Taming 'Big Tech': How the Digital Markets Act should identify gatekeepers

The European Commission is rushing to impose new rules on large digital platforms. A more careful approach would benefit European digital businesses.

Policy-makers and competition authorities increasingly believe that many of the world’s largest technology firms are abusing their dominant positions to stifle competition and treat their customers unfairly. The European Commission is among them. It has repeatedly fined large technology firms such as Microsoft and Alphabet (the parent company of Google) for anti-competitive behaviour and it has opened investigations into others. Recently, the EU’s Competition Policy for the Digital Era report and an independent review commissioned by the UK government concluded that some large technology firms’ market positions were deeply entrenched.

At least some of the Commission’s concerns are well-founded. Disruption in some of those firms’ core markets has not occurred for many years: Google has had a market share of 89 per cent or more in online search (measured by the number of times a user clicks on a search result) since at least 2009, for example. The risk of disruptive new market players, therefore, might no longer be sufficient to pressure large technology firms to keep delivering value for users.

This poses a potential problem for Europe. The entrenched firms tend to be US-based digital platforms, which provide infrastructure that European digital businesses rely on: app developers need app stores to distribute software; retailers use social networks and search engines to advertise; and merchants use digital marketplaces to list their products. In some cases, European digital businesses also compete with tech giants: for example, countless European companies sell their products on Amazon’s marketplace, in competition with Amazon’s own products (about 50 per cent of Amazon sales are made directly by independent businesses); and Spotify, a Swedish company, relies on the Apple app store to make its app accessible to iPhone users, in competition with Apple’s own music streaming service. If large, mostly non-European, technology firms are entrenched in their core markets, they could make it more difficult for new platforms to compete and might treat European businesses which use their platforms unfairly.

To solve this problem, the European Commission has proposed new competition rules for digital markets. The Digital Markets Act (DMA) hopes to change the behaviour of large technology firms by singling out one category of firm: the so-called gatekeepers. The Commission believes that business users are dependent on these gatekeepers to access consumers and defines them as firms which meet two criteria. First, the firm must provide a ‘platform service’: a service that brings together business and consumers, like an online marketplace or a search engine. Second, the firm must meet certain thresholds regarding its importance, impact and entrenched position. If a platform service has a sufficiently high user base, and a sustained annual European turnover of €6.5 billion or market capitalisation above €65 billion, the Commission can presume that these thresholds are met.

