Is the US or Europe more resilient to COVID-19?

- At the time of writing, US claims for unemployment benefit are rising again, after a second surge in the number of COVID-19 infections. In Europe, by contrast, economic activity is picking up, and the pandemic is largely under control (although there are some unnerving signs that infections are creeping up once more).

- US President Donald Trump downplayed the severity of the virus, called upon state governors to end lockdowns prematurely (thereby “liberating” citizens, as he put it), and failed to expand testing and contact tracing sufficiently. By favouring re-opening over suppressing the virus, the US population – and the economy – may emerge from the pandemic in poorer health than most European countries. But many Europeans think that their comparative success is not only explained by better leadership, but also by the European model of larger and more interventionist government. Are they right? Yes and no.

- On the face of it, big, well-funded states appear to have provided a better safety net for workers and people infected with the disease. Kurzarbeit (short-time working) in Europe, in which governments subsidise wages to keep workers attached to firms, have prevented the unemployment rate from rising for now. In the US, it shot up in March and April. But the US headline unemployment rate is misleading; many workers who are counted as unemployed are in fact furloughed, and the temporary expansion of unemployment benefit – which furloughed workers receive – has provided generous income support.

- Emergency expansion of healthcare access provided uninsured Americans with access to testing and treatment, and brought the US closer to the European norm of universal coverage. There are no charges for COVID-19 testing, and the federal government is paying for treatment for the uninsured (although insured Americans must cope with high co-payments as normal).

- Yet the risks of the pandemic to the US are both immediate and long-term. Many states have started to lock down again as infections continue to rise. Around 1 per cent of cases will die, and another 4-5 per cent will be left with potentially long-term health problems. Renewed lockdowns will reverse the recovery in employment, and premature withdrawal of emergency income support to businesses and households would lead to steep rises in bankruptcies, unemployment and poverty. This is more likely in the US than Europe, where there is greater consensus on the need for government to impose further lockdowns and keep as many affected firms and households solvent as possible.

- The US healthcare system was not working well on the eve of the pandemic: life expectancy had stalled, even as costs had ballooned. If COVID-19 survivors who suffer long-term health problems do not receive more financial support, many will face spiraling healthcare costs and falling living standards. The US labour market creates fewer jobs than its northern European peers: after the Great Recession the US employment rate was slower to recover than in the UK and Germany. And the US lacks the support European governments provide to retrain unemployed workers and help them find jobs that are available.

- A resounding victory for Joe Biden in November’s presidential election may give him the mandate to improve the healthcare of poor and unhealthy Americans and to bolster support for the unemployed, bringing the US closer to European norms. But the Republican Party will do all it can to thwart attempts to share more risk between US citizens.

- Europeans, however, should not be complacent about the challenges they face. The European response to the crisis has certainly demonstrated the advantages of well-funded states, and a high level of risk-sharing within countries. But in the decade since the euro crisis Europe has suffered from chronically weak demand, the result of a failure to share enough risk between member-states: high public debt in Italy means that its government is less able than Germany’s to support firms and workers during the pandemic.

- The EU’s recovery fund is a welcome step towards greater risk-sharing between EU economies, but it is small and time-limited, with transfers between member-states amounting to 2.8 per cent of annual GDP. If the pandemic ends quickly, it may help to prevent Southern Europe’s debts from curtailing a recovery in the demand for labour. But as social distancing continues, private and public sector debt and unemployment will continue to rise. The eurozone’s macroeconomic risk-sharing is not automatic enough, other than through the European Central Bank (ECB), whose role in keeping government debt service low is contested in Germany.

- If the pandemic endures, US and European politics will continue to be dominated by their respective federal weaknesses. Before COVID-19, greater risk-sharing at the federal level was difficult on both sides of the Atlantic, despite the strong case for it. Whichever side proves more able to do so – with the consent of electorates – will be the more stable polity in the decades to come.

According to the popular narrative, the US and Europe represent different ways of managing market economies and democratic societies. The US has a smaller government, more dynamic markets, and a culture of individual responsibility. In Europe, taxes are high, better quality public services are available to all citizens, and more rigid labour markets provide greater protection for workers (at the price of higher unemployment).

Europeans feel that their model has been vindicated by America’s handling of COVID-19 (and to a lesser extent, the struggles of the UK). Big, well-funded states appear to have controlled the spread of the virus more effectively, Kurzarbeit schemes have curtailed unemployment, and universal healthcare systems have largely coped with the sudden rise in people needing hospital treatment.

On the US side, reasonable observers accept that Trump has given up on suppressing the virus – and that several (mostly Republican) state governors ended lockdown too early. But they point out that America’s world-leading medical scientists and drugs companies will be quicker to discover treatments and an effective vaccine. In the interim, while the US headline unemployment rate has skyrocketed, the country’s dynamism means that capital and labour will be more speedily deployed to sectors of the economy that are less constrained by social distancing, helping economic growth to return more rapidly.

But is this story about the differences between the US and European models true, and which is better placed to deal with the fallout of the pandemic? This paper weighs the evidence and finds that the differences between the two sides of the Atlantic are in some ways not as large as is commonly supposed. The US headline unemployment rate is misleading; many workers who are counted as unemployed are in fact temporarily furloughed, and US unemployment benefit has provided sufficient income support. For their part, European economies are better at reallocating resources and creating new jobs than is often assumed.

But in other ways the differences are considerable. Poor and unhealthy Americans face much more risk than most of their European counterparts. The US model is also poorly-placed to deal with the longer-term impact of COVID-19. The virus does not just kill people; it may also lead to long-term health problems for survivors, who will need public support to improve their health and keep them in work. Nor is the US labour market as dynamic as its proponents suggest, and it is less effective at creating jobs than those in many northern European countries.

As we show below, the European response to the pandemic has demonstrated the advantages of well-funded states, and a high level of risk-sharing within countries. But Europe suffers from weak demand, the result of a failure to share enough risk between countries. Unless the EU’s recovery fund is the start of more permanent risk-sharing between EU member-states, Europe’s South faces the prospect of a weak recovery and persistently high unemployment.

Why the US failed to control the virus

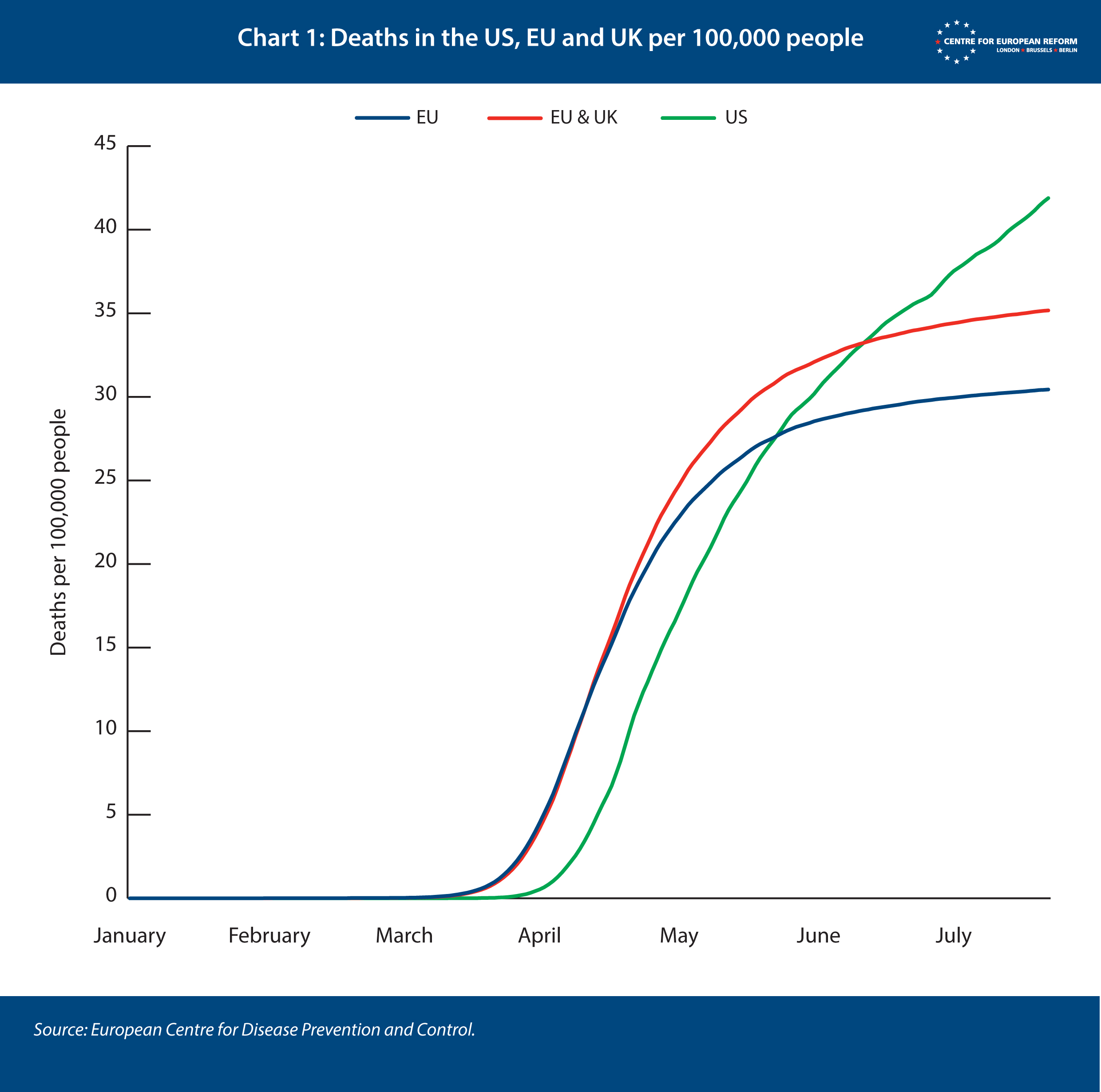

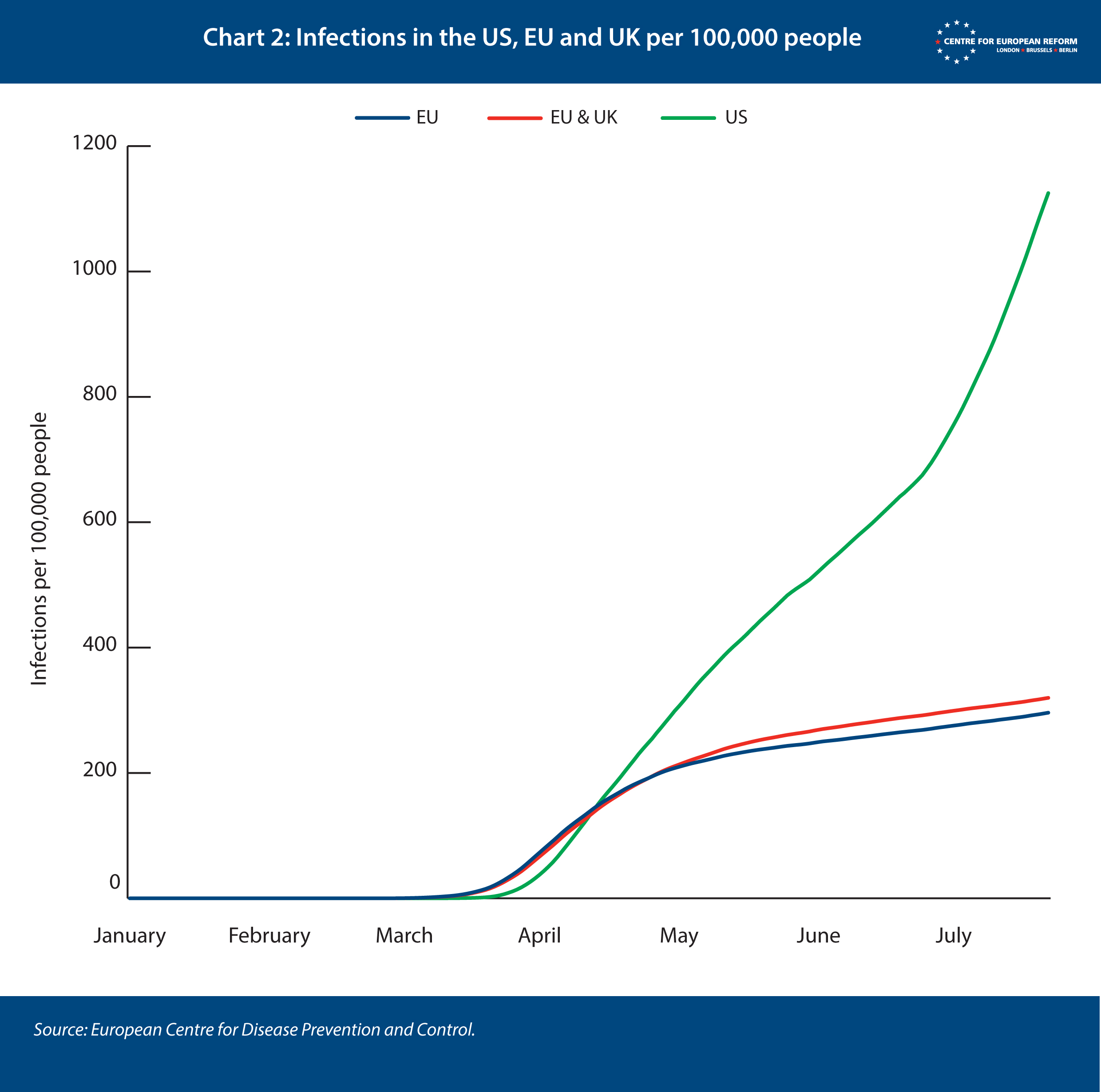

So far, the EU has performed better than the US in arresting the spread of the coronavirus and thereby paving the way for a sustainable easing of the lockdown. As of late July, US fatalities stood at 42 per 100,000 people, marginally higher than the EU’s 30, or 35 including the UK (see Chart 1). But US infections were much higher – nearly 1,200 per 100,000 people compared with 320 in the EU and UK – and rising almost ten times as quickly as in Europe (see Chart 2).

There are some issues with data comparability, reflecting levels of testing and differing methods to calculate death rates. But, if anything, these differences have probably led to an under-recording of US deaths relative to European ones. For example, France and Germany counted care home deaths from the start of the outbreak, whereas the US only required care homes to start reporting COVID-19 related deaths at the end of April.

