fostering economic growth to make existing debt fall relative to income. Europe’s deficit and debt reduction targets are too rigid after this crisis, and need to be loosened. Europe should aim to stabilise debt in countries with high debt levels, such as Italy (something that Rome had achieved, prior to the current crisis).

At the same time, Europe should be relentlessly focused on fostering economic growth, and on inflation returning sustainably to its 2 per cent target. This is the best way to bring down debt in the process. It is important that Europe does not repeat the mistakes it made during the euro crisis: to switch fiscal policy into premature austerity and end monetary stimulus too soon.

There will be severe consequences for the EU if it fails to agree on a bold recovery fund and a stronger focus on growth. The EU’s promise of economic convergence among its member-states underpins its political appeal and needs to be reaffirmed. Since Italians’ living standards started to diverge from those in Northern Europe in the mid-1990s, euroscepticism has grown.11 A recent poll by Tecnè found that a majority of Italians think that EU membership has been a disadvantage for their country, and a sizeable share want to leave the EU. Spain has historically been one of the most pro-EU countries in Europe, but continued divergence may result in more anti-EU sentiment there too. Unless the EU has the support of public opinion in all of its big member-states, it will continue to be dysfunctional, and in extremis its very existence may be threatened. If the EU fails to implement bold policies to support the worst hit and foster growth, the COVID-19 crisis is bound to lead to further divergence, and policy-makers will have no-one to blame but themselves.

2: ‘From today’s emergency to initial thinking about tomorrow’, Banque de France, 4th April 2020.

3: Florian Dorn and others, ‘Das gemeinsame Interesse von Gesundheit und Wirtschaft: Eine Szenarienrechnung zur Eindämmung der Corona-Pandemie‘, ifo Institute, May 2020.

4: For example, Robert Verity and others, ‘Estimates of the severity of coronavirus disease 2019: A model-based analysis’, Lancet Infectious Diseases, March 30th 2020; ‘Antibody tests support what’s been obvious: COVID-19 is much more lethal than the flu’, Washington Post, April 28th 2020.

5: Clemens Fuest and others, ‘Die volkswirtschaftlichen Kosten des Corona-Shutdown für Deutschland: Eine Szenarienrechnung’, ifo Institute, April 2020. In this analysis, we use ifo’s assumptions for 63 sectors in their fourth, relatively optimistic scenario. We (and they) exclude the public sector from our analysis.

6: A good overview of estimates on how debt affects interest rates is provided in Tigran Poghosyan, ‘Long-run and short-run determinants of sovereign bond yields in advanced economies’, International Monetary Fund, 2012. Silvia Ardagna and others, ‘Fiscal discipline and the cost of public debt service: Some estimates for OECD countries’, National Bureau of Economic Research, 2004, show a threshold at around 64 per cent, below which higher debt does not have a positive effect on rates, which guided our choice of threshold.

7: The average maturity of government bonds in the OECD was around 8 years in 2018, and 17.5 years in the UK. See OECD, ‘Sovereign borrowing outlook’, 2019.

8: Specifically, we assume that every percentage point of public debt added between 60 and 70 per cent of GDP raises market interest rates for 10-year government bonds by 1 basis point; between 70 and 80 per cent of GDP the increase is 2 basis points and so forth. Any increase above 110 per cent of GDP adds 6 basis points to the interest rate. These are added to the current market interest rate for 10-year government bonds, a standard rate for long-term debt. This is in line with the estimates in the literature in footnote 6.

9: Greece is included in the chart, but a large proportion of Greek debt is official assistance, with fixed interest rates, so the effect will be smaller than shown here.

10: Christian Odendahl and others, ‘Sharing the fiscal burden of the crisis: A Pandemic Solidarity Instrument for the EU’, VoxEU, April 2020.

11: Luigi Scazzieri, ‘Trouble for the EU is brewing in coronavirus-hit Italy’, CER insight, April 2nd 2020

Christian Odendahl, Chief economist, Centre for European Reform

John Springford, Deputy director, Centre for European Reform

May 2020

We are grateful to Gianna Angelopoulos-Daskalaki for her support for this project.

View press release

Download full publication

Related content

How the EU should co-ordinate an end to the COVID-19 lockdown

A proposal for a coronabond: The Pandemic Solidarity Instrument

Bold policies needed to counter the coronavirus recession

The big European sort? The diverging fortunes of Europe's regions