Public investment: A modest proposal

Last Wednesday Jean-Claude Juncker, the president of the European Commission, announced his plan to create a €315 billion ‘European Fund for Strategic Investment’ to try to stimulate the European economy. It will take the form of an investment fund; €21 billion will be taken from the EU budget and the European Investment Bank to act as the fund’s capital. This will be used to offer guarantees that will reduce risk for private investors. The hope is that this will stimulate private lending to infrastructure and research and development, and take the value of investment over €300 billion.

That figure looks impressive, but the fund is unlikely to have much impact on growth. This is because it has been designed to avoid any new public borrowing for investment. There is no new public spending – pre-existing funds are being shuffled into the programme. So new spending will have to come as a result of loans from the private sector. Juncker hopes that the capital of the fund can be ‘leveraged’ by 15 times, meaning that the value of private lending will dwarf the public capital that has been committed. This would be double the leverage ratio of the European Stability Mechanism, and infrastructure investments are often more risky than lending to governments, which should reduce private investors’ willingness to lend to the fund. Finally, member-states can inject more capital into the fund if they wish, and these investments will be excluded from their deficit targets under the eurozone’s fiscal rules. But they are unlikely to do so, since the European Investment Bank will pick the projects that will be funded, and so governments’ capital will be mostly used in other member-states.

It may seem pointless to argue for a more sensible investment strategy, since it would require counter-cyclical government investment of the type that the eurozone has repeatedly rejected. But the case for such a strategy is strong. Instead of fiddling with financial engineering, eurozone member-states should simply borrow money directly from the markets and invest it themselves. There is little need for the Commission or European Investment Bank to be involved. Member-states need to co-ordinate on the size of the stimulus – Germany providing some stimulus on its own will not be enough – but they do not need a common instrument to do so. The eurozone is in the last-chance saloon: unless it starts to grow, and unless inflation rises, public sector debt will become uncontrollably large in some member-states. And, counter-intuitively, more public investment would reduce the burden of debt, not raise it.

The eurozone economy has stagnated for three years: in real terms, it is now slightly smaller than it was in the first quarter of 2011, and is still 2 percent below its peak in the first quarter of 2008. Inflation is very low, at 0.4 per cent. Unemployment is stuck above 11 per cent. But policy-makers have done little in response. Mario Draghi, the president of the European Central Bank, has continued to try to improve inflation expectations through talk rather than through action: the ECB is yet to embark on quantitative easing.

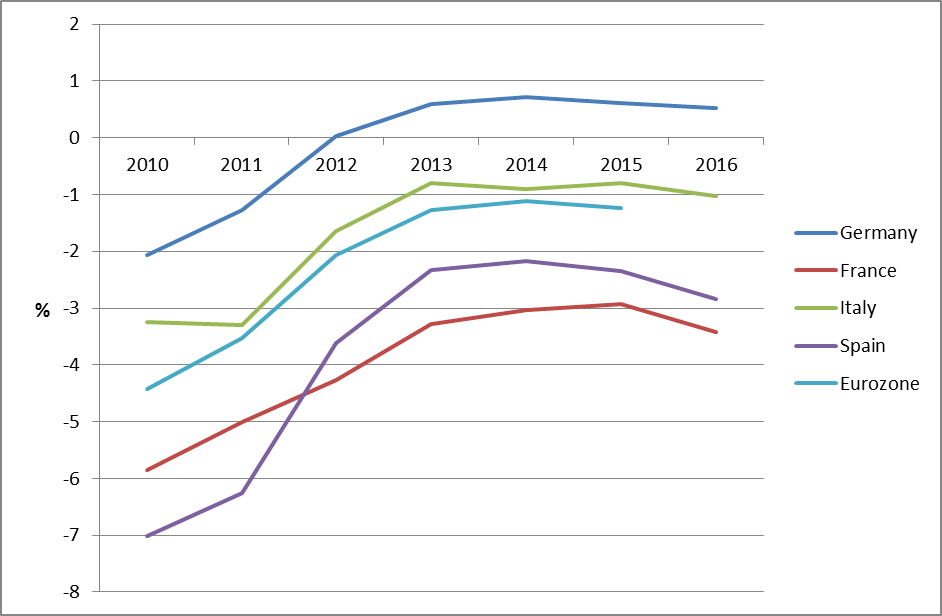

Meanwhile, eurozone countries remain committed to fiscal targets (limiting structural budget deficits – the deficit adjusted for the economic cycle – to below 0.5 per cent) that tightly circumscribe their freedom to go for a fiscal stimulus. Fortunately, fiscal policy will contribute a little to growth across the eurozone between 2015 and 2016, as France, Italy and Spain have successfully won more time to comply with these rules (see Chart 1). However, there is no indication that the eurozone is close to launching a meaningful fiscal stimulus.