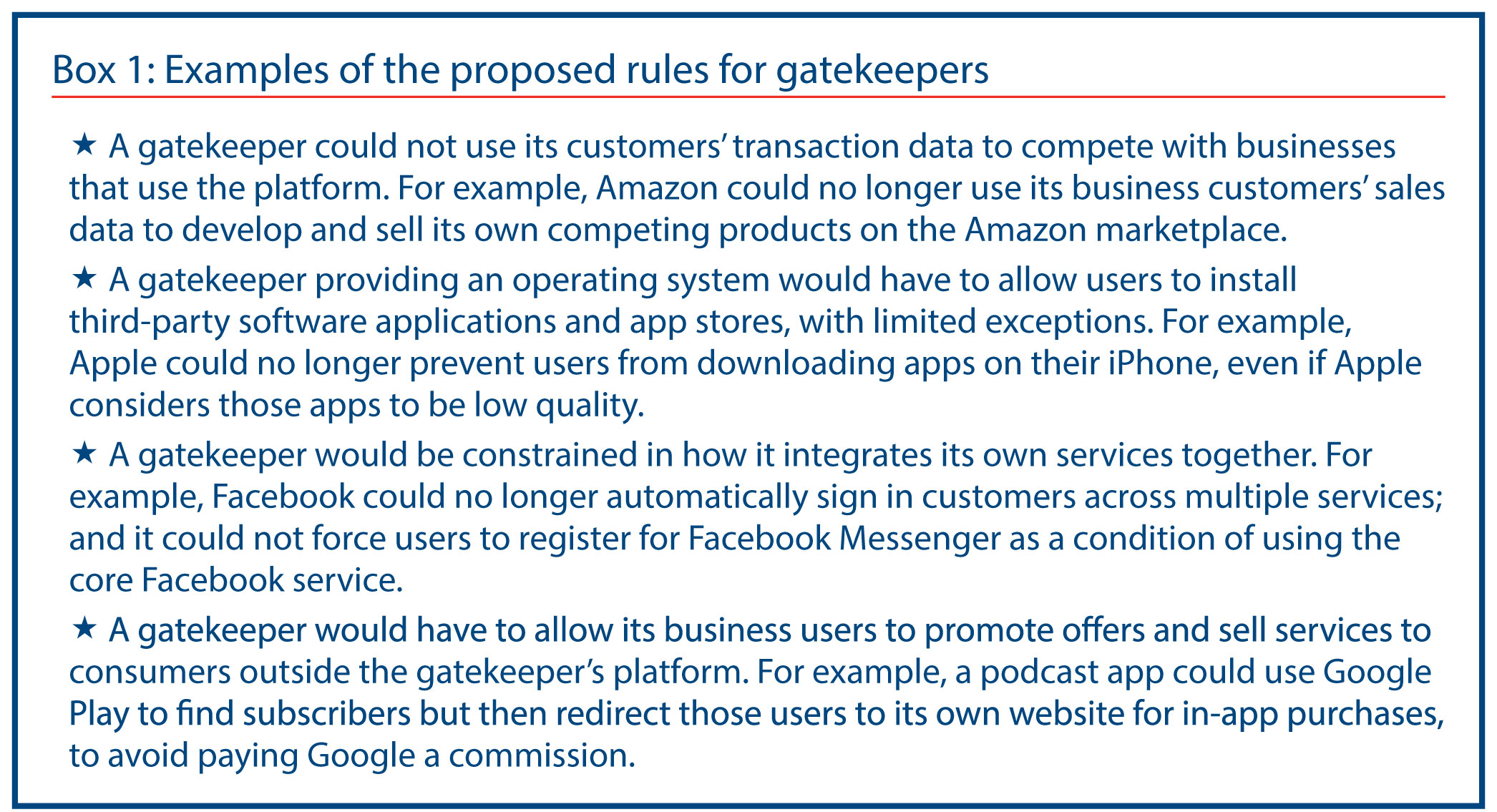

To avoid unfairness, the DMA wants these gatekeepers to comply with a set of rules to keep operating in European markets (see Box 1).

Compliance with these rules would, in effect, change the gatekeepers’ established business models and practices – sometimes in fundamental ways. These changes may improve the position of businesses which use or try to compete with the gatekeepers, but they would also reduce the value of these gatekeepers to consumers. For example, consumers would enjoy less targeted product development efforts from Amazon; they might be less certain of the quality of iPhone apps; and they would lose the convenience of being automatically signed in across a platform’s different services. This outcome could only be worthwhile if the gatekeeper rules allow the creation of new sources of competition which do not currently exist. This is why it is important the DMA only treats as ‘gatekeepers’ those firms which are genuinely entrenched and are not subject to competition, and probably will not be in the future.

Compliance with the Commission’s proposed rules would, in effect, change the gatekeepers’ established business models and practices – sometimes in fundamental ways.

Under the current proposal, too many companies could end up being treated as a gatekeeper, and not always for the right reasons. There are three problems with the Commission’s plans for identifying a gatekeeper.

First, many platform services are already subject to a degree of competition, because the consumer can easily compare prices between different services and the cost of switching to another service is low. For example, consumers using Amazon can identify the retailer of a product and, with a few clicks, purchase the same item from that retailer through another online platform or from the retailer directly. Many would do so if Amazon charged higher prices than its competitors. The risk of consumers using a competing service probably explains the pressure Amazon imposes on retailers to keep their prices on Amazon low – Amazon’s relatively low margins suggest that its own profitability is constrained too, and its share of e-commerce worldwide is only 13.7 per cent. In fact, Amazon’s situation is not too dissimilar from that of large supermarket chains. Supermarkets are often in fierce competition with each other and pressure their suppliers – which are sometimes small businesses such as local farmers – for better terms. Competition authorities have determined that supermarkets’ behaviour is generally not unfair, and these practices benefit consumers by enabling lower prices.

