Leave your phone at home: Why EU roaming charges will only increase for UK consumers

Will the end of free EU roaming make the UK mobile market fairer, as some economists claim? Don’t bet on it.

British consumers have become accustomed to using their mobile phones without incurring any additional charges while visiting the EU. Prominent Brexiters, such as British justice secretary Dominic Raab, promised that free roaming in the EU for UK consumers would continue after Brexit. But three of the four major UK mobile network operators have recently announced the return of roaming charges. The proposed charges are modest, and The Economist argues they will actually make the UK mobile market fairer – because consumers who do not roam will no longer have to cover the costs of those who do. But it is wishful thinking to expect the UK market to become fairer overall. More likely, price-sensitive consumers will simply give up the convenience of roaming, and UK consumers who still roam will be lumped with high charges. The UK cannot solve this problem unilaterally: any solution needs an agreement between the UK and the EU.

Price-sensitive consumers will simply give up the convenience of roaming, and UK consumers who still roam will be lumped with high charges.

How roaming works

In order to understand how Brexit affected roaming charges, it is necessary to understand that there are two distinct markets that influence how much consumers pay when roaming.

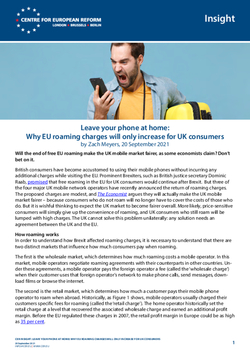

The first is the wholesale market, which determines how much roaming costs a mobile operator. In this market, mobile operators negotiate roaming agreements with their counterparts in other countries. Under these agreements, a mobile operator pays the foreign operator a fee (called the ‘wholesale charge’) when their customer uses that foreign operator’s network to make phone calls, send messages, download films or browse the internet.

The second is the retail market, which determines how much a customer pays their mobile phone operator to roam when abroad. Historically, as Figure 1 shows, mobile operators usually charged their customers specific fees for roaming (called the ‘retail charge’). The home operator historically set the retail charge at a level that recovered the associated wholesale charge and earned an additional profit margin. Before the EU regulated these charges in 2007, the retail profit margin in Europe could be as high as 35 per cent.

Both the wholesale and retail markets suffer from poor competition, however, leading to unfair pricing practices.

In the wholesale market, it costs a mobile operator very little to allow a foreign network’s customer to roam on its network; the cost is barely different from that of serving a domestic customer. But the wholesale market has unusual features, which have kept those wholesale charges unjustifiably high. For example:

- There are typically only between two and four mobile operators with their own network in each EU member-state. This means few businesses compete to offer roaming to their foreign counterparts.

- Mobile operators may take incentives other than price into account. For example, many operators are part of multinational groups. Such operators may be reluctant to offer low wholesale roaming charges to foreign operators that compete domestically with their own overseas affiliates. This further reduces competition.

- Mobile operators prefer to send traffic to roaming partners that will reciprocate with a similar amount of traffic in reverse. This means the negotiated wholesale price for reciprocal traffic does not impact either operator’s profitability. Therefore, in the absence of regulation, mobile operators have an incentive to agree high rates with each other for reciprocal traffic, in order to justify high retail charges. Mobile operators often agree to charge each other a different, lower, price only for the portion of their roaming traffic which is not reciprocated.

The retail market also suffers from imperfect competition. Most customers do not travel overseas often, and roaming prices are rarely an important factor when they choose their mobile operator. In general, mobile operators therefore have historically faced little pressure to reduce their retail roaming charges.

How have UK roaming charges changed since Brexit?

As a result of these market failures, the EU started imposing caps on wholesale and retail charges from 2007. These became more stringent over time. Retail charges across the EEA were largely abolished in 2017 as part of the EU’s ‘Roam Like At Home’ initiative.

The UK government initially said that Brexit would not change these arrangements, even if the UK left the single market and the UK and EU failed to agree a trade deal. Although there was a deal, the UK-EU Trade and Co-operation Agreement included no wholesale or retail caps: it only committed the parties to “endeavour to cooperate” on promoting “reasonable” roaming rates.

The UK could not sensibly keep its promise that UK consumers would not pay for EU roaming. EU operators are now free to raise wholesale charges for UK operators (and vice-versa). This means that UK operators should be able re-impose retail roaming charges to cover any higher wholesale costs – otherwise, all UK mobile services would become more expensive.

The UK government’s promise that UK consumers would not pay for EU roaming could not be kept.