The spread of the virus followed a comparable trend in the EU and the US until mid-April, but has since diverged sharply. The number of infected Europeans declined steadily after lockdowns were imposed, including in the UK, the worst-hit European country measured by the overall number of deaths. Europe is experiencing further outbreaks, but after dipping in May and early June US infections surged in the second half of June, exceeding their April highs. While the states that were worst affected at the beginning of the outbreak – New York, Massachusetts and New Jersey – now have the situation under control, the rebound in infections has been driven by rapid growth in states that had largely come through the early stages unscathed, such as Texas, Florida, California and Alabama. After the renewed surge in infections in the US, final American fatalities will probably outstrip the number in Europe.

What explains the differences between – and within – the EU and the US? EU figures span a low of 0.5 deaths per 100,000 people in Slovakia to a high of 84 in Belgium; and in the United States from 2 in Montana to 159 in New York State. The virus spreads more quickly in densely populated areas, especially poor densely populated areas with high levels of co-morbidity – obesity, diabetes, heart problems and high blood pressure. London has been the hardest hit big city in Europe in absolute terms, whereas New York has suffered the most in the US. Both are populous global hubs with close economic and cultural links with other countries, and cramped living conditions. It is no coincidence that the worst fatality rates have been in New York’s The Bronx and London’s East, the poorer areas of the two cities.

Older people are much more likely to die of COVID-19 than younger ones, so on the face of it, countries with older populations should have seen higher death rates. The median age in the US is 38.2, considerably lower than the EU’s 42.6.1 Indeed, the EU includes most of the oldest populations in the world. But within the EU there is no correlation between a country’s average age and the number of COVID-19 fatalities: Italy and Germany have the second and third oldest populations in the world; the former has been hit hard, the latter has not. Meanwhile, the UK has the second youngest population in the EU.

Much as the prevalence of densely populated areas is a better indicator than overall population density, co-morbidity rates explain differing mortality rates better than the average age of the population or life expectancy. Whereas in EU countries 60 per cent of deaths have been among the over 80s, the proportion is under 50 per cent in the US. The median age of a US COVID-19 case is 48 compared with 63 in Italy.2

While the virus has spread more quickly in poorer areas, there is no correlation between a country’s per capita income and the spread of the virus. For example, richer Western EU members have suffered more than poorer Eastern European ones. The picture is similar in the US. While the north-eastern states of the US are wealthier, there is little correlation between per capita income and deaths from coronavirus across the rest of the country.

A weak public health response explains US failure

Housing density and the prevalence of underlying health conditions clearly provide part of the explanation for differences in infection and death rates. But the more important factor is differing policy responses to the outbreak: the level of testing and contact tracing, the spread of the virus at the point of lockdown, and compliance with the lockdown.

First, the correlation between the number of tests a country has conducted and its infection and fatality rates is strong, but not foolproof: testing needs to take place early in the outbreak and be accompanied by contact tracing. Countries that have done it well – South Korea, Taiwan, Australia and notably Germany – have succeeded in containing the number of fatalities.

The US federal response was not only chaotic, but the issue quickly became highly politicised along partisan lines.

Second, the earlier the lockdown, the fewer infections and deaths, and the sooner it has been possible to lift the restrictions. The German lockdown officially begun on March 22nd, but schools, nurseries and universities were closed on March 13th, when restrictions on visiting care homes were also put in place. The incubation period for the virus is around two weeks and in the seven days following the start of Germany’s lockdown, 322 people died in the country from the virus. By contrast, in the week following the UK’s lockdown on March 23rd, 1,384 people died in the UK.

The difference between the two countries’ performance may partly reflect differences in the quality of healthcare, in particular in care homes, but the main reason was undoubtedly that the UK lockdown came when the virus was much more widespread than it was in Germany. It only looked as though the two countries were at a comparable stage because Germany had tested more people and therefore had fewer unrecorded infections. Other European examples, such as the widely divergent records of Norway and Sweden, confirm the importance of early lockdowns, as do the very low level of infections and deaths in Central and Eastern Europe.

Third, Europe’s lockdown measures were widely accepted as necessary by citizens and generally compliance was good. The policy response has not become highly politicised anywhere in Europe, including in the UK. By contrast, the US federal response was not only chaotic, but the issue quickly became politicised along partisan lines, with opinion polls revealing widely divergent levels of concern about the virus among Democrats and Republicans. This was partly because the outbreak was initially concentrated in blue (Democrat) states; red (Republican) ones were less affected, took limited preventative action and compliance was worse. Scepticism about the virus on Fox News may even have encouraged its spread. Researchers at Harvard, Chicago, Warwick and Zürich universities showed that areas where more people watched Sean Hannity, a host who downplayed the severity of the pandemic, had higher infections and fatalities than areas with similar shares of conservative voters, Fox News viewers, and older and unhealthy people.3

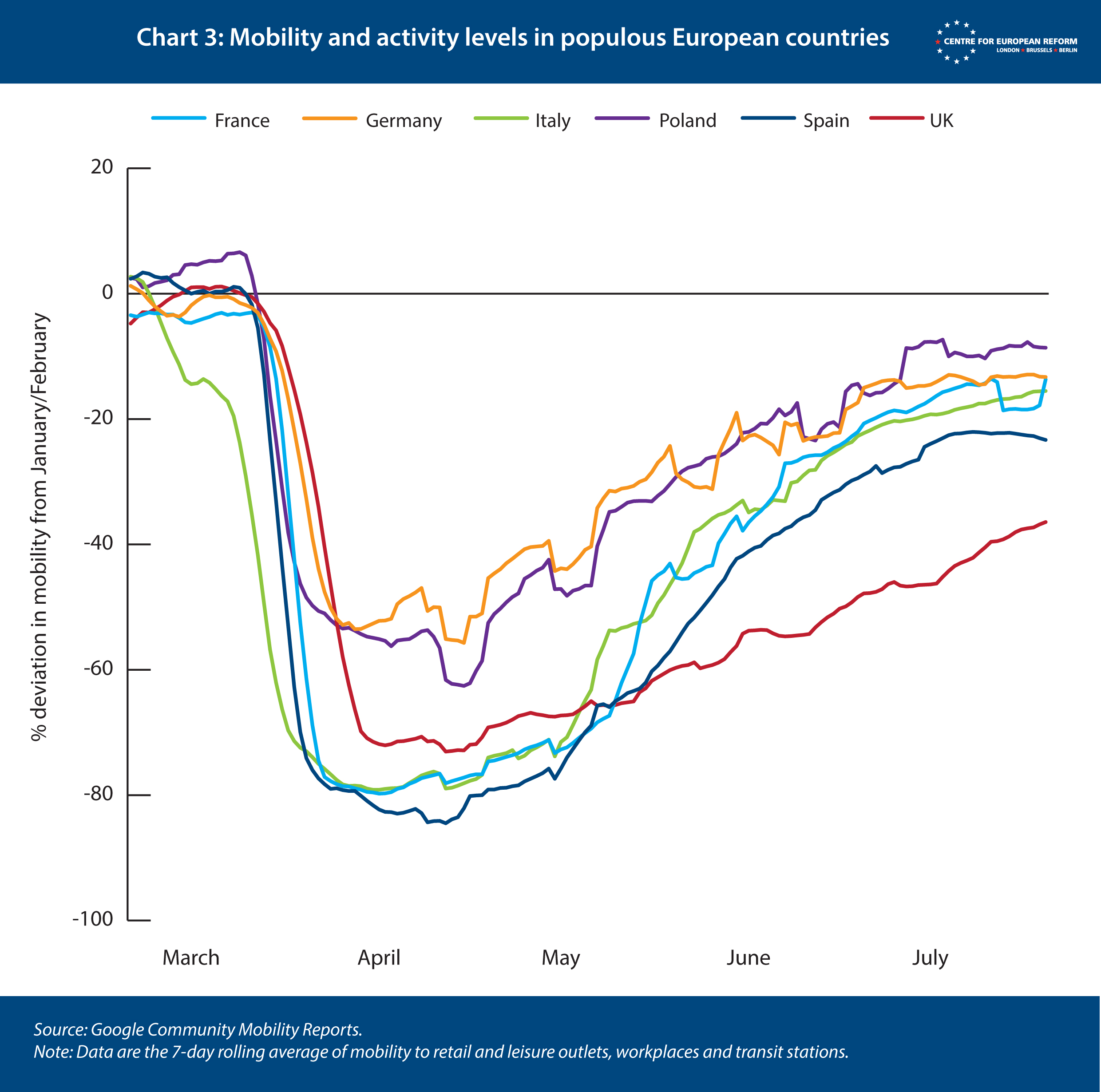

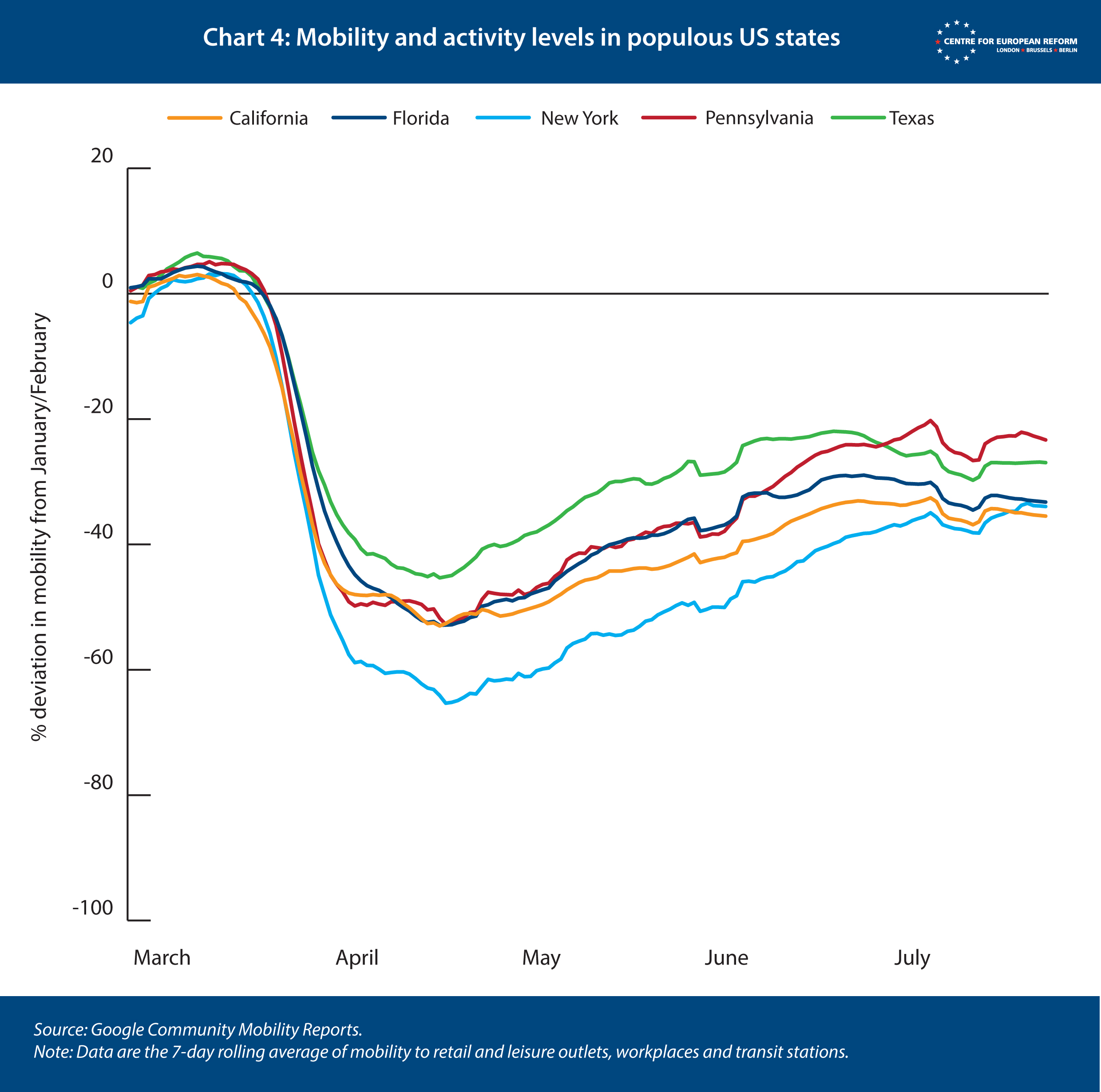

Google GPS data, which tracks people visiting transport hubs, workplaces and hospitality and leisure outlets, show that the lockdown in the US was relatively lax (Charts 3 and 4). Mobility fell much further in the EU. Even in New York State, which has been more badly affected than any EU country, it fell by considerably less than in the hardest-hit EU countries such as France, Italy, Spain or the UK. Indeed, mobility in the UK fell by twice as much as in Florida, Pennsylvania and Texas.

Better compliance with lockdown measures in Europe relative to the US partly reflects differing labour market responses to the lockdown. Whereas most EU countries were quick to furlough workers, who also have a right to paid holidays, many Americans had less choice than Europeans about whether to continue to work.

Labour market and income support policies

Both the EU and US responded to the economic shock posed by the coronavirus outbreak with unprecedented fiscal support. EU countries have provided guaranteed loans to firms to keep them solvent, and introduced short-time working and wage subsidies in an attempt to keep workers attached to firms. The US has relied upon lending, increased unemployment insurance and tax rebates to households. Meanwhile, the Federal Reserve, European Central Bank and Bank of England moved aggressively to head off a financial crisis by intervening in markets.

The direct US fiscal stimulus – increased spending, tax cuts and the waiving of taxes and social contributions – was bigger than in Europe (bar Germany). But this is to be expected, because ‘automatic stabilisers’ such as generous unemployment benefits, other welfare entitlements and high tax rates, are weaker in the US than in the EU.4 That requires the federal government to provide more discretionary spending during recessions.5 For their part, European countries have deferred unprecedentedly large amounts of tax and social contributions, including in some cases the servicing of loans. This alleviates the immediate pressure on households and businesses, but cannot be labelled ‘stimulus’ as the money will (probably) be repaid at some point in the future.

