A stronger carbon market is necessary for a more competitive European industry

European heavy industry is losing competitiveness – but a weaker carbon market will not fix this. Industry should invest in low-carbon production, supported by both carbon-price signals and targeted investment incentives.

While worries about the EU’s global competitiveness have taken centre stage at recent EU leaders’ summits, Europe is split over whether it should stay the course on carbon pricing. The EU Emissions Trading System (ETS) puts a price on emissions of carbon and other greenhouse gases. But in recent months, some heavy industry lobbies – especially in chemicals and steel – have called for the ETS to be weakened in the name of competitiveness. Others, notably those who have already invested heavily in decarbonisation, caution against tampering with the ETS and warn that doing so would undermine the business case for low-carbon investments.

While worries about the EU’s global competitiveness have taken centre stage at recent EU leaders’ summits, Europe is split over whether it should stay the course on carbon pricing.

Member-states are similarly divided. As many as ten member-states, including Austria, Czechia, Italy and Poland, have asked the Commission to relax the ETS. Germany’s chancellor Friedrich Merz seemed to condemn the ETS – before quickly backtracking and highlighting its importance. While even ETS moderates like Spain, France and Germany are in favour of some degree of reform, the Nordics continue supporting the ETS.

There are two main reasons for the current wave of criticism. First, the fraught geopolitical context is making Europe’s long-standing problem of high energy prices for industry worse. As fossil fuel prices spiked in recent months due to the US-Iran conflict, some member-states argued that the ETS should be put on ice to keep energy prices down.

Second, major changes are approaching for the ETS, which currently applies to about 40 per cent of the EU’s greenhouse gas emissions. The ETS, created in 2005, sets a cap on emissions, which has been progressively tightened over time to achieve ever more ambitious climate goals through energy-efficient and low-carbon innovation. Each tonne of emissions is associated with an emissions allowance, which is effectively a permit to emit. Today, industry largely receives permits for free: if they do not suffice to cover their emissions, producers need to purchase more on the carbon market; vice versa, they can sell excess allowances. These market transactions shape the EU carbon price. Between 2026 and 2034, industry will gradually have to purchase more emissions allowances as their free allocation will be phased out: together with a lower cap on emissions, this policy change is expected to lead to increasing EU carbon prices.

Simultaneously, the EU is extending the reach of its carbon pricing policies: some imports into the EU are now exposed to a carbon price through the new EU carbon border adjustment mechanism (CBAM). In mid-July, the Commission plans to present a review of the ETS, which is expected to expand coverage to additional sectors. A new carbon market – the so-called ETS2 – is also due to start in 2028, covering emissions from road transport and buildings. This is therefore a prime time for old and new grievances about the ETS to resurface.

Opponents of the ETS usually make two arguments: that the EU is isolated in its use of carbon pricing as its main climate policy tool, and that the EU carbon price is too high and unpredictable. Both are wrong. As this insight shows, other countries increasingly use carbon pricing, and the EU carbon price, while high, is not the main culprit of European industrial woes.