But rather than address this narrow problem, the UK government took a deregulatory approach and removed any limits on retail roaming charges. Three of the UK’s largest mobile operators – Vodafone, EE, and Three – have now introduced retail charges. O2 has reduced customers’ roaming allowances but has not yet increased prices.

Should the return of roaming charges be welcomed?

Counterintuitively, The Economist, and some other commentators, have welcomed the return of roaming charges. They argue that free roaming raises prices for consumers who do not use roaming – because mobile operators’ wholesale costs have to be recovered from all customers.

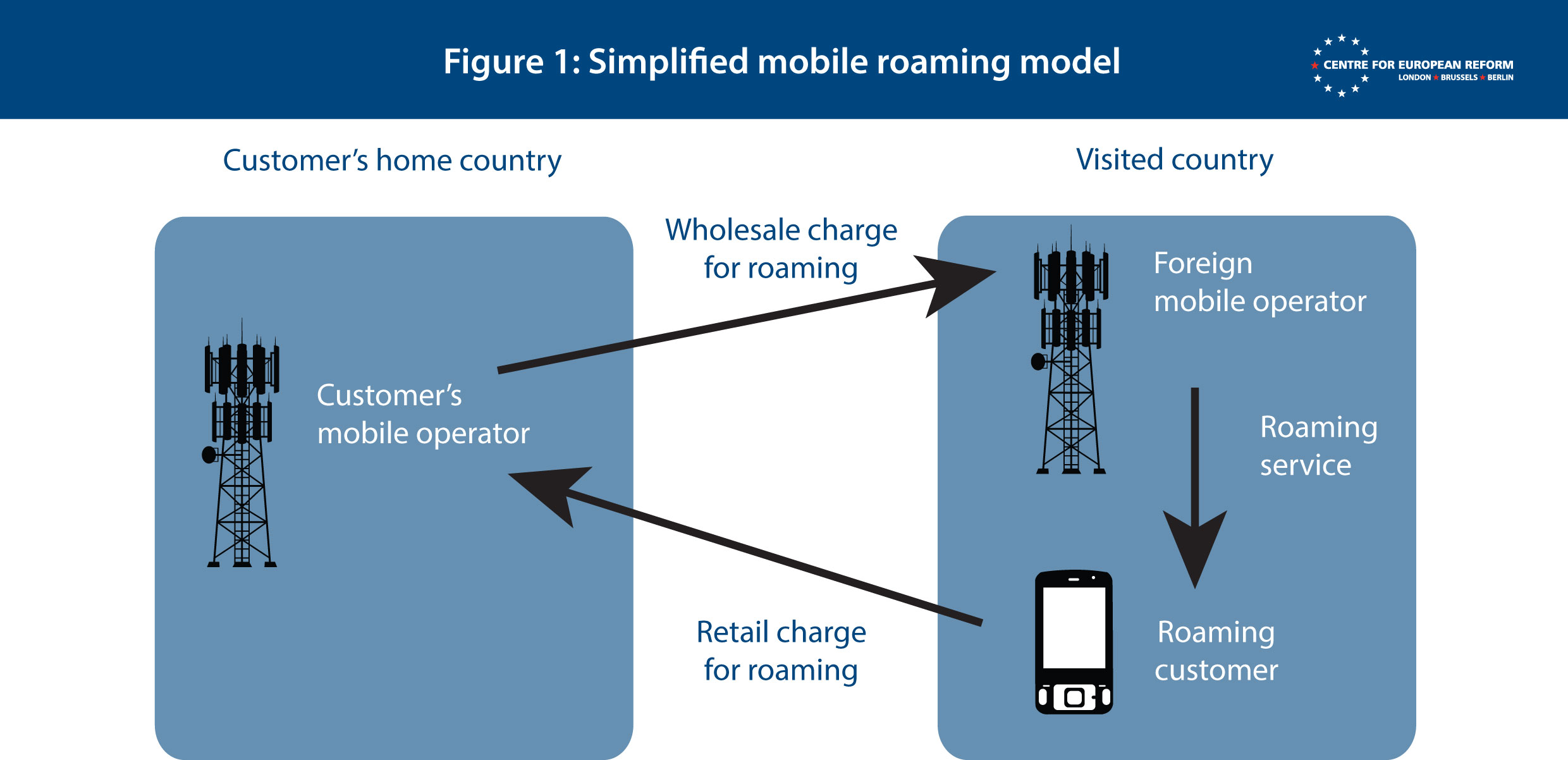

This argument is not wrong but its impact is overstated. First, roaming comprises only a small proportion of European operators’ overall traffic. Second, the EU roaming regime includes ‘safety brakes’ to stop abuse by the most prolific users of roaming services and to protect operators for whom roaming could become unsustainable. Third, while customers who do not roam subsidise those who do, the size of that cross-subsidy depends on the wholesale charges an operator actually incurs to provide roaming. The EU has already regulated wholesale charges to a low level; actual prices have decreased even further (see Chart 1 below); and the EU plans to drive down the cap on wholesale charges down even further in future. Any cross-subsidy is therefore already small and continuing to shrink.