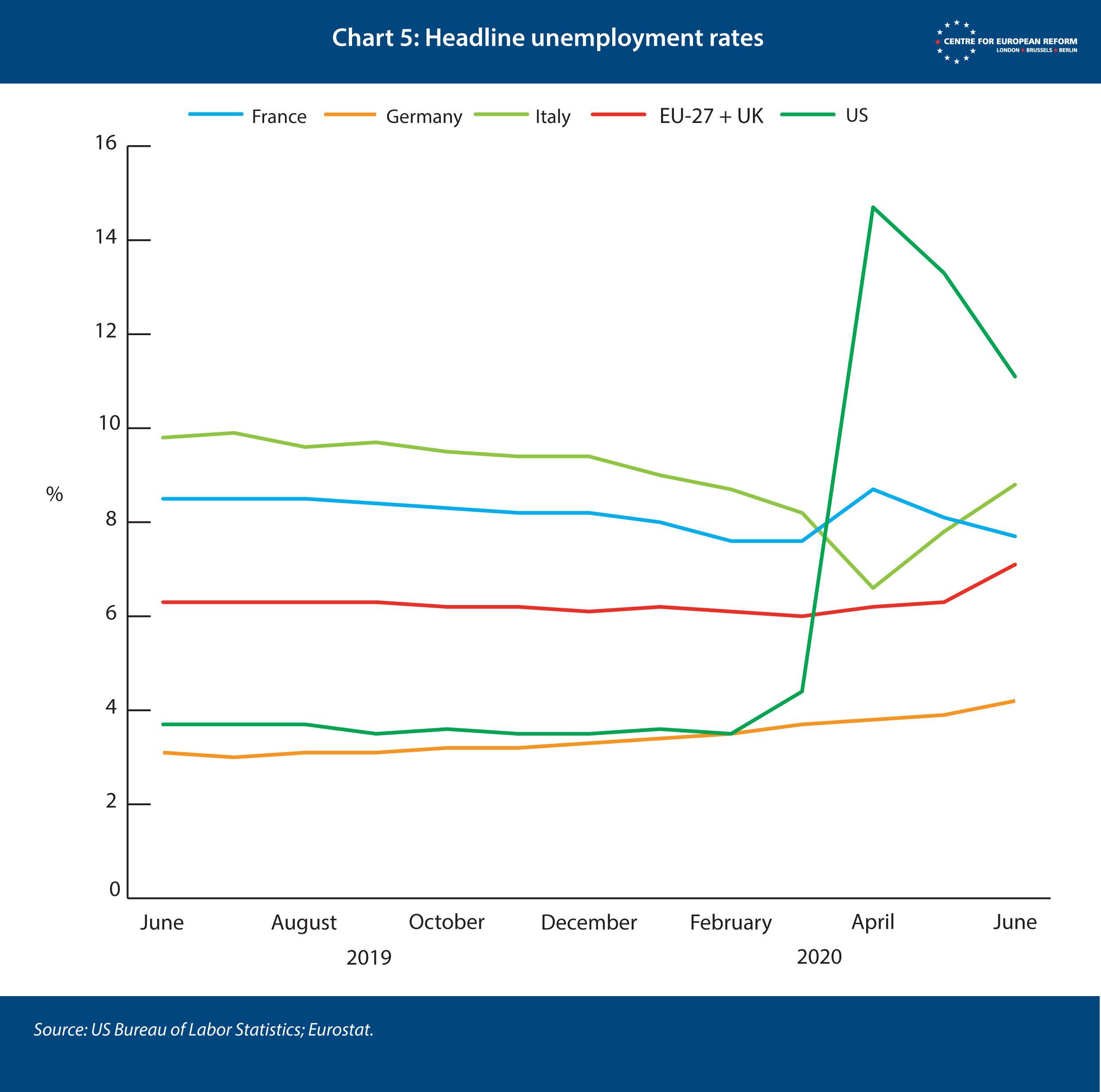

Despite comparably-sized economic shocks and stimulus packages, the US and European labour markets have behaved very differently since the start of the outbreak, at least superficially. The headline rate of US unemployment has soared, while the equivalent rate has been unchanged in Europe (see Chart 5). There are some structural reasons why the rate of unemployment is more cyclical in the US than in Europe. Public sector employment is lower in the US, for example. And it

is cheaper for firms to lay off workers in the US than in Europe. But this alone does not explain the striking disparity.

Many European countries have softened the impact of the crisis on their labour markets by employing a system – long-established in Germany and Austria – called Kurzarbeit (short-time working). In some countries, the number of hours a firm’s employees work has been reduced to take into account the fall in demand, but wages are reduced by less than the reduction in hours, with the government (or social security funds) covering the difference. Others, such as the UK, have introduced schemes that require furloughed employees not to work, in order to reduce the opportunity for fraud.

Kurzarbeit works well in countries with highly regulated labour markets and generous unemployment benefits. Where it is expensive to lay off workers, firms would rather avoid doing so, especially when they believe that they will soon need to rehire them. Notably, the UK moved quickly to introduce a government-financed scheme to subsidise private-sector wages: workers receive up to 80 per cent of their salaries (capped at £2,500 a month). Any business, regardless of size, could apply for the funding, which does not have to be paid back.

It remains to be seen how many workers in the US and the EU will ultimately end up unemployed.

Like the UK, the US has no tradition of Kurzarbeit, but did introduce the Paycheck Protection Program (PPP), under which firms with up to 500 employees could apply for loans to help pay salaries and hence retain workers. The loans are forgiven on the condition that the money is spent within eight weeks and a minimum of 75 per cent of it is used for payroll. Although expensive – the PPP has so far cost $640 billion6 – it appears to have been less effective than European schemes, considering the rise in the headline unemployment rate. There is no data on how many people retained their jobs as a result of the PPP. It is possible that the rise in headline rate of US unemployment would have been even greater without it, but it seems more likely that much of the money has gone to firms who did not need it and had no intention of laying workers off.7

Instead of using the PPP, many US employers responded by imposing temporary unemployment, with the intention of calling workers back once the economy recovers. In many cases, these workers still qualify for company healthcare benefits and receive state unemployment benefits. These benefits vary from state to state, from relatively generous in Massachusetts to paltry in Texas, but the federal average is $370 per week. However, under the US stimulus programme, unemployed workers have received $600 per week in addition to these unemployment benefits.8 This means that newly unemployed workers have been receiving around the median US net wage; some have been better off than when they were working, some worse off. The scheme expires at the end of July. In addition, income tax payers have received tax rebates – $1,200 per individual and $500 per dependent child.

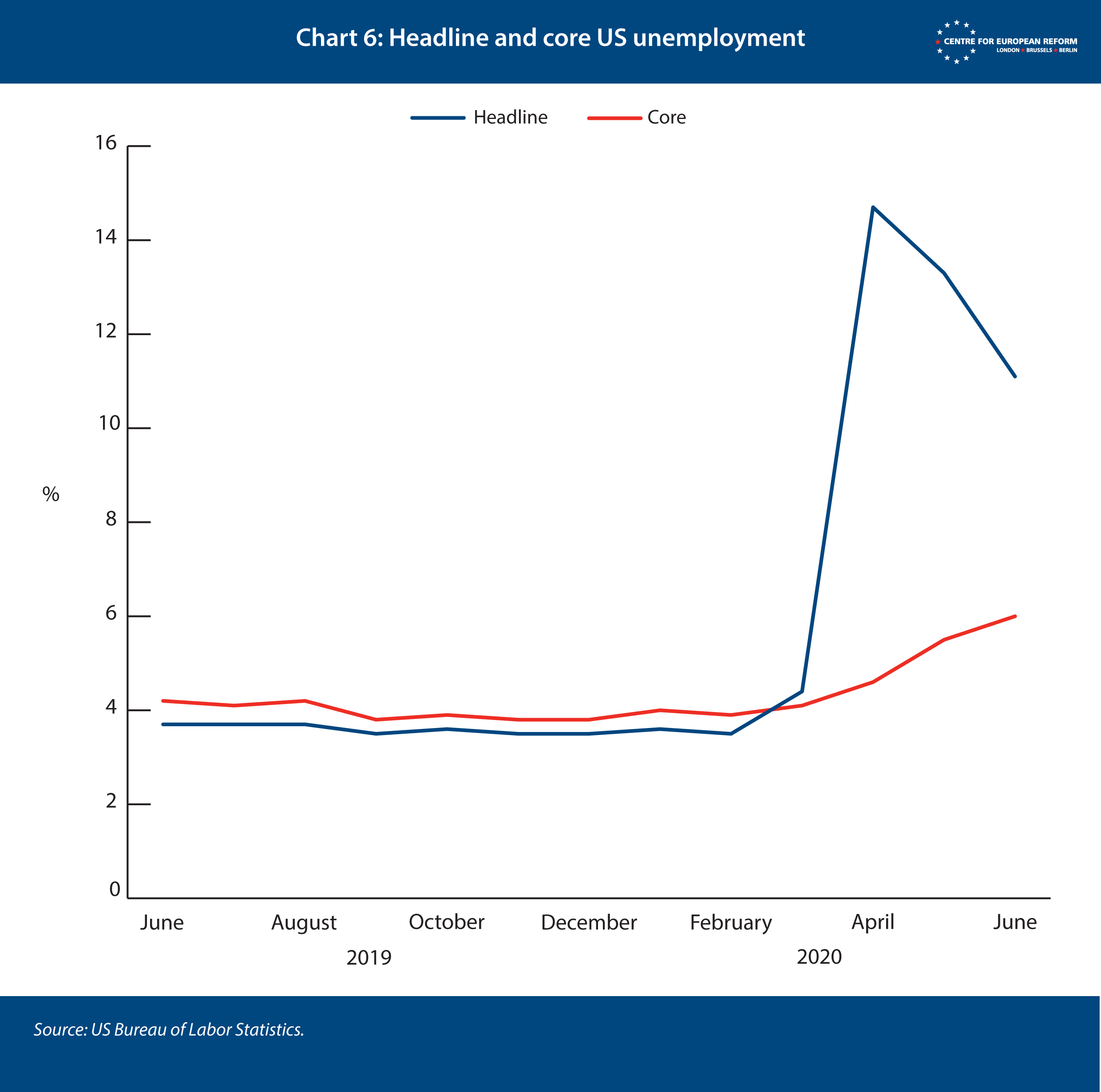

As a result of these different approaches, it is difficult to compare the performance of the US and European labour markets. A focus on the headline rates of unemployment is misleading. According to the US Bureau of Labor Statistics, nearly all the rise in unemployment between February and April comprised workers classed as temporarily unemployed (see Chart 6: ‘core’ unemployment does not count workers that have been temporarily laid off). While far more people have been laid off in the US, the state has stepped in to provide a high level of income substitution. By contrast, Europe has opted for wage subsidies of one form or another, but the collapse in demand for labour has been similar. Of course, it remains to be seen how many workers currently temporarily laid off in US – and those receiving wage subsidies in the EU – will ultimately end up unemployed.

The relative effectiveness of the differing EU and US approaches will partly depend on the length of the downturn. If there is a rapid recovery from the third quarter of 2020, the European approach will probably be vindicated. Unemployment will have risen by less than in the US, and firms will have retained workers and their loyalty, and be better placed to boost production quickly. By contrast, US unemployment will have risen more and – depending on how many temporarily unemployed workers end up taking jobs elsewhere – US firms could face higher costs rebuilding their workforces and difficulties ramping up production. The European approach could also prove to have been cheaper, not least because of the failure of the US PPP.

But what if the downturn is protracted and the recovery weak? Short-time working and wage subsidies are not a long-term solution. They are costly even for countries with generous unemployment benefits, and the longer Kurzarbeit goes on the more socially inequitable it becomes; workers with full-time jobs in the sectors covered by these schemes are protected from the downturn while others face the full brunt. But so long as countries can bear the fiscal cost, the European approach is still preferable to what could happen in the US once the exceptional support for the unemployed runs out. In the US, regular unemployment benefits typically last for only 26 weeks, but as little as 12 weeks in Florida and North Carolina. Moreover, with the exception of some north-eastern states and California, they are low compared with many European countries (though not the UK). Unemployed Americans then have to rely on welfare benefits, which are very low in some states. However, the longer the downturn and weaker the recovery, the greater the likelihood that consumption and investment patterns will shift and the challenge will not be to kick-start existing production capacity but to shift resources – capital and labour – into new industries. Could the US approach leave it better placed to manage this process than the European one?

Is the US labour market more dynamic than European ones?

The US has a reputation for labour market dynamism, compared to the average in the EU. There are fewer employment protections for workers, allowing companies to lay off staff when revenues dry up, which in theory makes them more willing to hire when revenues rebound. This has prompted several observers to argue that, while lockdowns have led to higher headline unemployment in the US than in Europe, the recovery in employment will be more rapid too, as labour shifts from contact-heavy sectors of the economy, such as hotels and restaurants, to more pandemic-proof occupations, such as delivering goods ordered online.