The EU ETS today

A meaningful carbon price

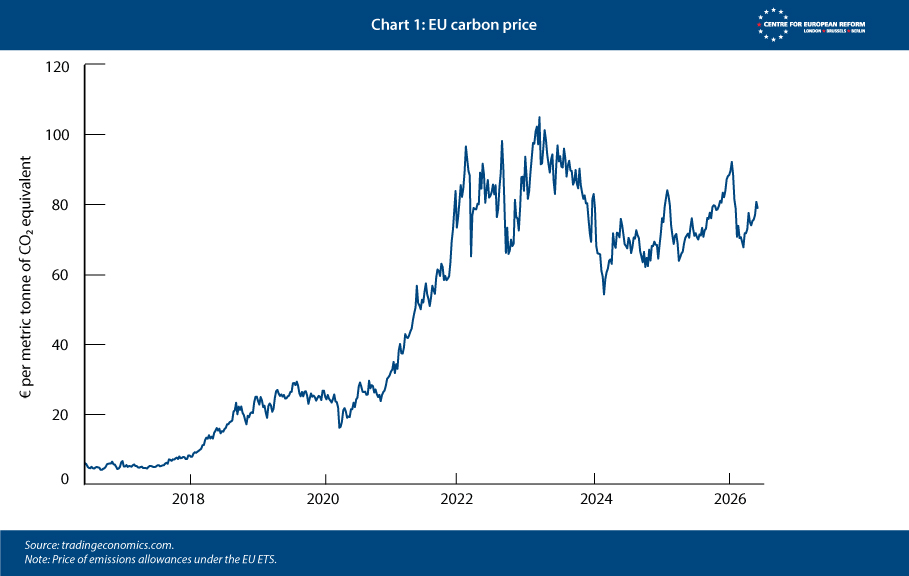

Gone are the days of minuscule, inconsequential EU carbon prices. The price of EU carbon allowances has been above €60 per tonne of CO2 since the post-Covid recovery. The upward evolution in EU carbon prices is down to two factors: first, the EU found a credible way to address excess allowances that plagued the system in its early days, depressing prices. Second, it has since approved ever more ambitious climate targets: as the EU heads towards climate neutrality by 2050, the amount of emissions will drop, and the price associated with them will increase. But recent flip-flopping on climate policy commitment has created some uncertainty: today, the EU carbon price is around €75 per tonne of CO2, down from its €100 peak in 2022 (Chart 1).

Uneven emissions reductions

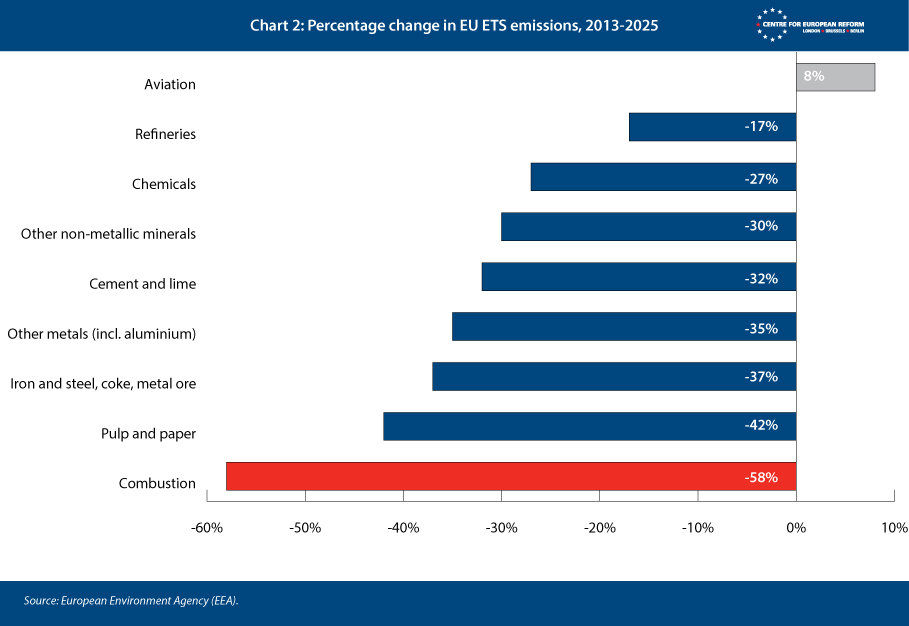

ETS-covered emissions from fossil fuel combustion – largely from power generation – have come down by about 60 per cent since 2013, when the ETS entered its most ambitious and effective phase. Increasing carbon prices prompted a shift from coal to gas power generation, and a massive expansion of renewable energy. Industrial emissions have fallen more slowly, but there is also evidence of some decoupling between emissions and production, as the gross value added of EU industrial production has increased between 2013 and 2023. Emissions from aviation, by contrast, have increased by 8 per cent (Chart 2). Among heavy industry sectors, emissions have fallen fastest in pulp and paper manufacturing and slowest in chemicals, with cement and lime, iron and steel and other metals and non-metallic minerals in between.

ETS-covered emissions from fossil fuel combustion have come down by about 60 per cent since 2013.