Removing this cross-subsidy entirely is only beneficial for UK consumers overall if wholesale charges remain low, and retail mark-ups are reasonable. This will only happen if EU regulation has become unnecessary and market forces alone keep prices low. Unfortunately, the evidence for this assumption is weak.

Why wholesale charges could increase

The Economist suggests that competition between mobile operators in each EU member-state is sufficiently high that operators will compete to attract UK mobile operators’ roaming traffic. In theory, this would drive down wholesale charges and remove the need for regulation.

Chart 1 shows that the evidence for this theory is at best ambiguous:

- In support of this theory, competition has driven wholesale charges in the EU well below the regulated maximum. This is probably because the roaming regulation has encouraged consumers to use roaming, put pressure on mobile operators to negotiate low wholesale charges with each other (since operators can no longer recover high fees from retail roaming charges), and higher roaming volumes have made it more attractive for operators to provide roaming to each other.

- Against this theory, Chart 1 also shows that wholesale charges still remain somewhat above authorities’ upper estimates of the costs of providing roaming, with wholesale profit margins of at least 22 per cent for data and 16.5 per cent for calls. This suggests that competition is still not fully effective. Furthermore, Chart 1 also shows that the unregulated charges which EEA operators levy on non-EEA operators remain very high. There is therefore potential for very significant wholesale charge increases without regulation to prevent that outcome.

At the very least, there is a real risk that wholesale charges will increase for UK operators and converge with the wholesale charges for other non-EEA countries. EU operators could charge UK operators more, knowing that UK operators could once again pass on higher EU wholesale charges directly to consumers through retail roaming charges. Operators will once again be able to act on their incentives to set high prices for reciprocal traffic, to justify higher retail prices – in Poland, for example, the major operators have already signalled that they will charge consumers for roaming in the UK in future. Finally, retail roaming charges mean that UK consumers will reduce their use of roaming to some extent – for example, by relying on less convenient alternatives like Wi-Fi hotspots when travelling – making it less attractive for foreign operators to compete for UK operators’ roaming traffic. Collectively, these factors may lead to higher wholesale charges. That would cause even higher retail charges, as UK mobile operators would try to maximise profits from those customers who will continue to use roaming services even at high rates.

Why retail charges could increase, even if wholesale charges don’t

Even if wholesale charges have not increased – and do not increase in future – UK mobile operators may also increase their retail mark-ups on roaming charges. Whether they can profitably do so largely depends on whether UK customers will now treat roaming prices as an important factor in their choice of mobile operator.