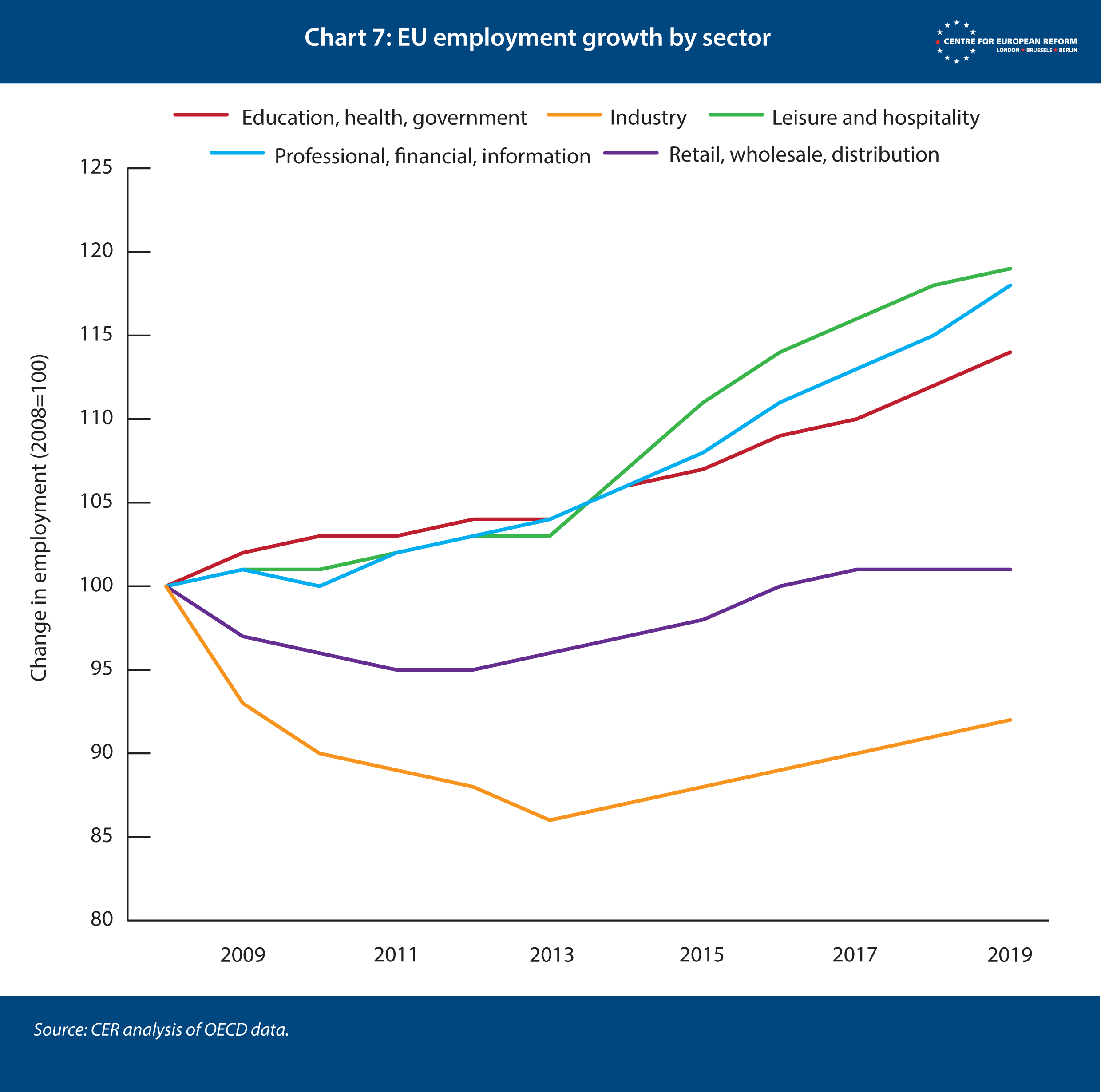

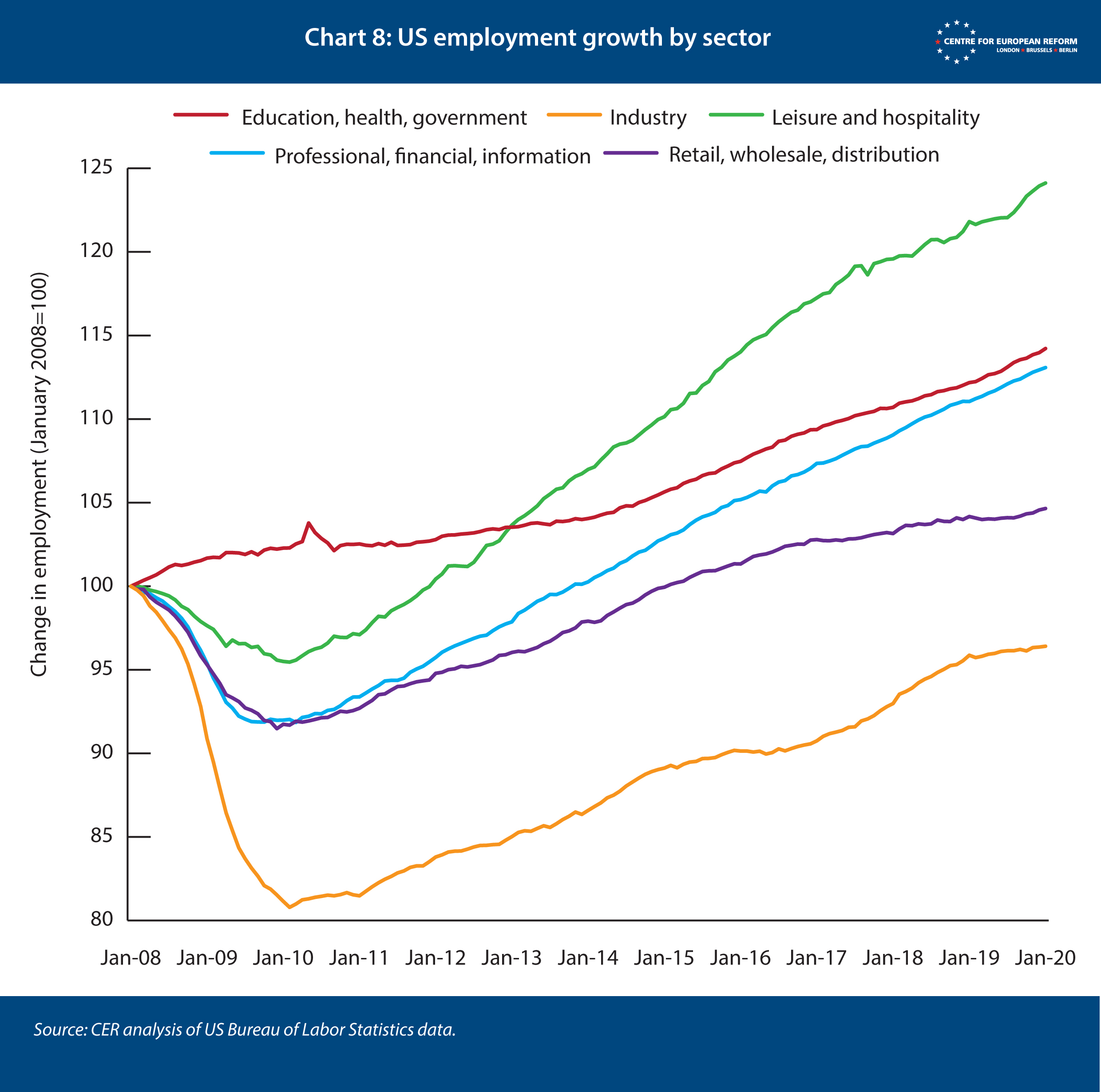

But if we compare the changing patterns of employment in the US and EU after the Great Recession, the difference between the two is not as stark as the popular narrative suggests (Charts 7 and 8). US businesses in all sectors (bar health, education and government) laid off workers rapidly in 2008-9, and by 2010 all were taking on workers again. The prolonged euro crisis meant that the turnaround did not happen in Europe until 2013. But by 2019, the pattern of job gains and losses across sectors was remarkably similar between the US and EU, with sizeable gains in leisure and hospitality and professional services offsetting falls in factory work and stagnant goods distribution. The slower pace of labour market recovery in Europe appears to have largely been the result of subdued demand, with employers unwilling to hire because their revenues were weak. Once the economic recovery took hold in Europe after 2013, employment rapidly picked up in services sectors (apart from retailers challenged by online shopping).

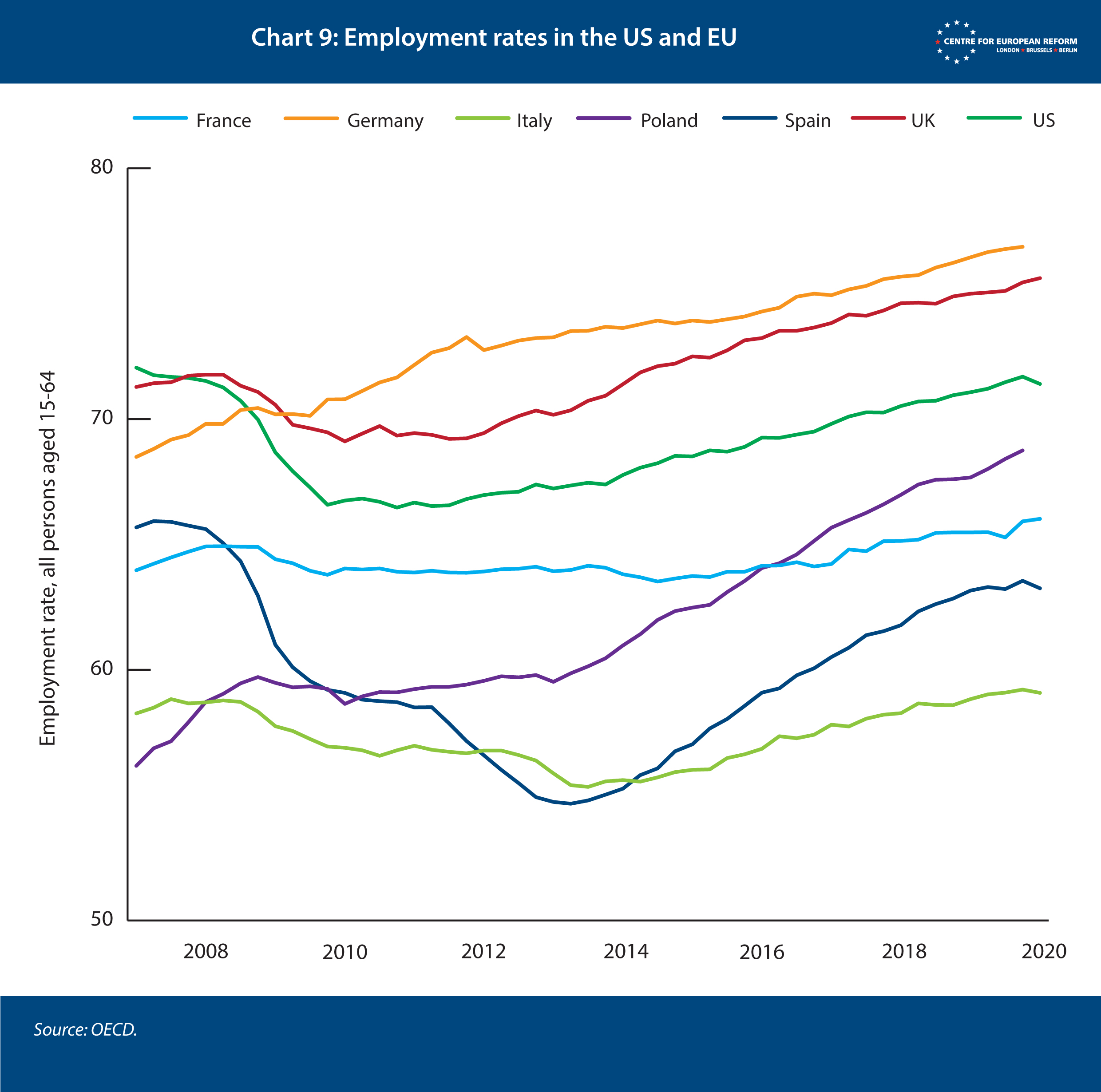

If anything, the US jobs recovery was middle-of-the-road, by European standards. While America’s headline unemployment rate fell quite rapidly after 2010, many workers had left the labour market, especially men between the ages of 25 and 64. The employment rate – the number of people employed divided by the working-age population – gives a less flattering picture (Chart 9). Germany, Poland and the UK recovered much more rapidly (the UK on the back of falling real wages and in-work benefits, which forced some people onto the labour market to maintain their household income).9 The US cycle was comparable to Italy’s (albeit from a far higher base).

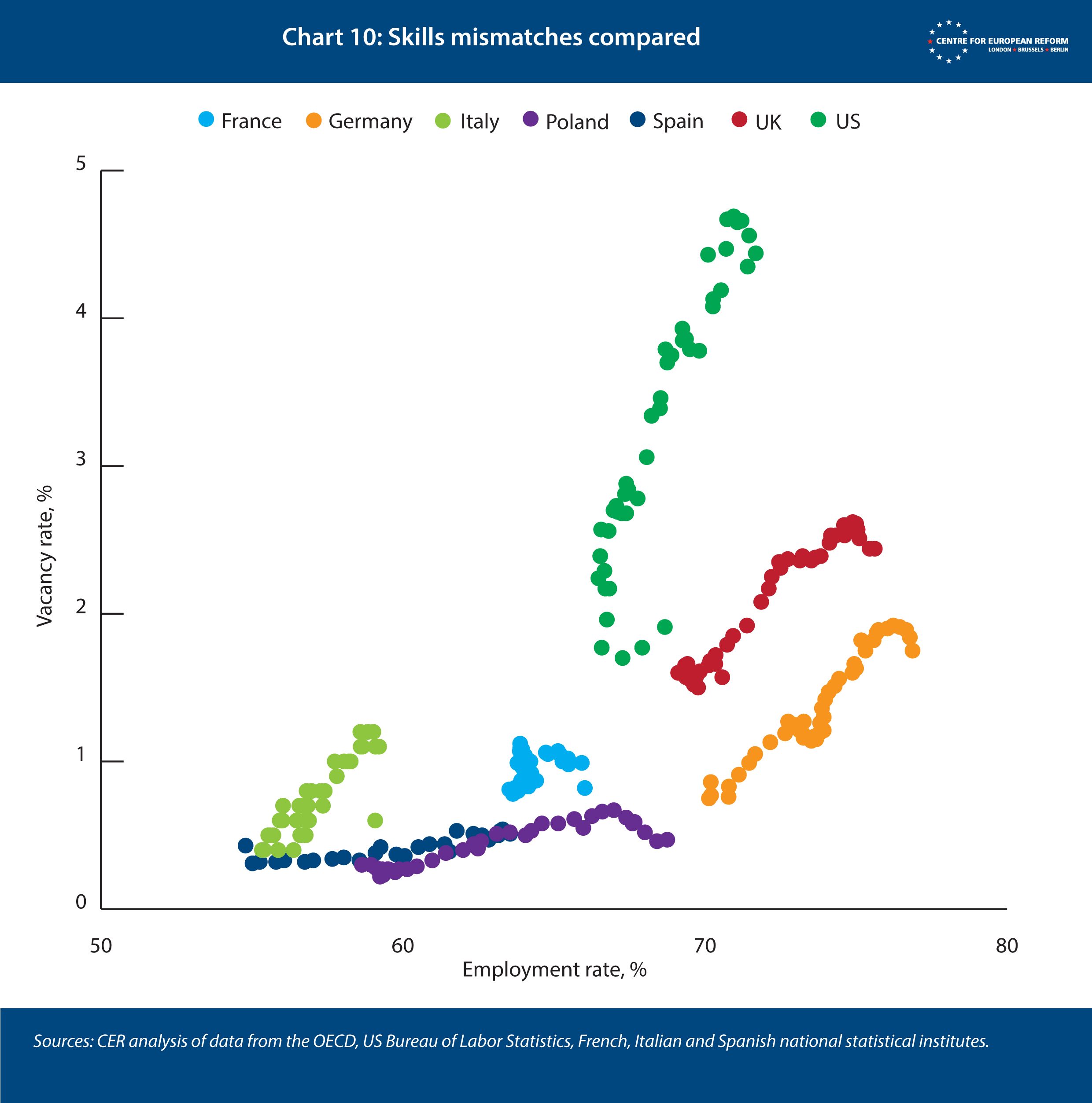

The US appears to have a bigger problem with matching workers’ skills to those that are in demand by employers. Chart 10 plots the vacancy rate (how many vacancies there are relative to employed people) against the employment rate. All countries started towards the bottom left of the chart, in the first quarter of 2009, and as the recovery took hold, they moved towards the top right. Compared to European countries, the US labour market requires more vacancies before workers who had left the labour market are dragged back into it. This is evidence of ‘skills mismatch’, either because employers were offering jobs that people without work were less able to do, or because regions with strong labour demand failed to draw in workers from regions with higher unemployment.