Chart 1. Eurozone structural government deficits

Member-states should not merely stop digging. The eurozone needs a fiscal boost, alongside more unconventional monetary policy, to kick-start growth and raise inflation. As ever, the biggest obstacle to such a programme is Germany, which has been facing increasingly desperate calls to stimulate the eurozone economy through a programme of public investment at home. It has been running down its infrastructure for over a decade. It can borrow money, essentially for free, since yields on its long-dated debt are lower than expected inflation.

Berlin’s stock response is that a German investment stimulus would do little to boost the eurozone economy as a whole. They point to research that suggests the impact of a German programme of fiscal stimulus on other member-states would be small. According to the ECB, a 1 percentage point increase in German government spending would only boost French GDP by 0.03 per cent.

However, other researchers have shown that the spillover effects would be bigger. In a 2013 paper, Jan in’t Veld, an economist at the European Commission, questioned the method of studies that found little benefit for Germany going it alone. He pointed out that they did not include important factors that would make their models more realistic under current conditions: a far larger proportion of households than usual lack access to credit, for example, and the ECB’s interest rates are effectively at zero. When these factors were included in the model, the spillovers were higher, at between 0.2 per cent for France, Italy and Spain, rising to 0.3 per cent for Ireland. The IMF found that the effect would be of a similar size. This suggests that a German stimulus would have a moderate impact on output in other countries, and is worth pursuing for both domestic reasons and for the benefit of the eurozone as a whole.

However, as the Oxford University economist Simon Wren-Lewis notes, a fiscal stimulus in the eurozone would be more beneficial the more countries participated in it. To understand why, consider the effect on GDP of the eurozone’s co-ordinated austerity programmes since 2010. In’t Veld found this effect to have been very large. In Germany, Ireland and the rest of the eurozone ‘core’ of Belgium, the Netherlands, Austria and Finland, simultaneous austerity more than doubled the impact on output compared to austerity pursued alone. In France, Italy and Spain – larger economies that are slightly less open to trade – the impact was around 40 per cent bigger. Why is that the case? Austerity leaks into other member-states, since it reduces demand for other eurozone member-states’ exports. If a member-state cuts its deficit alone, reducing demand for imports, that reduced demand is shared across its trading partners, which makes the effects fairly modest. But if every country imposes austerity at the same time, the effect on imports is much larger. The obvious lesson is that simultaneous fiscal stimulus (as opposed to rectitude) will have much larger effects on output than if Germany acted alone.