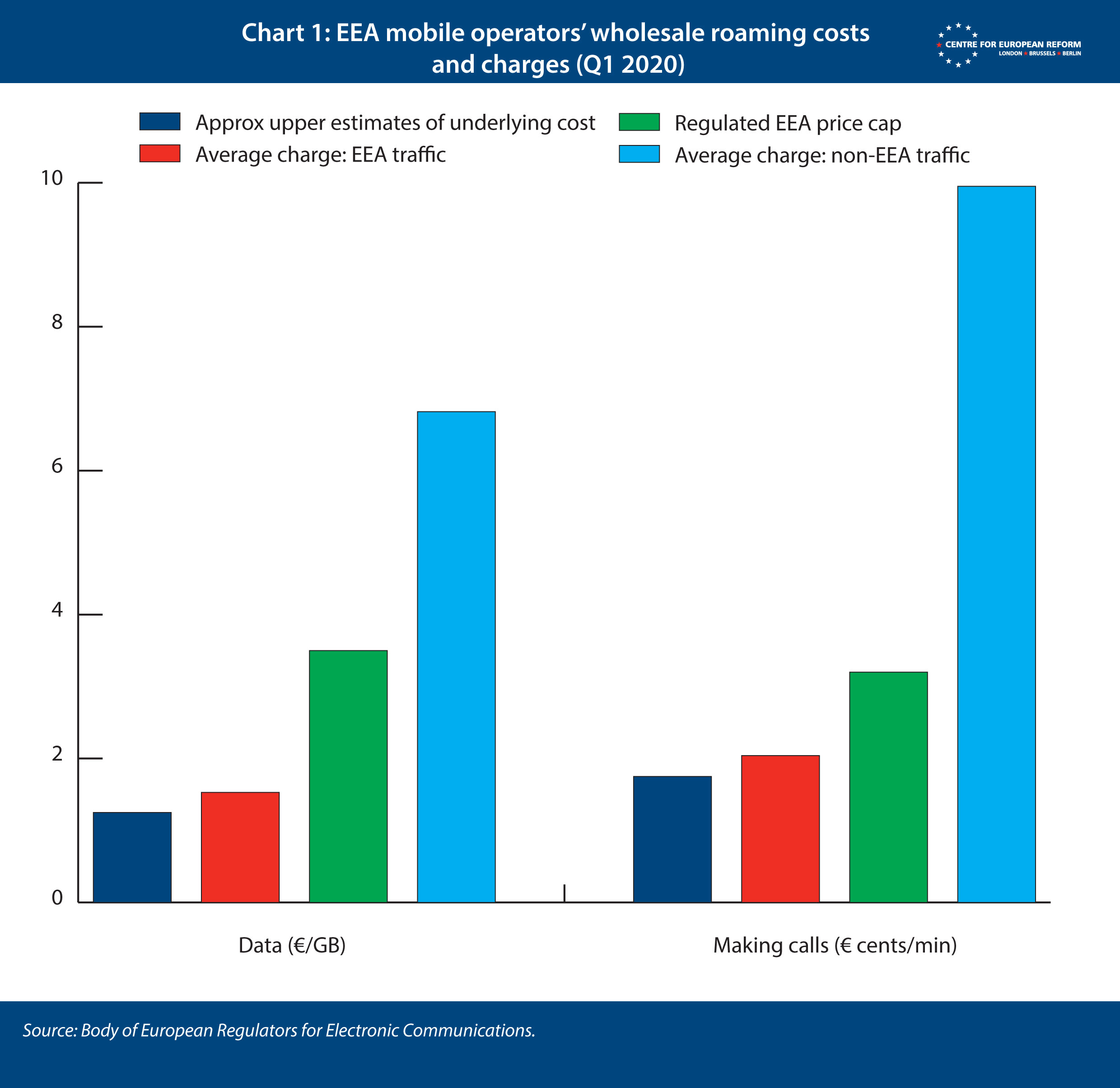

There is not yet much evidence that UK customers’ behaviour will be sufficient to keep retail roaming charges at the levels mobile operators have now proposed. As Table 1 shows, the UK’s mobile operators charge much more for roaming in the most popular travel destinations outside the EEA (other than Switzerland) than for roaming inside the EEA. Table 1 also shows that charges and pricing structures vary significantly between operators, and sometimes country-by-country, making it impossible for consumers to compare prices easily, especially for consumers who do not know where they are likely to travel when they are signing up for a new mobile contract.

When UK mobile operators re-introduced roaming recently, their explanations implied the new roaming charges represented increased mark-ups. If the UK operators were merely passing on higher wholesale charges, they probably would have justified the price increases publicly on that basis. Instead, Vodafone, EE and Three pointed to either future “uncertainty” about wholesale charges or the need to raise revenue to fund domestic investment. Furthermore, Three took the opportunity to increase prices not just for EEA destinations, but for non-EEA destinations too, where wholesale prices are unlikely to be significantly affected by Brexit. Three previously distinguished itself from its competitors by offering free roaming to many destinations outside the EEA at no additional cost. The removal of this offer suggests that it is simply not worthwhile for mobile operators to compete to drive down retail roaming charges, and it makes more sense to extract high profits from those customers who will pay high prices for roaming.

What the UK government should do now

The EU’s Roam Like At Home arrangements are imperfect, because of the cross-subsidy they impose between customers who roam and those who do not. There are some simple improvements that the EU could make to improve those arrangements, such as granting mobile operators more scope to prevent consumers from using free roaming services excessively. But the EU regime’s problems are overstated and the UK’s deregulation is not a better solution. Competition law is unlikely to be a good alternative to regulation either: the problem is an international one and involves vast numbers of different mobile operators across different countries. Competition law is slow in dealing with these types of cases, and claims about excessive pricing are notoriously difficult to win.