What does all this mean for labour market recoveries from the COVID-19 pandemic? If the recovery is relatively rapid because immunity is higher than we realise, local lockdowns and contact tracing are effective, or a vaccine and treatments are rapidly developed, we should see relatively swift jobs recoveries on both sides of the Atlantic. US workers who had been pushed onto the unemployment rolls temporarily by employers will be rehired, and furlough schemes in Europe will be unwound.

But if the virus is around for a long time, employment will be slower to recover, as workers in ‘contact-heavy’ jobs in bars, restaurants and retail have to find work in less dangerous sectors of the economy. This can take several years, as the slow employment recoveries in the US, Spain and Italy after the financial crisis demonstrate.

The UK, France, Spain and Italy are all planning to extend their Kurzarbeit and furlough schemes for several months (UK, Italy) or up to two years (France). In all likelihood, the amount that employers contribute to support the income of furloughed workers will rise over time, as has already been announced in the UK, and some countries are expected to vary the amount of support by sector, with bars, restaurants, gyms and cinemas receiving more. But the longer it takes for a vaccine to be developed, the more the ‘opportunity cost’ of furloughing workers will grow. So far, European governments have announced some stimulus measures to raise consumption, because they hope that unemployed people will be more quickly rehired if revenues are strong in contact-light sectors of the economy. The UK, France and Germany have announced measures to raise consumption, by cutting VAT (Germany), by propping up the housing market with a cut to transactions taxes (UK), and by raising subsidies for electric car purchases (France). At the time of writing, Congress and the White House are yet to agree what form of additional stimulus they will provide. But boosting consumption in contact-heavy sectors while the virus is still prevalent is a questionable policy: consumers have good reason to avoid bars and restaurants, and if the stimulus is effective in overcoming their fears, it may raise infection rates, which will only cause such ‘social consumption’ to fall again.

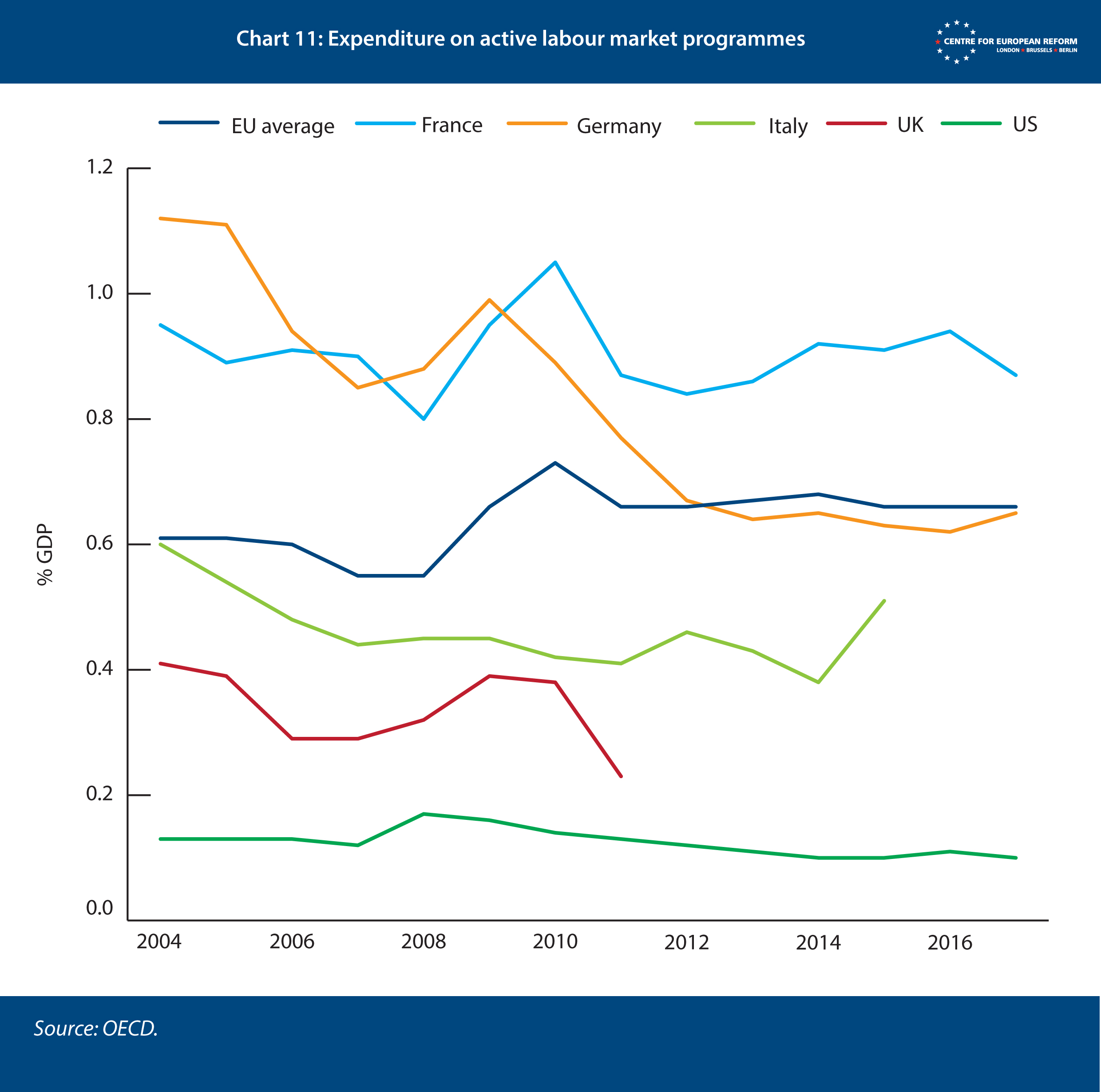

Since unemployment will be higher than during the Great Recession, and more concentrated in the low-skilled and labour-intensive leisure and hospitality sector, governments should be concentrating more resources on active labour market policies that help people to find new jobs. These policies include ‘matching’ services undertaken by job centres, training, and wage subsidies for new hires. European governments spend far more than the US and the UK on these policies, and their expenditure is more ‘cyclical’, rising in times of recession and falling during recoveries (see Chart 11). Governments should consider spending more on these programmes, which can help to improve workers’ skills and match the skills they have to those that employers want. Both also have the effect of raising productivity.10

If the past decade is any guide, the most successful labour markets at redeploying workers will be in northern Europe, not the US. But Southern Europe faces a major challenge. Demand for labour in these economies will recover more slowly than elsewhere because tourism is a big employer. And, as we discuss in the following section, public debt is higher and potential growth lower, leaving these governments with less space to stimulate demand and speed the recovery in employment.

Why the US has more fiscal capacity than the EU

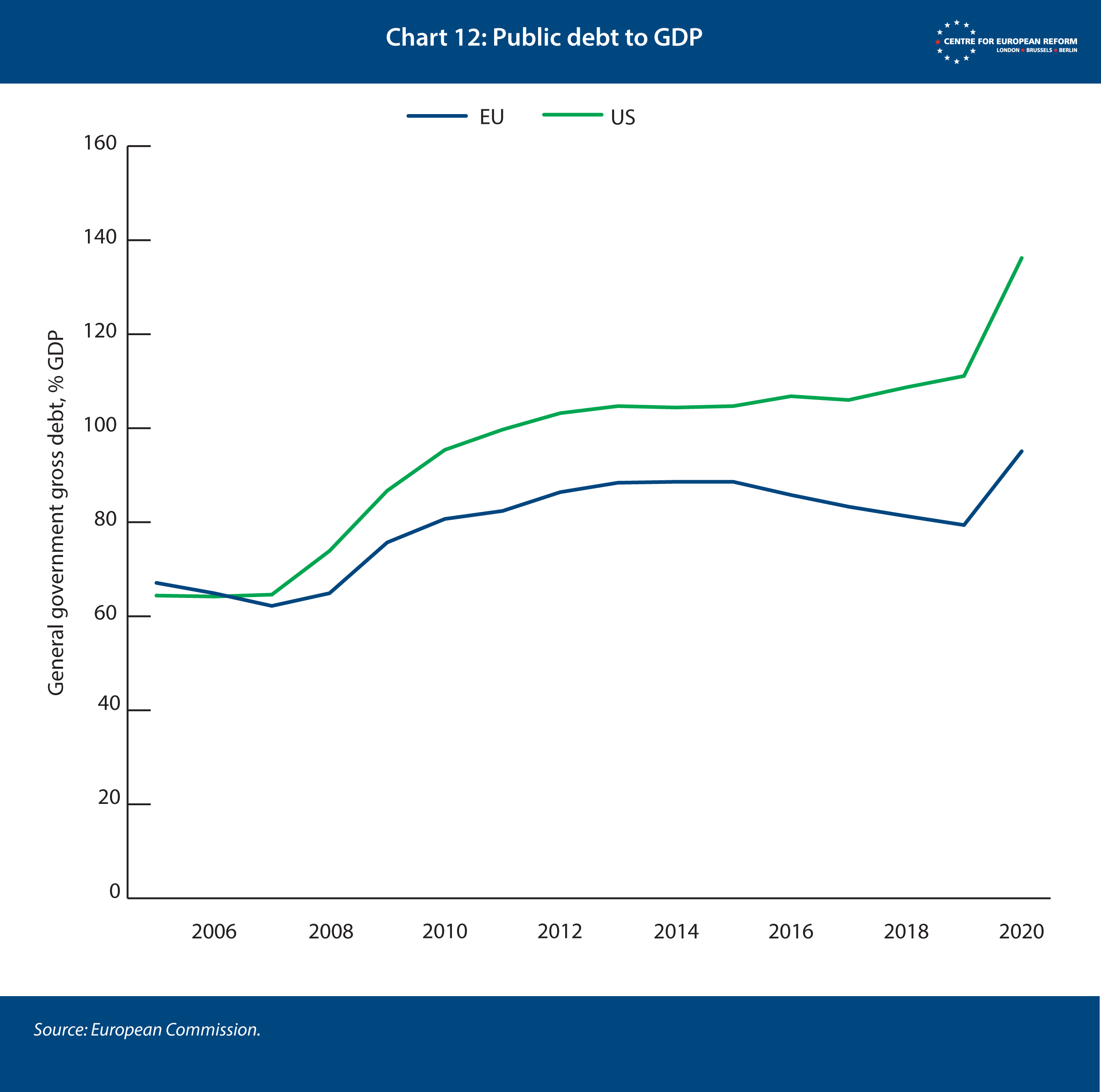

The measures employed by the US and European governments to contain the crisis and support economic activity until a resilient recovery is underway are costly. Their sustainability partly depends on countries’ fiscal capacity. On first sight, the EU has more such capacity than the US (see Chart 12). The European Commission estimates that the ratio of EU public debt to GDP will end 2020 at 95 per cent of GDP as opposed to 135 per cent in the US. Even if the rise in European debt in 2020 is greater than the Commission is assuming, it will still be significantly lower than in the US.

Fiscal capacity, however, is not determined by the level of debt alone. A host of factors are important: an economy’s growth prospects; the liquidity of its financial markets; the international role of its currency; and the level of confidence in its institutions. All help to determine how much perceived risk is attached to a country’s public debt. US debt is federal debt – it is issued by the US government rather than individual states. In short, risk is shared between all US citizens, not by state governments: if Mississippi were to issue sovereign debt it would find fewer takers than California. And the Federal Reserve stands squarely behind this debt. Crucially, the US dollar is also the unrivalled global reserve currency and US Treasuries the world’s principle ‘safe asset’, which lowers the cost for the federal government of servicing its debt.

By contrast, EU debt is largely the sum of the national debts of the 27 member-states; they do not yet issue debt jointly and therefore do not pool risk. The new recovery fund, scheduled to start in 2021, will be funded through joint debt. While it is an important step towards fiscal risk-sharing, it is relatively small, amounting to 0.7 per cent of EU GDP on an annualised basis. And within the eurozone, countries share a central bank – the ECB – which is constrained legally and politically from acting as a lender of last resort to governments in quite the way the Fed can and does. These institutional differences would not matter so much if all EU member-states had similar levels of economic development, debt and growth prospects, and if they all responded to economic shocks – such as the coronavirus outbreak – in the same way.