Persistent freebies

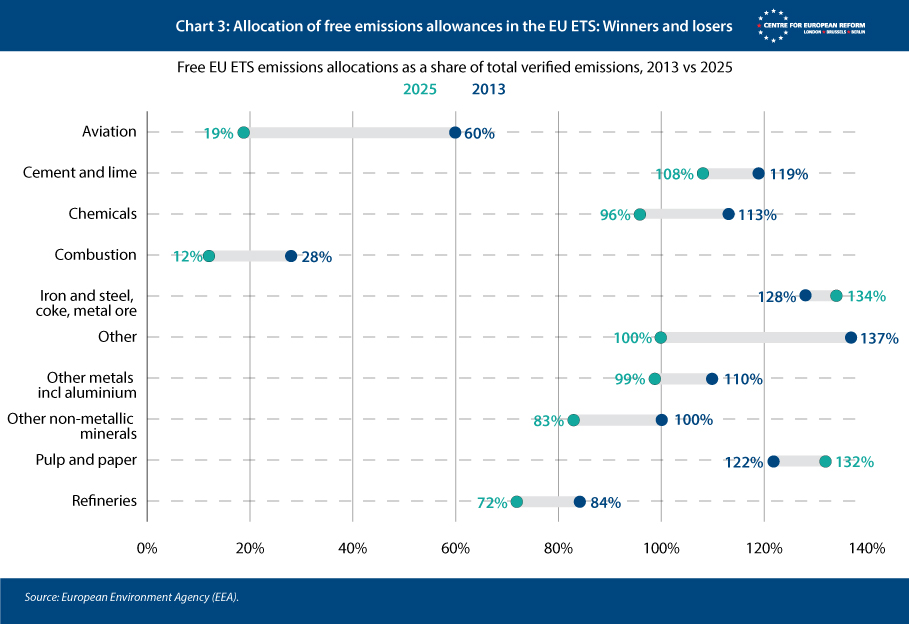

Industry and power generation have decarbonised at different speeds because not all sectors have been equally exposed to carbon prices. In the early days of the ETS, between 2005 and 2012, emission allowances were almost entirely given to industry for free. From 2013, allowances began to be auctioned. A large share of allowances remains free, however, to discourage some industries from moving carbon-intensive production to regions with weaker climate policies – a process referred to as ‘carbon leakage’.

The share of allowances that firms receive for free depends on the sector’s exposure to global trade competition and on the efficiency of production processes. Manufacturers generally receive more free allowances if they are more trade-exposed and more efficient. The European Commission regularly revises industry-specific efficiency benchmarks to reward the most efficient and innovative plants.

As shown in Chart 3, however, virtually all heavy industry emissions benefit from free allocations to this day. Some industries receive more allowances than they need to cover their emissions, which they can resell, and some have even seen the share of free allowances increase since 2013. Both factors result in sizeable windfall profits and reduced costs. While free allowances are arguably an effective tool to prevent carbon leakage, they do not provide a sufficiently strong incentive to decarbonise production.