The British government, or the UK telecoms regulator Ofcom, could regulate the retail market. Either of them could require that UK mobile operators limit their retail roaming charges. Such regulation must allow UK operators to pass on wholesale charges to their consumers, while prohibiting any excessive retail mark-ups. That at least might have prevented the current round of price increases, which were not an inevitable outcome of a hard Brexit.

Domestic regulation cannot, however, prevent UK mobile operators being overcharged by European operators or vice-versa – so a hard Brexit will probably be responsible for future price increases. Britain cannot unilaterally regulate the behaviour of foreign operators or the prices those foreign operators offer for services delivered in their own countries. The UK Government should therefore overcome its reluctance to propose new roaming caps with the EU. The European Parliament has already called for the preservation of free UK-EU roaming after Brexit. The EU is also studying options to secure free roaming between the EU and the Western Balkans and Eastern Partnership countries in future. Given the long road towards single market membership for these countries, and the existing commitment to co-operation in the UK-EU TCA, the EU cannot claim that it will only contemplate cross-border price caps with countries in the single market.

Domestic regulation cannot prevent UK mobile operators being overcharged by European operators or vice-versa – so the Brexit deal will probably be responsible for future price increases.

Some in the EU no doubt see the end of free roaming as an important, visible symbol of the harm caused to the UK by Brexit. But cooler heads should recognise that free, or at least low-cost, roaming will help to maintain close social and economic ties between the UK and the EU. Such ties will be essential to improving political and economic relations between the UK and the EU over time.

Zach Meyers is a research fellow at the Centre for European Reform.

Comments

Telecom infrastructure in the UK is good, but should be a whole lot better. We need lots more fibre to the home, lots more 4G coverage in rural areas, lots more 5G in urban areas and better bandwidth to cope with rapidly growing data demand.

This requires investment to build out the infrastructure, and the investment requires rational pricing by the market participants to generate reasonable returns to justify investment. Rational pricing includes charging higher prices for a better product, and charging for value added services like roaming. This is commerce at its most basic.

The EU roaming regulations on the other hand, are a neat example of irrational pricing. Why were the regulations to eliminate roaming charges introduced in the first place? How did this piece of single market "improvement" come about?

The grubby story outlining the history of EU roaming reforms is laid out by a former Commission spokesperson Ryan Heath in a Politico article from a few years ago. It's well worth a read.

As Ryan outlines, there is no heroes in the EU roaming story, just European Commissioners ganging up with MEPs to bludgeon an industry with artificial price controls in order to build a political message to EU citizens growing increasingly indifferent to the EU. Oh, and to create a "legacy" for a soon-to-retire Commissioner. As Ryan puts it, the effort was one of "policy-based evidence-making" - i.e. make up evidence to justify a pre-determined evidence-free policy. The initiative was 100% Commission politics, 0% single market economic reform.

Meanwhile in 2021, Politico reports that when the pandemic struck in Germany the poor quality telco network required COVID stats to be collected by fax, and homeworking and schooling were handicapped by chronic under investment in telecommunications. A German photographer found he could transfer data faster on horseback with DVDs than sending via the broadband network. Still, as he galloped on the horse with the DVDs he must have been comforted by knowing he had all that free EU roaming.

Major European telco providers operate networks in the UK as well as the EU. If Vodafone, Telefonica and Deutsche Telecom decide they get better returns from diverting investment from price-capped EU networks to market-priced UK networks, leading to me getting better home and mobile broadband, I'm more than happy to pay £2 a day to check social media from a holiday sun lounger in Spain.

What seems odd is how the mobile phone market all follow each other like lemmings - why are there no offers for a higher monthly charge but with roaming included?

What is the position in Northern Ireland? Presumably they are in the happy position of being subject to the EU regulations.

- O2: Yet to reintroduce EU roaming charges, already offer premium plans with inclusive roaming to US, Canada, Australia, New Zealand and others

- Three: re-introduced EU roaming charges, yet to launch premium plan with inclusive romaing

- Northern Ireland treated the same as all other parts of the UK. Re-introduced EU roaming charges exclude Ireland (Republic of) to prevent accidental roaming charges incurred by Northern Ireland residents.

- All UK consumers can set manual bill caps control maximum monthly charge from premium mobile services including roaming

- All UK consumers protected from automatic bill caps to prevent bill shock from premium services including roaming

Drama about reintroducing UK roaming charges is a storm in a teacup.

Commission now plans to mandate global consumer electronic manufacturers as to what port technology they must use on devices. This is also a terrible idea, which will lead to further outcomes unhelpful to Europe's digital growth.

Add new comment