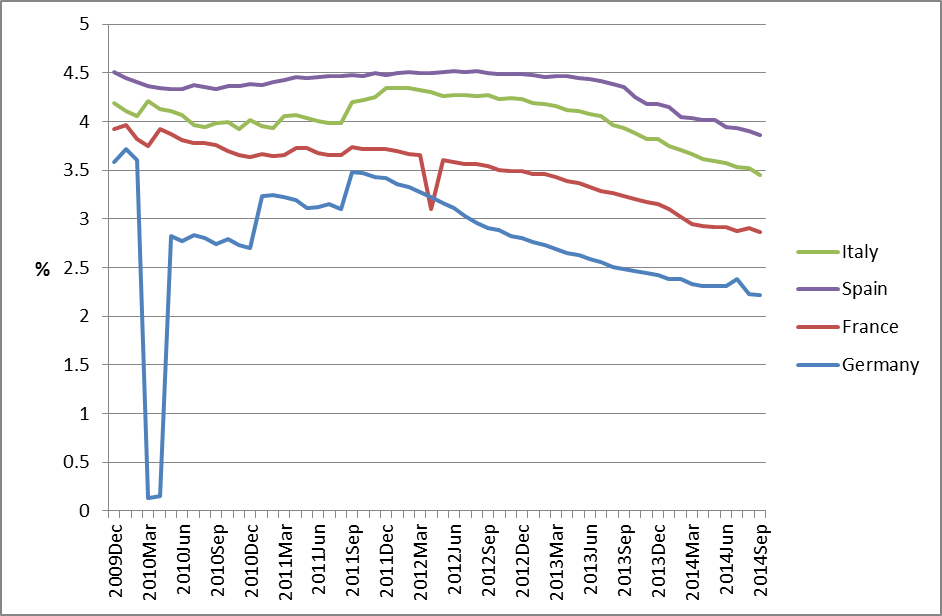

Many in Frankfurt, Berlin and Brussels argue that any co-ordinated stimulus beyond the core would be far too risky, since the ‘periphery’ cannot afford to take on more debt. But the ECB, through its ‘Outright Monetary Transactions’ programme, has reduced the risk that a country might be forced to leave the eurozone, at least for now. It has promised to act as a lender of last resort to eurozone governments – which brings the eurozone into line with other developed countries – and as a result, borrowing costs for governments have fallen. Chart 2 shows the average interest rate on existing stocks of government debt. Government borrowing costs have fallen rapidly since 2012, with Italy and Spain’s average debt service costs as low as Germany’s were in 2009. These countries do not face a funding crisis.

Chart 2. Average interest rate on stock of existing debt

Now that the ECB has given the eurozone the chance to pursue a broad-based fiscal stimulus, it should use it. The most sensible thing to do would be to invest in energy, transport, digital networks and other forms of infrastructure. Public spending in these areas has a high ‘multiplier’ – meaning that it raises GDP by more than tax cuts or other forms of spending. This is because little of the money is saved, as with tax cuts. Moreover, government investment leads to higher levels of private investment. A new road linking businesses and consumers, or employers and workers, will create economic activity.

There is not a shortage of things to invest in, especially in Italy and Germany. The quality of Italian infrastructure is far lower than its competitors: the IMF gives it 3.9 out of 7 compared to France’s 6.4. The quality of Germany’s infrastructure is high, but has been falling steadily since 2006 – especially its roads, which are now at the G7 average.

The case for increased infrastructure spending in Spain and France is less obvious: France has sensibly maintained its infrastructure spending, unlike other countries, and has the best infrastructure in the G7. Spain invested too much in physical infrastructure in the boom years. However, investment in human capital might be a replacement. But both countries have higher youth unemployment than the OECD average, and the quality of vocational and tertiary education for young people who have done poorly at high school in both France and Spain is bad.

In its latest World Economic Outlook, the IMF calculated that the multiplier on debt-financed government investment in developed economies, under the prevailing depressed economic conditions, would be so large that:

- a 1 percentage point of GDP increase in public investment would raise output by 2 per cent in the short term, rising to 3 per cent in the long term, as the supply capacity of the economy expanded;

- and such a stimulus would reduce public debt by 1.6 percentage points for a ‘high efficiency’ investment programme – which means investments that bring in higher taxes – and by 0.6 percentage points for a ‘low efficiency’ one.

This exercise in haggling makes one thing clear: that the eurozone’s fiscal rules have not been abandoned, as some commentators suggest. They may not be followed to the letter, but, unless member-states insist that the rules are abandoned or reformed, a sensible counter-cyclical fiscal policy will not be forthcoming.

There are two ways to reform the rules to make them less pro-cyclical. The first would be to cite the Stability and Growth Pact’s ‘exceptional circumstances’ clause, which allows member-states to breach the 3 per cent limit on budget deficits in “periods of severe economic downturn for the euro area or the EU as a whole.” The current depressed state of the eurozone econmy surely counts as such a period. A more radical option – and therefore one that is more unpalatable for the eurozone’s creditor countries – would be to supplement the existing fiscal rules with a ‘golden rule’, which would allow governments to borrow to invest over the economic cycle. This would remove investment from the eurozone’s fiscal framework altogether. This should have been the case from the start, since, under the current framework, public investment has been slashed more than other forms of spending, despite its high multiplier.

This modest proposal, which is founded in economic theory and evidence, will no doubt be ignored or rebuffed by the austerians, as though it were akin to Jonathan Swift’s proposal three centuries ago (that the problem of an Irish famine could be solved by parents eating their children). The problem is that, unless the eurozone treats ‘lowflation’ as the emergency that it is, debt restructuring will eventually become inevitable. But, unless Germany joins the rest of the eurozone core and the ECB in doing all they can to raise growth and inflation, the effort will fail. This is the tragedy of the eurozone: its member-states are bound together, and can only escape with the help of Berlin, Frankfurt and Brussels. That help is unlikely to be forthcoming. But it does not weaken the case for public investment, as part of a broader attempt to pull the eurozone economy off the rocks.

John Springford is a senior research fellow at the Centre for European Reform.