CBAM, a transformational add-on to the EU carbon market

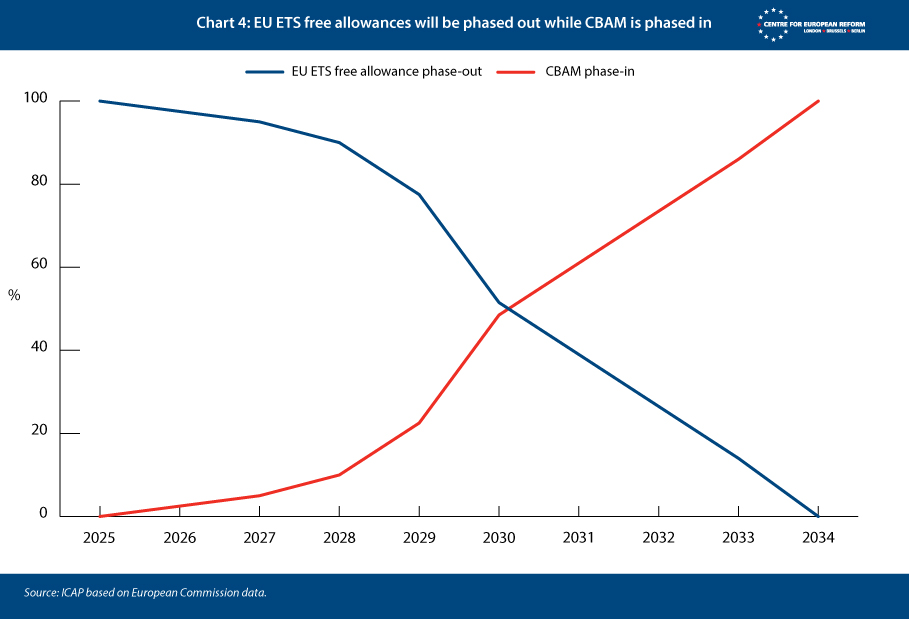

This is why the EU has implemented a new tool to prevent carbon leakage: the carbon border adjustment mechanism. Between 2026 and 2034, the share of allowances that industry receives for free will gradually reach zero, as CBAM is gradually phased in (Chart 4). CBAM is a way to charge a carbon price on imports into the EU of some heavy industry goods from countries that have a lower carbon price than the EU, or none at all.

But more and more countries and regions have been implementing carbon pricing systems in recent years, with around 100 jurisdictions now having some form of carbon price in place, covering 29 per cent of emissions worldwide. The EU’s CBAM has at times been instrumental in convincing trade partners to set up their own domestic carbon pricing scheme: the EU provided the perfect scapegoat for governments to implement an otherwise unpopular policy, while enabling them to retain carbon pricing revenues at home rather than allowing the EU to gobble them up with CBAM fees. But the EU carbon price remains among the highest in the world.

This is not to say that CBAM is perfect. While it aims to level the playing field within the EU single market by charging for imports of certain goods covered by the ETS, it cannot guarantee the same treatment for EU exports to third countries. Many industries subject to CBAM are consequently dissatisfied with it, and ask for export subsidies to bridge the carbon price gap they face outside the EU.

Scattered revenues

ETS revenues provide a substantial contribution both to the EU and national budgets. In 2024, the auction of ETS emissions allowances raised €38.8 billion in revenues. Of this, 63 per cent went to member-states and 36 per cent into different EU-level funds supporting innovation in low-carbon technology (Innovation Fund), modernisation of energy systems in low-income member-states (Modernisation Fund), and energy security (Recovery and Resilience Facility for the REPowerEU plan).

ETS revenues are not used enough to support investment in low-carbon industrial production methods, however. In 2024, member-states reported using only 5 per cent of their revenues for this purpose – amounting to €820 million – whereas the decarbonisation of energy, buildings and transport each received 20-25 per cent of revenues. By contrast, member-states devoted €3.2 billion to compensating electricity-intensive industries for indirect carbon costs, given these industries pay indirectly for carbon prices embedded in the price of the electricity they consume, in addition to the carbon price associated with their direct emissions. But this mechanism effectively dampens incentives for industry to become more energy-efficient.

ETS revenues are not used enough to support investment in low-carbon industrial production methods.

The total investment needed for the decarbonisation of Europe’s largest energy-intensive industries has been estimated at €500 billion between 2025 and 2040, or an annualised €33 billion. ETS revenues between 2026 and 2030 could reach €115 billion overall (€23 billion annually) at a carbon price of €75 per tonne. This is a lower-bound estimate, given that carbon prices are expected to increase as the emissions cap tightens, but it illustrates the opportunity cost of persistent free allocations, which would amount to €151 billion in foregone revenue over the same period. The shift away from free allocations, combined with higher carbon prices, should generate more revenues to support decarbonisation of the sectors that are most exposed to ETS prices, especially heavy industry.

Making the EU carbon price a stronger investment incentive

The purpose of the forthcoming ETS review is to upgrade the EU carbon market so it can deliver on the EU’s 2040 climate targets: reduction of its net emissions by 90 per cent by 2040 relative to 1990 levels, after a 55 per cent reduction by 2030 and on the way to climate neutrality by 2050. Because the ETS review comes at a time of intense political scrutiny of carbon pricing, it will aim to balance climate ambition with political feasibility. Expected measures include the introduction of international carbon credits, which would allow the EU to pay for some emissions reductions to take place outside its borders, and possibly a reduced rate of emissions cuts in the next decade.