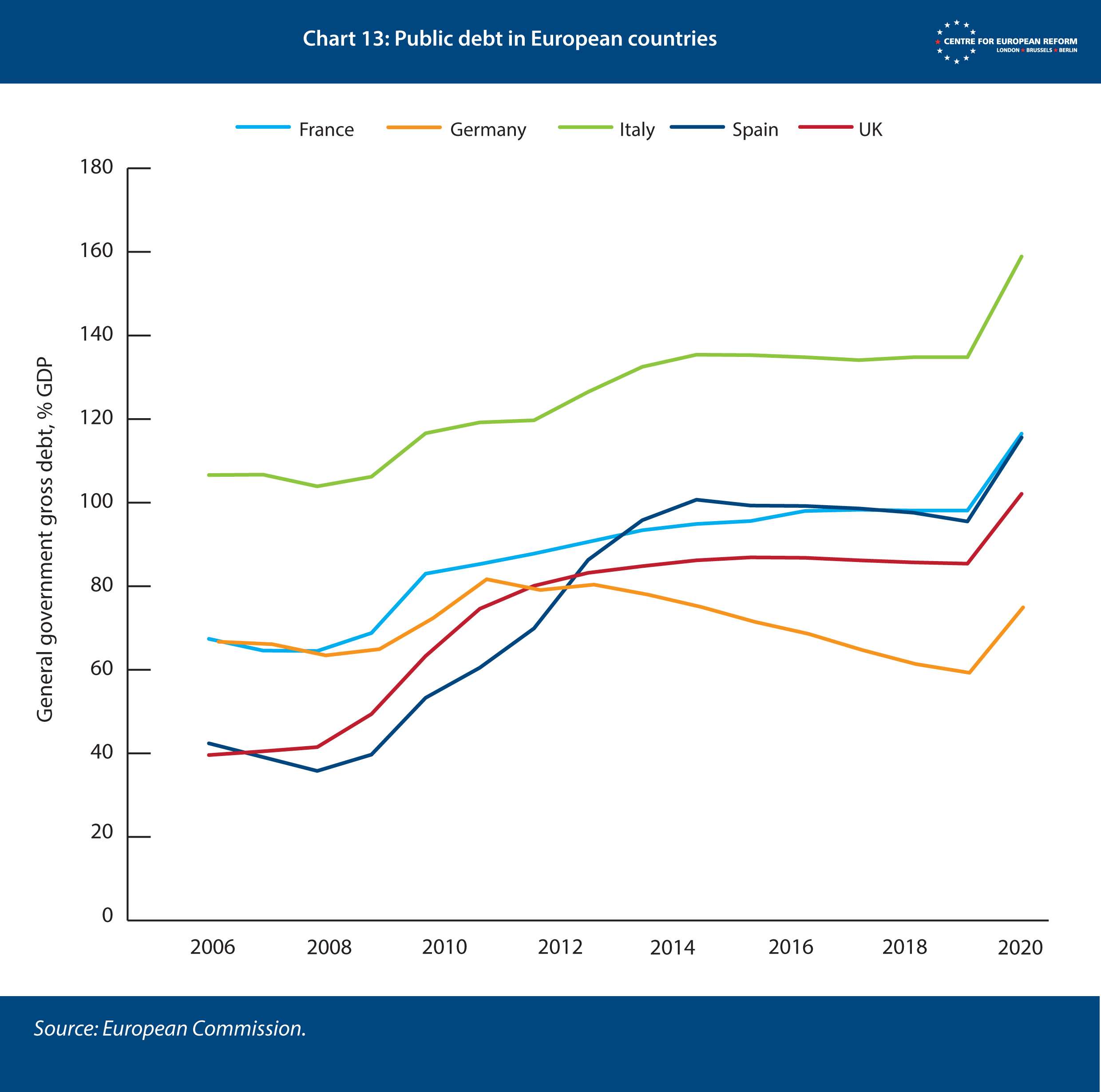

But this is not the case: they are a heterogenous group. For example, levels of indebtedness vary widely across the eurozone (see Chart 13), with some of the weakest economies facing the highest debt burdens – the Commission estimates that Italian public debt will reach 160 per cent of GDP by the end of 2020 (many private sector forecasts put it closer to 170 per cent). Italian growth prospects are also the worst in the eurozone. And together with Spain, Italy has been among the hardest hit by the pandemic.11 Ideally, the Italian government would be spending more than the others to offset the bigger impact to its economy and to ensure that the country’s recovery does not lag. But it is spending less than Germany, whose economy has been less affected than the Italian one, but which has much more fiscal space.

Member-states can now apply for credit lines of up to 2 per cent of GDP from the European Stability Mechanism to help combat the economic impact of the outbreak, but none has done so, perhaps fearing it could damage their political standing. The European Commission has proposed a €100 billion fund to provide cheap loans to hard-pressed governments to help finance unemployment support and other social programmes, but countries can borrow cheaply at present anyway.

Of more significance is the recovery fund, agreed in July 2020, which will provide €390 billion in grants to EU member-states between 2021 and 2028, with the EU borrowing the money collectively. These grants amount to 2.8 per cent of annual EU GDP, but the money will be distributed according to countries’ unemployment rates and GDP per capita on the eve of the crisis, as well as how badly their economies are affected by the pandemic. This will provide Italy, Spain and Greece with grants worth 2.5, 3.5 and 7 per cent of annual GDP respectively spread over 2021 and 2022, with smaller transfers in later years.12 This is a significant step forward, with the EU for the first time borrowing collectively and transferring significant resources to stabilise the continent’s economy. But the transfers are relatively small in the context of the recessions that many countries are enduring, with the Organisation for Economic Co-operation and Development (OECD) forecasting falls in output of over 10 per cent in Southern Europe in 2020.13 If there is a second wave, or it takes a long time to develop a vaccine, the recovery fund may not be enough to forestall further divergence between Northern and Southern Europe.

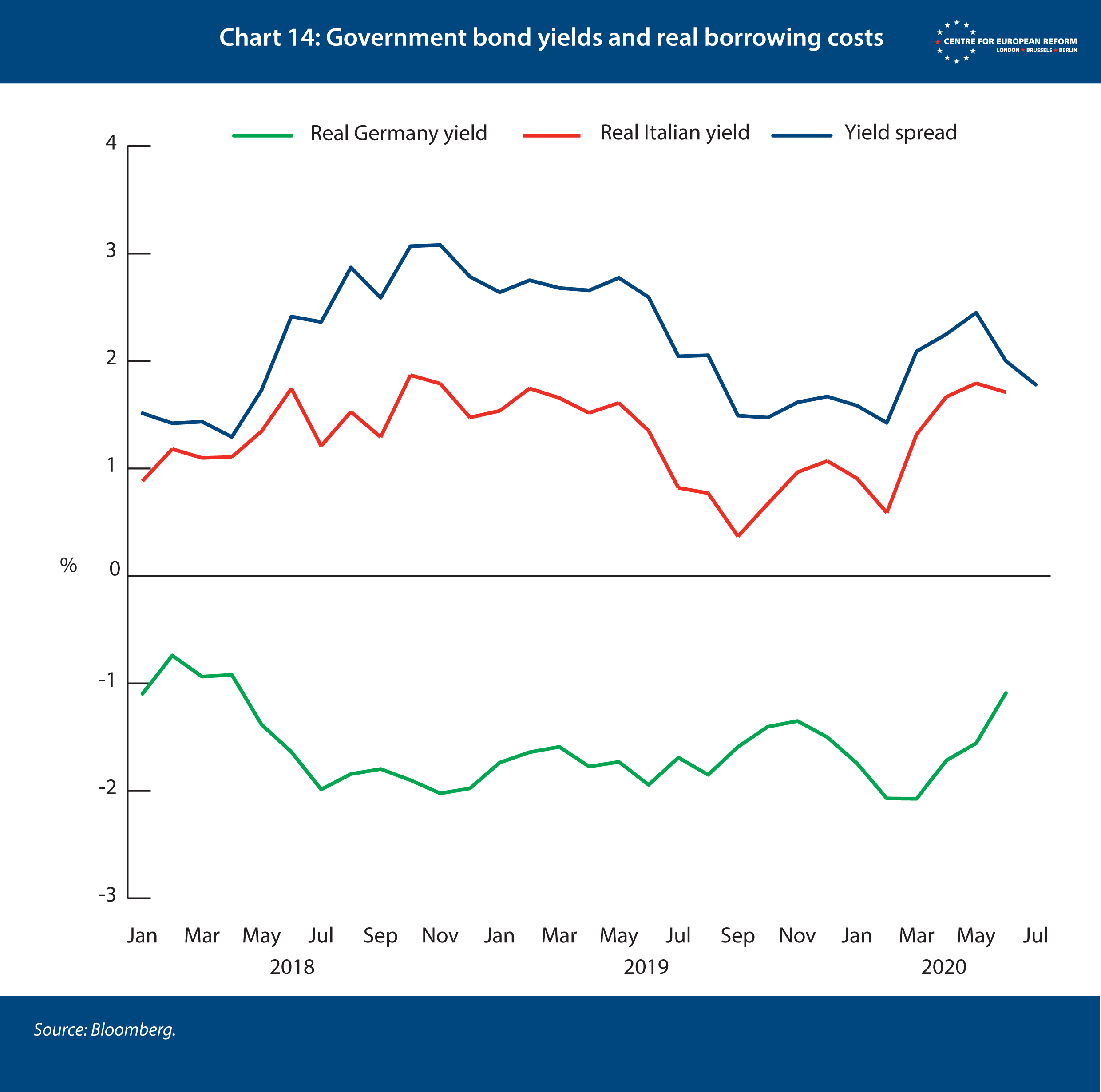

In the absence of sizeable common debt, the ECB has acted as the ‘mutualiser of last resort’, by promising to keep government borrowing costs low. The central bank is not explicitly targeting bond yields or spreads (the difference between German and other countries’ borrowing costs), but has implicitly committed to keeping Italian borrowing costs at a level that ensures the country’s debt burden is sustainable. However, with Italian inflation running at significantly below German levels, this still implies considerably higher real borrowing costs in Italy than in Germany, which threaten to hold back the Italian economy relative to the German one, leading to further economic divergence (see Chart 12).

Italy might be able to borrow considerably more money than it is now without prompting a big rise in borrowing costs; the ECB’s commitment could be enough to convince investors that Italy is good for the additional debt. After all, it would make economic sense for the Italian government to spend more now – it would bolster the country’s economic recovery and could ultimately reduce its debt burden. But there are good reasons for the Italian government’s caution. If it were to step up borrowing sharply, it could make it harder for the Commission to gain the support of all member-states for its plans to spend its share of the recovery fund. And it could also embolden northern criticism of the ECB’s alleged ‘latinisation’, making it harder for the central bank to make good on its commitment to keep Italian borrowing costs at sustainable levels.

European social models are more able to cope with a shock of the magnitude of the pandemic, but the EU’s southern member-states are less well-placed to cope with the fiscal implications of a long downturn. Europe as a whole has less fiscal capacity than the US, despite lower aggregate levels of debt. The lack of mutualization and only partial integration of member’s capital markets means that the EU’s fiscal capacity as a whole is lower than in the US. The recovery fund, while helpful, will not be enough to address the differences in fiscal capacity between the member-states. Securing Europe’s social models will require a permanent, rather than one-off, common fiscal capacity, and one that is larger and stabilises the economy with more automatic spending and borrowing.

The US has plenty of fiscal capacity, but there is formidable political opposition to using it, at least for public services and welfare programmes. While the US’ fiscal response to the crisis has been larger than Europe’s, the US lacks strong automatic stabilisers, and additional government action is needed to shore up the economy. With US politics strongly polarized, putting together the political coalition needed to push through such reforms will prove difficult. Put bluntly, whereas Europe refuses to share enough risk between countries, the US refuses to share enough risk between citizens. Unlike Europe, the US is a single demos, but it has found it politically difficult to socialise risk to the extent we see within European countries. Perhaps the biggest policy challenge facing the US is its healthcare system, which is massively expensive yet generates poor health outcomes compared with Europe.

COVID-19 and healthcare models

The European healthcare model is better equipped to deal with the economic and social consequences of the pandemic. Europe spends less on healthcare and has better outcomes, largely because European healthcare systems are simpler, better regulated and universal. Americans are also unhealthier than Europeans. This partly reflects greater inequality and poverty rates, but Americans are also less physically active. European healthcare outcomes have been improving faster than American ones, where the growth in life expectancy has stalled, and deaths from alcohol, drugs and suicide have risen. The question is whether European health outcomes are set to worsen because of the unprecedented expenditure restraint of the last ten years, the demands placed on healthcare systems by the coronavirus outbreak, and many countries’ lack of fiscal space.

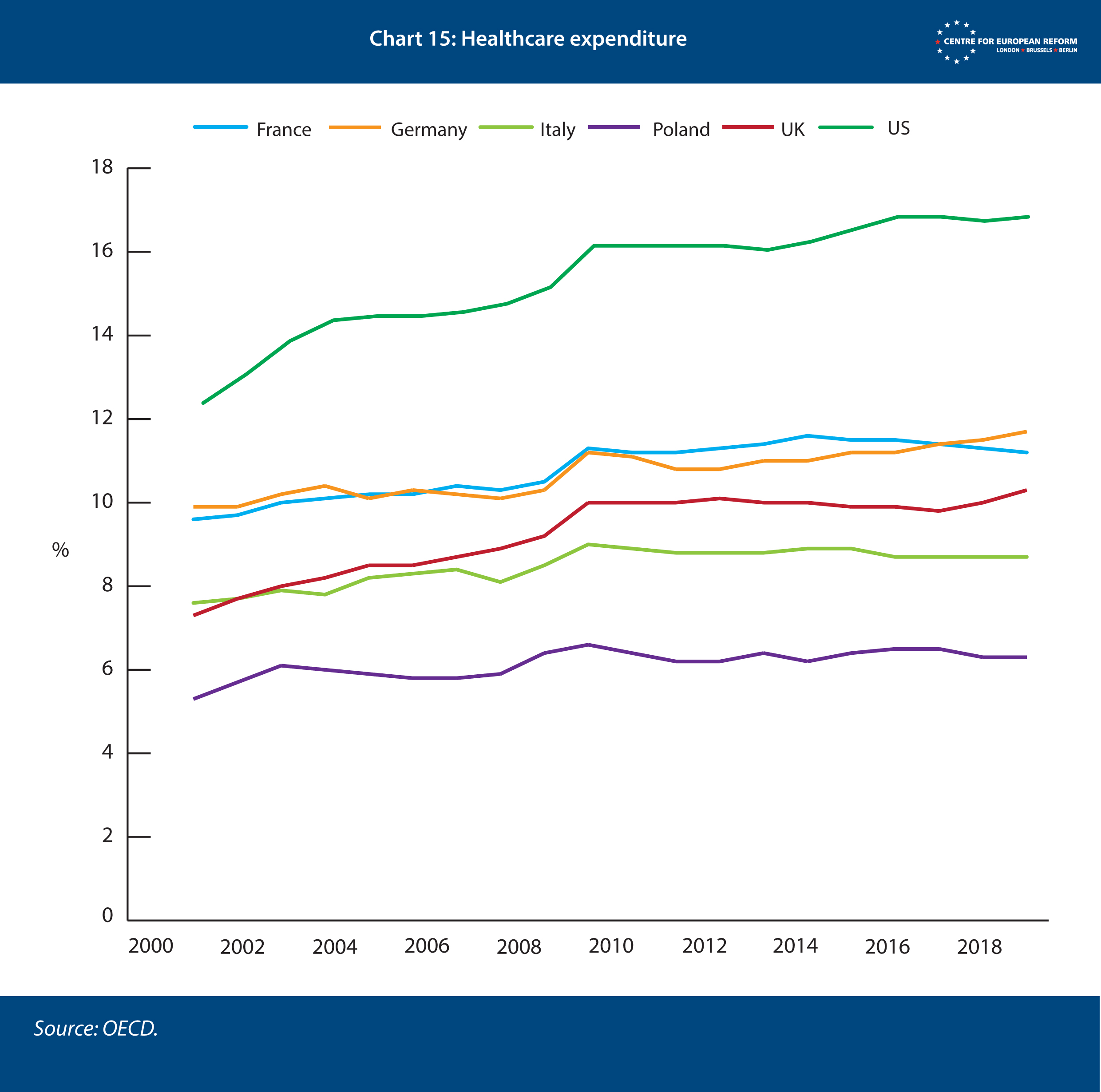

US healthcare is far more expensive than European provision. As Chart 15 shows, the US spends almost twice as much of its GDP on health as Spain and Italy and half as much again as Europe’s biggest spenders – France and Germany. After rising strongly in the 2000s, European healthcare expenditure remained pretty constant through the 2010s. With economic growth having been weak throughout the period while societies got older, this implies very tight control of spending. Growth in US healthcare also slowed, albeit from an already high base.