Second, some digital platforms may be vulnerable not only to competition, but also to ‘disintermediation’: rather than relying on a different platform, consumers and businesses could connect directly after finding each other on the platform, and therefore make the platform (and all of its competitors) redundant. The threat of disintermediation can discipline some platforms to keep their terms reasonable for both consumers and businesses. For example, Airbnb makes it difficult for a consumer to contact a service provider directly until after the consumer has committed to booking accommodation through the platform, by not showing the exact address of the accommodation until after a booking is made. However, if Airbnb priced excessively, consumers and businesses would be more likely to find ways to ‘free-ride’: identifying each other using Airbnb, but then transacting directly to avoid paying commission to the platform. Preventing ‘free-riding’ may not be unfair in all circumstances: sometimes, it can be essential for a platform to survive.

Third, digital markets are often ‘ecosystems’ – and so identifying gatekeepers by looking at the size of just a single platform service may not be a good indicator of whether the firm is genuinely entrenched. For example, the DMA identifies instant messaging services such as WhatsApp as a platform service. However, this type of service is usually free, with limited or no advertising, and most consumers use multiple providers (often, people use WhatsApp to chat with friends and Twitter’s direct messaging service for professional reasons). These services are therefore probably not viable in the long term, except by being cross-subsidised as part of a platform’s broader ecosystem of products. Considering such platform services in isolation therefore provides no real indication about whether the platform is genuinely entrenched. The Commission would need to examine how different platform services interrelate and create ecosystems that may prevent consumers or businesses from switching to alternatives.

The DMA will need the approval of the European Parliament and the Council of Ministers before it becomes law. Law-makers should make three modest amendments to the DMA during the legislative process, to ensure platforms are not inappropriately targeted as gatekeepers.

Law-makers should make three modest amendments to the DMA during the legislative process, to ensure platforms are not inappropriately targeted as gatekeepers.

One modification is merely a refinement. If a platform is designated as a gatekeeper solely because of its size and the platform challenges that designation, the Commission must undertake a detailed analysis to decide whether the platform is genuinely a gatekeeper. However, the DMA says that, when the law first comes into force, the Commission must aim to undertake this analysis for all the large platforms which challenge their designation within 12 months. This timeframe reflects the widespread expectation that all the largest tech firms will be designated as gatekeepers, and fast. However, this timeframe is not realistic. Lawmakers should amend the DMA to allow more time to undertake this exercise properly and provide more assurance that all relevant evidence will be considered.

Second, the Commission should not treat platforms as gatekeepers merely because they could become entrenched “in the near future”. Digital markets tend towards having only one or two gatekeepers, due in part to economies of scale (for each consumer a platform acquires, it becomes easier to acquire even more consumers, creating a ‘network effect’). Imposing rules on one platform in a market would not change this tendency: it would simply impose a selective competitive disadvantage on one platform, which would probably cause a different platform to become entrenched over time. If the Commission wished to preserve competition in a market which has not yet ‘tipped’ towards one or two entrenched gatekeepers, but which has characteristics which make it likely to ‘tip’ in future (even if no platform in the market acts anti-competitively), it would probably need to impose rules on all of the platforms in that market, rather than regulating only gatekeepers.

Third, the Commission should scale back the regulation of gatekeepers to digital services where competition problems are the most severe, and therefore require the most urgent intervention, and which have similar competitive dynamics. The proposed UK approach for regulating digital markets illustrates how this model could work. The UK’s Digital Markets Unit (DMU) would regulate only one type of digital service – online platforms funded by digital advertising – and would require those services to comply with a code of conduct setting out general principles. Of the largest technology firms, this would probably only regulate services offered by Google and Facebook. This focused approach recognises that digital markets are complex, and that concerns about ‘gatekeeping’ do not necessarily apply to all digital markets (or at least, not in the same way), and so carefully tailored rules for each market will be needed. The UK Competition and Markets Authority, may expand regulation to other digital markets in future: but it would need to undertake a further detailed investigation of the additional markets it wants to regulate. The Commission could take a similar approach to expanding the DMA’s scope to additional platforms over time.

Policy-makers are right to question why some large digital platforms appear to have become entrenched and whether a lack of competition is causing unfair outcomes for European businesses. However, not all digital markets suffer from the same competition problems and require the same rules to address these problems. To address the problem the Commission has identified, and with the approach the Commission proposes, the Commission needs to ensure only genuinely entrenched platforms are regulated as gatekeepers. If it does not, it risks harming investment and innovation, without generating benefits for European businesses and consumers.

Zach Meyers is a research fellow at the Centre for European Reform.

Add new comment