The key issue is how the ETS affects industrial competitiveness and how free allowances shape investment incentives. Although carbon price levels have fallen from recent highs, many industrial players have been complaining vocally about their impact on competitiveness since they are unmatched outside Europe. CBAM aims to level the playing field – but only does so for a subset of goods covered by ETS today, including steel and aluminium, and only on the EU market and not abroad. The planned CBAM expansion to a range of composite goods –which use basic carbon-intensive goods such as steel as inputs – should strengthen protection against carbon leakage. But many firms are still worried that, as free allowances are phased out, they will have to start paying much more for carbon emissions. The fact that some non-EU competitors will also face CBAM-related costs when selling into the EU provides only limited reassurance.

The burden of carbon prices for European industry currently depends on how carbon-intensive production is and on how dependent different industries are on fossil fuels as feedstock. ‘Freezing the ETS’, as some national leaders are clamouring for, is a false solution: it would not magically relieve industry’s woes. On the contrary, it would hurt investment payback for frontrunners – businesses that have been ahead of the curve in investing in decarbonisation efforts, based on their expectation that EU climate policy would remain consistent and credible.

Europe’s reliance on fossil fuels exposes its producers to high and volatile fossil fuel prices. Investments to decarbonise industrial processes are therefore necessary to improve European competitiveness, not only to curb emissions. So how can the ETS review encourage investment in decarbonisation?

Investments to decarbonise industrial processes are therefore necessary to improve European competitiveness, not only to curb emissions.

The shift from free to auctioned allowances is central and can make a real difference. When businesses need to pay a carbon price through the purchase of emissions allowances, they are confronted with the cost of their carbon intensity. Innovating away from carbon-intensive production requires investment, but it can reduce the future costs of compliance with the ETS. Delaying the phase-out of free allowances would continue to mute the price signal that the ETS is supposed to send. If the worsening economic and geopolitical climate leads European policymakers to slow the phase-out, any extra breathing room for industry should come with conditions.

Tighter conditionality in the ETS would require two changes. First, member-states should make better use of ETS revenues to support industrial decarbonisation investments. The announced EU Industrial Decarbonisation Bank will complement these efforts by mobilising additional private capital. Second, as long as industry receives free allowances, this handout should be conditional on recipients investing in more efficient, low-carbon technologies to reduce their EU-originating emissions. That is the only durable path to reduce industry’s exposure to carbon costs.

The idea of conditionality in the use of ETS revenues is not novel. Since 2023, member-states have been required to spend ETS revenues only on measures to curb emissions. But compliance and transparency vary across countries, and the Commission is increasing pressure on member-states to ensure revenues are spent in line with climate action priorities.

Attaching conditions to free allowances would be more complex, merely because of the volumes involved: the ETS applies to 10,000 installations across power generation and industry. But it is possible. The Commission could review conditions limiting access to free allowances alongside installations’ performance relative to the efficiency benchmarks. Today, businesses subject to the ETS receive all their allowances for free only if they are among the 10 per cent most efficient installations in their category, and less if not. This already creates an incentive for low-carbon innovation. The Commission could go further by requiring ETS installations to present innovation investment plans, and by granting a part of their free allocation only if they implement those plans and reduce emissions.

Europe’s political leaders are rightly concerned about competitiveness. However, aggressive competition from China, a volatile trade environment due to erratic US policy, and dependence on fossil fuels are all bigger vulnerabilities than the ETS. The carbon price provides a ‘stick’ incentive for decarbonisation – but in hard-to-abate sectors, where progress has lagged, watering down the price pressure risks diluting that incentive even further. To support low-carbon innovation in heavy industry, the EU should strengthen the ETS, preserve its carbon price signal, and ensure that member-states use more ETS revenues to give industry a credible ‘carrot’. All this would encourage industry to innovate away from fossil-fuel-intensive, carbon-intensive production, and help Europe curb its costly dependencies sooner rather than later.

Elisabetta Cornago was assistant director at the Centre for European Reform.

Add new comment