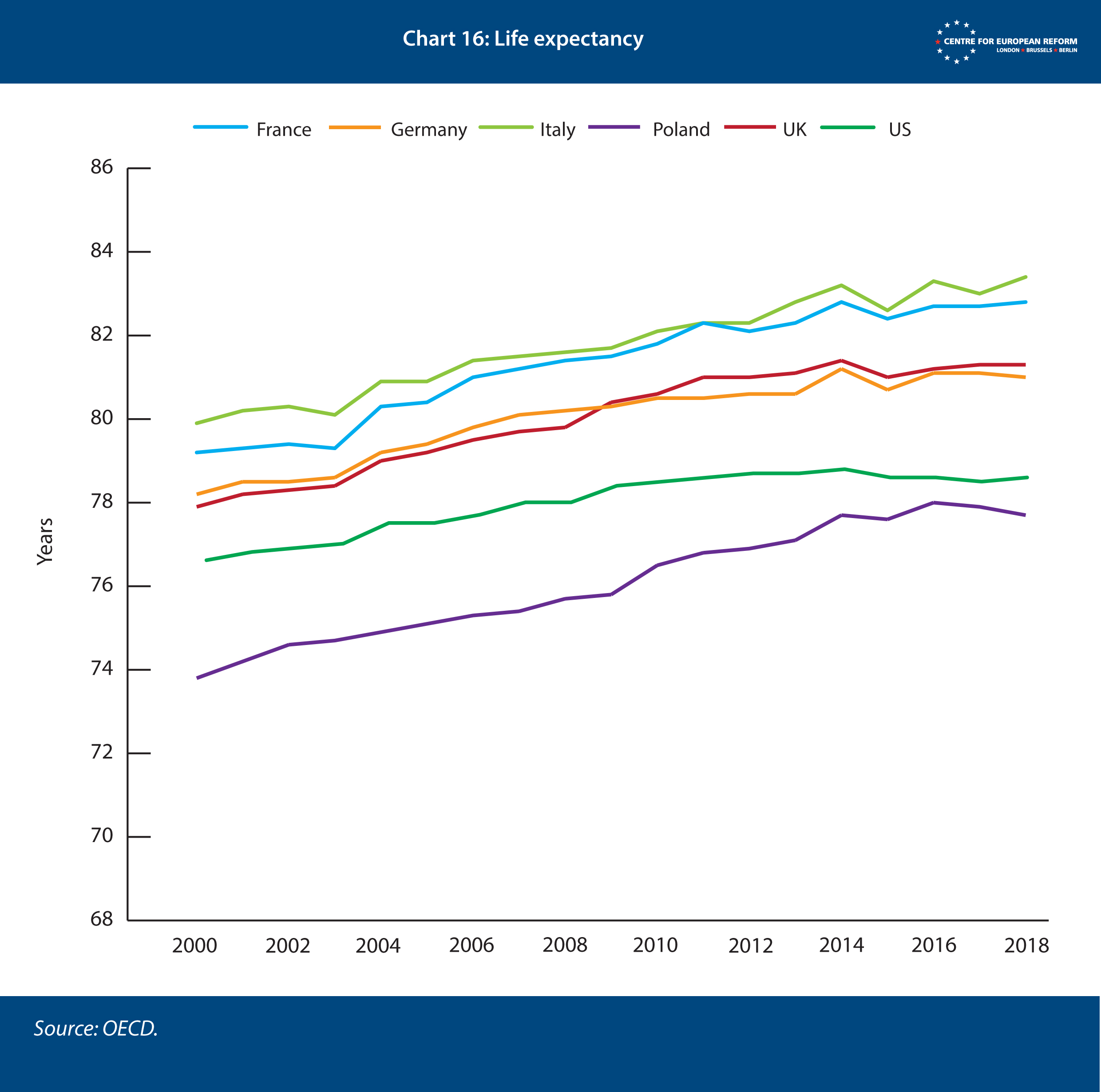

Higher US expenditure on healthcare is not reflected in better health outcomes. The most basic indicator of the healthiness of a country’s population is how long its inhabitants live. Life expectancy is markedly lower in the US than Europe, and the gap is growing (see Chart 16). Within Europe, there is no correlation between health spending and life expectancy; Italy and Spain spend the least on healthcare but have the longest life expectancy, while Germany spends the most and has the lowest.

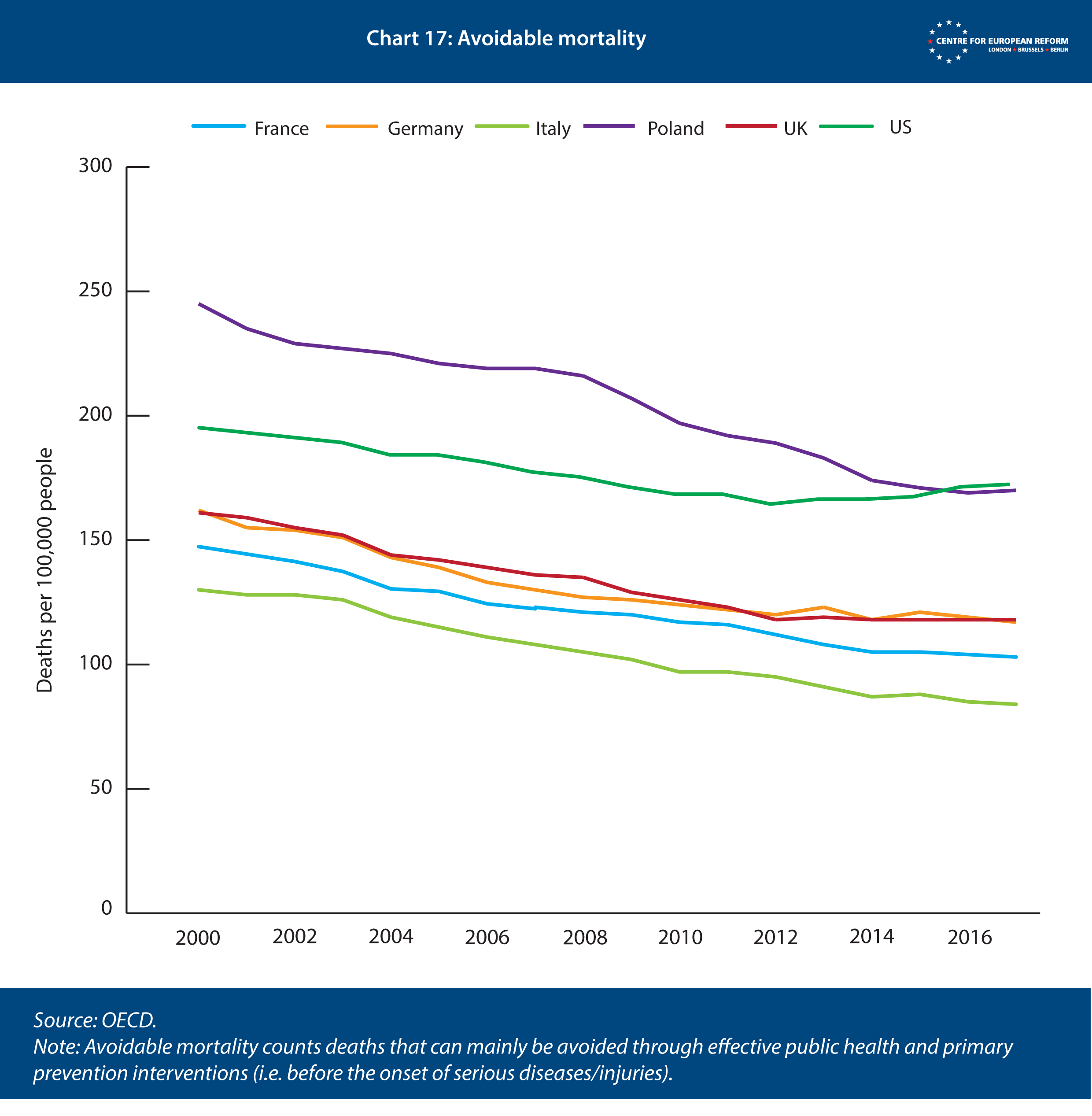

The principle reason for low US life expectancy is that Americans are, on average, unhealthier than Europeans, and becoming more so. Rates of ‘avoidable mortality’ – deaths that can mainly be avoided by effective public healthcare and primary prevention – are much higher in the US (see Chart 17). For example, Americans are more likely to die of circulatory and respiratory illnesses, or from glandular diseases, such as diabetes. Moreover, US infant mortality is two-thirds higher than in European countries with similar birth rates, such as France and the UK.

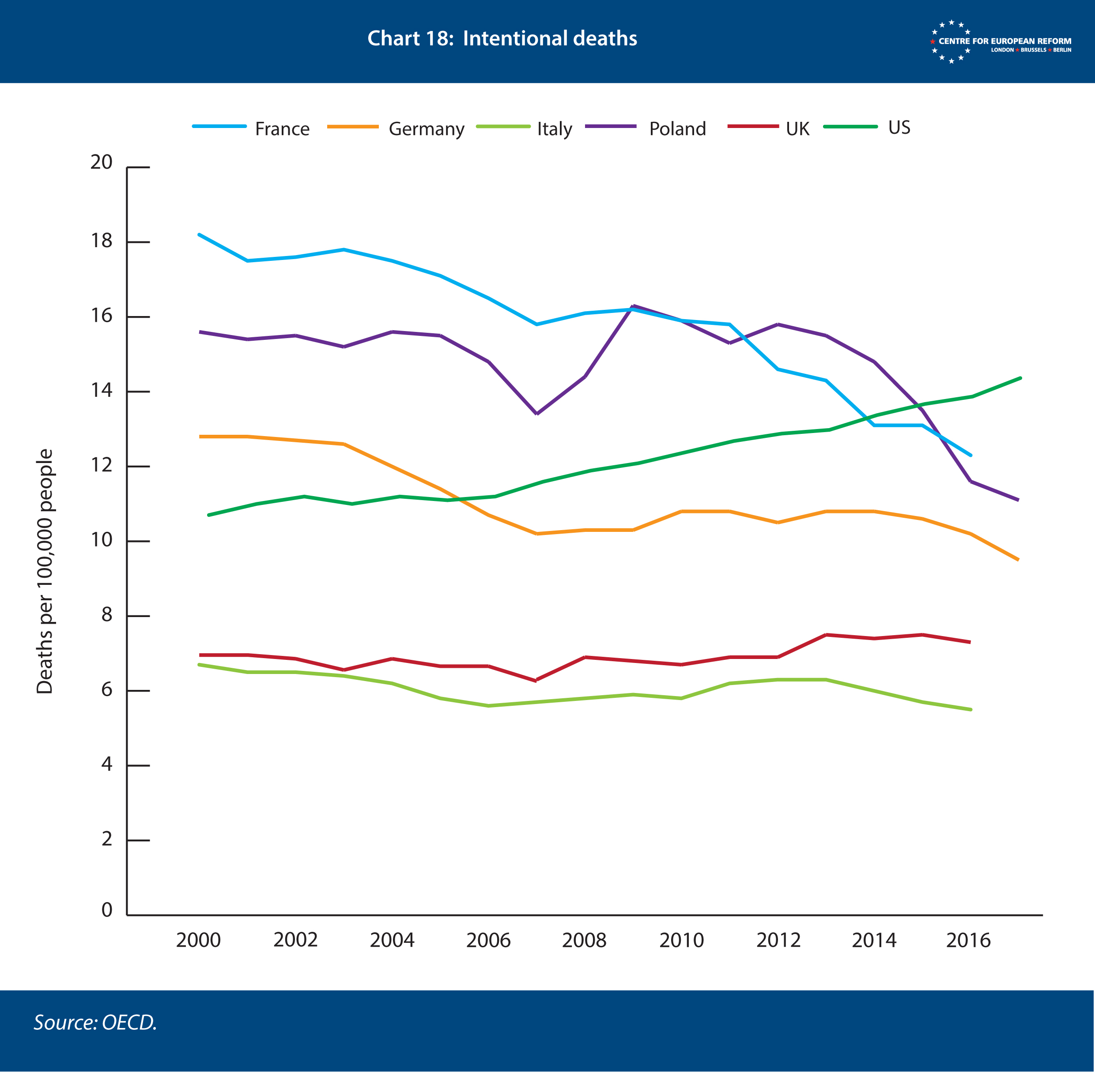

Suicides are also now more common in the US than in Europe. This was not always the case – 20 years ago US suicide rates were much lower than French or German ones. But they have risen steadily since then (see Chart 18). As Anne Case and Angus Deaton have shown, so-called ‘deaths of despair’ – deaths from opioid and alcohol addiction, as well as suicide – are driving this trend in the US. The group most affected is non-college-educated white men, whose working conditions and associated status have deteriorated sharply.14

There are a number of reasons why healthcare is more expensive in the US than in Europe. European governments or other public bodies play a big role in setting drug prices, the cost of medical equipment and hospital stays, as well as what treatments are available to patients. Prescription drugs cost on average twice as much in the US as in Europe.15 A knee replacement operation costs on average $29,500 in the US and $12,700 in the UK; an MRI scan $1,430 in the US, $450 in the UK and just $190 in the Netherlands.16 The cost of treatment also varies hugely across the US, with providers free to charge whatever the market will bear. Medicare and Medicaid are not permitted to negotiate prices with manufacturers, though private health insurers can.17 The complexity of the US system means that administrative costs are considerably higher – 8 per cent of total healthcare expenditure against 1-3 per cent in Europe.18 US medical staff, especially doctors, also get paid far more than in Europe, even after taking into account that average US salaries are higher than European ones.

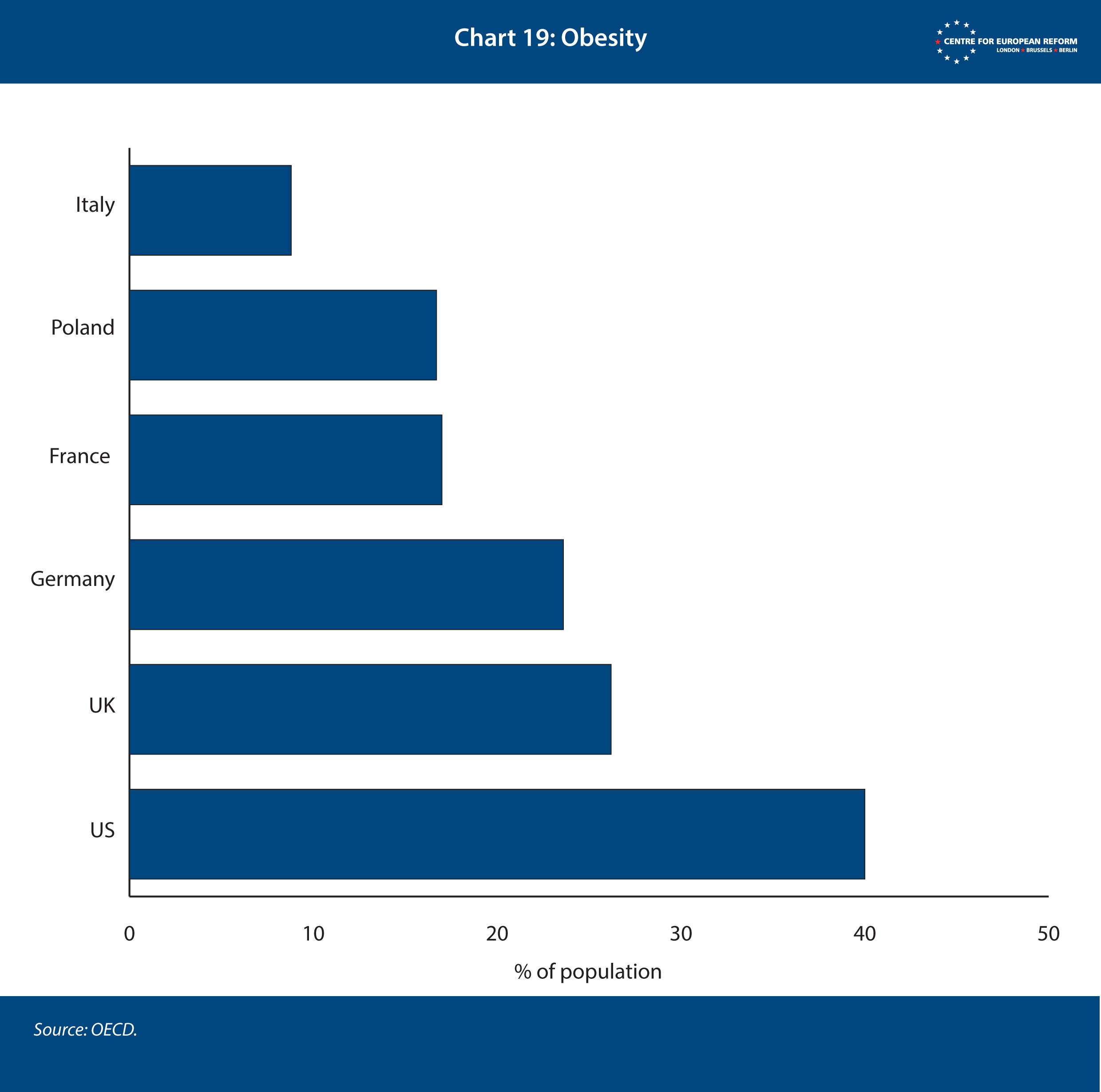

Inequality of access to healthcare mirrors higher inequality in the US as a whole. The prevalence of circulatory, respiratory and glandular illnesses reflects weak preventative healthcare but also obesity, poor diet and alcohol abuse, problems closely correlated with poverty levels (see Chart 19). Americans also have more sedentary lifestyles, walking less than their counterparts in other developed countries, as a result of greater urban sprawl and more limited public transport.19

High prescription drug prices in the US arguably cross-subsidise Europe’s much lower ones. If US prices were as low as in Europe, it is possible that drug firms would have weaker financial incentives to invest in new drug development. But the difference in drug prices between the US and Europe only accounts for around 15 per cent of the overall gap in healthcare costs.20

Going into the pandemic, then, Europeans’ health outcomes were much better than Americans’. But to what extent will severe recessions have an impact on public health? Perhaps surprisingly, many studies have found that recessions are linked to falling mortality rates in developed countries. The reason why is uncertain, but fewer deaths from cardiovascular and respiratory diseases may be down to lower exposure to pollution in periods of high unemployment, and fewer road deaths as commuting falls.21 Higher unemployment has been linked to lower alcohol consumption (probably because drinking is expensive) but more mental health problems and suicide.22

However, many of these studies look at the short-term links between unemployment and health outcomes. The COVID-19 pandemic will be bad for people’s health over the long term in two ways. First, many people who contract the disease need medical care. Some are hospitalised, and many who are not are reporting persistent health problems, including extreme fatigue, shortness of breath and neurological problems. Second, if the virus leads to markedly higher and persistent unemployment than previous recessions, people’s incomes will be lower, which reduces their ability to pay for healthcare. For a variety of reasons, European healthcare services are better able to cope with the long-term health consequences of the pandemic.

High and persistent unemployment in the aftermath of the pandemic will mean that fewer people will visit the doctor in the US.

The US healthcare system is a patchwork of private and public provision. People over 65 are covered by Medicare, a public insurance programme. Most people of working age receive private insurance through their employer, and those who are laid off because of the pandemic will lose their insurance. Those who fall into poverty will have access to Medicaid, a federal programme whose generosity is largely controlled by state governments. Before the Affordable Care Act – ‘Obamacare’ – was passed in 2010, many states restricted access to Medicaid to the poorest families and disabled people. Obamacare expanded Medicaid to all people with incomes below 138 per cent of the poverty level, but the Supreme Court ruled in 2012 that states could opt out of the expansion. To date, 13 states, mostly in the south, have done so.

By mandating and subsidising health insurance, Obamacare reduced the number of uninsured Americans from 50 million in 2010 to 27.5 million in 2018.23 In addition, an estimated 5-6 million undocumented immigrants do not have health insurance.24

The rapid rise in healthcare costs has led to increased use of cost-sharing with patients in the private insurance market. Visiting a general practitioner often costs more than $30 and a specialist doctor $45; and on average, insurance plans demand that patients pay for the first $1,600 of treatment before insurers take over.25 Such ‘deductibles’ are lower for older people on Medicare, but still over $1,000.

To plug the remaining gap in access to affordable healthcare after the pandemic began, Congress ruled that all public and private healthcare insurers eliminate patient payments for testing. The federal government would pay for uninsured people’s treatment if they fell ill with the disease, but those with private insurance would have to make co-payments as usual, up to their annual maximum, which can be more than $8,000 for an individual and $16,000 for a family.26

Inevitably, large numbers of uninsured people, and high co-payments for the insured, mean that unemployed people are less likely to visit a doctor in the US than in Europe. A Commonwealth Fund survey conducted in 2016 found that one-third of Americans said they had had a medical problem but did not visit a doctor, or skipped a medical test or treatment recommended by a doctor. In the UK, the Netherlands, Germany and France, the range was between 7 and 17 per cent.27 And the OECD found that the gap in doctor visits between the bottom 20 per cent of the US income distribution and the top 20 per cent was far larger than the OECD average.28

However, there are fairly wide differences between European countries in access to healthcare for rich and poor. In some countries, such as the UK and Sweden, patient co-payments are very low, while in others, health insurance providers require co-payments. But they are much lower than in the US, thanks to government subsidy and price regulations.

In summary, the US healthcare system provides highly unequal access to healthcare compared to the European norm. In part thanks to emergency legislation, unemployed and poorer Americans will have help with the costs of treatment for COVID-19, but many of the insured face large bills. High and persistent unemployment in the aftermath of the pandemic will mean that fewer people will visit the doctor in the US for other conditions, either because they do not have insurance, or because of high co-payments and deductibles. While co-payments weakened access to healthcare for many impoverished Europeans after the Great Recession, lower costs meant that the effect was much weaker. Given the extraordinary rise in costs in the US, high levels of income inequality, and highly unequal access to healthcare, it is not surprising that improvements in health outcomes had largely stalled before the pandemic. There is a risk that they will worsen further after the pandemic is brought under control.

Conclusion

There is too much uncertainty about COVID-19 to make firm predictions about its long-term effects. Hopes for a vaccine are rising, as developers in the US, China and Europe have found ways to stimulate human antibodies (although they have not yet demonstrated that their vaccines curtail infection). But successful vaccines will take time to be manufactured and deployed, and unemployment is likely to stay high in both the US and Europe in the interim, as hospitality, transport and leisure companies struggle to cope with continued social distancing measures.

The risks of the pandemic to the US are both immediate and long-term. Unless there is a rapid return to lockdown in many states, infections will continue to rise, around 1 per cent of cases will die, and another 4-5 per cent will be left with potentially long-term health problems. Withdrawal of emergency income support to businesses and households would lead to steep rises in bankruptcies, unemployment and poverty. And the healthcare system was already failing many citizens going into the pandemic: in its aftermath, if those who suffer long-term health problems do not receive support, many will leave the labour market. If the aftermath of the Great Recession is any guide, the US labour market will not be more effective at redeploying workers to contact-light sectors of the economy than Northern European countries, and it lacks the active labour market policies needed to retrain people and match them to employers. A resounding victory for Joe Biden in November may give him the mandate to expand healthcare and support for the unemployed, but the Republican Party will do all it can to stop him from sharing more risk between US citizens.

On the other hand, Europe fails to provide enough risk-sharing between member-states. The recovery fund is a welcome step, and if the pandemic ends quickly, it may be enough to stop Southern Europe’s debts from curtailing a recovery in consumption and labour demand. But as social distancing continues, private and public sector debt and unemployment will continue to rise. Eurozone macroeconomic risk-sharing is not automatic enough, other than through the European Central Bank, whose role in keeping borrowing costs low is contested.

If the pandemic endures, US and European politics will continue to be dominated by their respective federal weaknesses. Before COVID-19, greater risk-sharing at the federal level was difficult on both sides of the Atlantic, despite the strong case for it. Whichever side proves more able to do so – with the consent of electorates – will be the more stable polity in the decades to come.

2: ‘Coronavirus disease 2019 case surveillance – United States, January 20th-May 30th, 2020’, Centers for Disease Control and Prevention, June 2020.

3: Leonardo Burzstyn and others, ‘Misinformation during a pandemic’, National Bureau of Economic Research, June 2020.

4: Automatic stabilisers stimulate the economy when it slumps, without the need for direct intervention by government.

5: Julia Anderson and others, ‘The fiscal response to the economic fallout from the coronavirus’, Bruegel, July 2020.

6: As of the end-June.

7: Jérémie Cohen-Setton and Jean Pisani-Ferry, ‘When more delivers less: Comparing the US and French COVID-19 crisis responses’, Peterson Institute for International Economics, June 2020.

8: The US Cares Act is a $2 trillion federal stimulus agreed at the end of March. It comprises loans to business, increased unemployment insurance, direct payments to households and packages of financial support for particularly hard-hit industries.

9: Stephen Clarke and Nye Cominetti, ‘Setting the record straight: How record employment has changed the UK’, Resolution Foundation, January 2019.

10: Two good overviews are Shigeru Fujita and others, ‘The labour market policy response to COVID-19 must save aggregate matching capital’, VoxEU, March 30th 2020; Eduardo Levy Yeyati and others, ‘Life after coronavirus: Strengthening labor markets through active policy’, Brookings Institution, April 2020.

11: Christian Odendahl and John Springford, ‘Three ways COVID-19 will cause economic divergence in Europe’, CER policy brief, May 2020.

12: Tomas Hirst, ‘Euro strategy: Recovery fund clears first hurdle’, Credit Insights, July 21st 2020.

13: ‘Economic outlook’, OECD, June 2020.

14: Anne Case and Angus Deaton, ‘Deaths of despair and the future of capitalism’, Princeton University Press, 2020.

15: ‘A powerful pill to swallow: US vs international prescription drug prices’, US House, May 2020.

16: ‘The nation’s healthcare dollar: Where it came from’, Healthcare Cost Institute, 2018.

17: Medicare is a federal health insurer for Americans over 65 years old, and for some younger people with disabilities. Medicaid provides coverage to eligible low-income adults, children, pregnant women, elderly adults and people with disabilities.

18: ‘Healthcare spending in the United States and other high-income countries’, Journal of the American Medical Association, May 2020.

19: DR Bassett and others, ‘Pedometer-measured physical activity and health behaviors in US adults’, Medicine and Science in Sports and Exercise, October 2010.

20: ‘Healthcare spending in the United States and other high-income countries’, Journal of the American Medical Association, May 2020 ; CER calculations.

21: Douglas Miller and others, ‘Why are recessions good for your health?’, American Economic Review, May 2009.

22: Sara Evans-Lacko and others, ‘The mental health consequences of the recession’, PLOS One, July 2013; ‘Health at a glance’, OECD, 2011.

23: Jennifer Tolbert and others, ‘Key facts about the uninsured population’, Kasier Family Foundation, December 2019.

24: Samuel Dickman and others, ‘Inequality and the health-care system in the USA’, The Lancet, April 2017.

25: Kaiser Family Foundation, ‘Benchmark employer survey finds average premiums now top $20,000’, September 2019.

26: Jamie King, ‘COVID-19 and the need for health care reform’, New England Journal of Medicine, June 2020.

27: The Commonwealth Fund, ‘International health policy survey of adults’, November 2016.

28: OECD, ‘Health for everyone? Social inequalities in health and health systems’, 2019.

John Springford, deputy director, Centre for European Reform and Simon Tilford.

This research was supported by MSD. The views expressed are those of the authors, not MSD.

View press release

Download full publication

Related content

CER podcast: The EU's €750 billion question: How should the COVID-19 recovery fund be spent?

Trump's COVID-19 response is deepening the transatlantic rift

The recovery fund faces a tricky passage

Securing Europe's medical supply chains against future shocks

Three ways COVID-19 will cause economic divergence in Europe