Turning down the heat on transatlantic tech

The EU and US are adopting different approaches to trade and investment in technology with China. But their mutual mistrust is unwarranted.

The US and EU are trying hard to increase their co-operation on technology and trade matters, including through the Trade and Technology Council (TTC) and dialogues on transatlantic data flows and on subsidies. Having learnt from past fruitless efforts at tech co-operation, the EU and US are keeping their ambitions modest: neither expects full regulatory co-ordination nor many headline-grabbing achievements. Nevertheless, the new relationship has already achieved some significant breakthroughs: for example, the EU and US are closer than ever to restoring seamless flows of personal data.

Ideally, these forums would at least help build trust and encourage the EU and US to keep each other’s interests in mind. But there is still significant mistrust, especially about how to manage trade and investment with China. The EU believes that the Biden administration is using China as a cover for protectionist industrial policy in its Inflation Reduction Act (IRA) and in its technology export controls. And the US is concerned that EU tech regulation unfairly targets US companies and that EU member-states' less restrictive approach to China is opportunistic. Yet the US and the EU overstate the harm the other side’s policies will cause them in the long run. They would both benefit from turning down the heat.

The Inflation Reduction Act

The IRA, which President Biden signed into law in August 2022, provides $490 billion in spending and tax breaks to support green technology, including large subsidies for electric vehicles (EVs). These subsidies are intended to reduce US dependence on China for EV technology. For example, tax credits are only available if minerals and battery components are not sourced from a “foreign entity of concern”. In principle, this objective is sound. China currently produces about 80 per cent of global electric batteries and has more than half of the global market share in processing the minerals essential to these batteries.

But China is not the only loser. For some EV subsidies, a proportion of production must take place in the US or a country with which the US has a free trade agreement (FTA). There is no US-EU FTA: so EV production in Europe will not qualify. President Biden insisted the IRA was not meant to harm America’s partners, saying the FTA requirement “was added by a member of the United States Congress who acknowledges that he just meant allies.” Other lawmakers, however, acknowledge the law is meant to create American jobs, implying that lawmakers simply did not have European interests in mind. The IRA has already led some European car manufacturers to say they will invest in the US in order to receive the subsidies.

America’s Inflation Reduction Act has already led some European car manufacturers to say they will invest in the US in order to receive the subsidies.

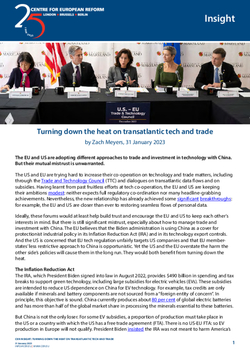

EU leaders are alarmed and are considering whether to respond with their own subsidies. Europe is currently a major exporter of motor vehicles, exporting about half of its total production and generating a €79.5 billion annual trade surplus (about a third of the EU’s total trade surplus). The industry is also a major employer in Europe. It already lost its lead in solar panels because of China’s huge subsidies, and does not want to lose another green industry. As Chart 1 shows, there are glimmers of hope: Europe has recently become a net exporter of EVs and hybrid vehicles. And the US electric vehicle market offers huge growth potential – only 5 per cent of vehicles in the US are electric, far less than in Europe and China.

The US is wrong to argue that Europe is crying “crocodile tears” when it comes to the IRA. It is true that, on EVs, the EU maintains stronger protectionism than the US. Imported electric vehicles face a 10 per cent import tariff. Equivalent US tariffs are only 2.5 per cent. However, Europe’s approach is compliant with international trade laws, because there is no discrimination between imports from different countries (unless they have an FTA with the EU). More importantly, import tariffs like the EU’s promote domestic production to fulfil domestic demand (and stimulate exports only indirectly, by enabling local companies to build scale). Some IRA subsidies, by contrast, promote exports – for example, the IRA subsidises advanced battery manufacturing facilities even if the batteries are not sold in the US but are exported. This suggests the US wants not just to reduce its own reliance on China – an understandable goal, even if that does not necessarily require local production – but also to wrest global leadership of an industry Europe hoped to lead.

Europe’s fears are, nevertheless, almost certainly exaggerated. The EU should take firms’ promises of auto investment in the US with a grain of salt: many may ultimately decide the costs of qualifying for IRA tax credits are too high. To claim credits, an EV manufacturer must remove China from key parts of its battery supply chains. At this stage, most IRA credits are only guaranteed to apply for eight years. Auto firms must therefore act as quickly as they can, even though existing supply chains are already barely coping with increasing demand for EVs. Western car firms are removing China from their supply chains slowly, if at all. Many EV manufacturers may therefore decide the costs and risks of fundamentally changing their supply chains outweigh the sugar hit of a few years of subsidies. For firms which do not already invest in the US, temporary tax credits already seem to make little difference to America’s attractiveness.

Even if firms do qualify, IRA subsidies may not change marginal investment decisions. The EU has only a small share of US car imports today – mostly for luxury cars – and this was never likely to change much. Protectionism, and the high cost of shipping EVs across borders, mean that about 80 per cent of EV sales worldwide are of locally produced vehicles. That suggests any European dreams of exporting huge volumes of EVs to the US, or at least attracting a disproportionate share of EV investment, were always unrealistic. That also illustrates that investment is not a zero-sum game: more green investment in the US does not necessarily mean less green investment in Europe.

Export controls

Europe’s concern about America’s aggressive new tech export controls are also misconceived. Before 2022, the US had already imposed some export controls targeting China’s access to American chips: its long-standing goal was to hold China two generations of chip technology behind the US. After Chinese chip-maker Semiconductor Manufacturing International Corporation (SMIC) achieved a breakthrough, bringing it closer to the technological frontier, Biden rapidly changed tack. Washington now wants to maintain as much of a lead as possible. New US export controls require Washington to approve sales of a greater range of advanced US chips and chip-making equipment – including sales made by companies outside America that use US software and tools.

The Netherlands has, after lengthy negotiations, agreed to strengthen its own export control policies too. Dutch cooperation is crucial because the Netherlands, the US and Japan together provide almost all the world’s chip-making equipment. However, it is unclear whether the Netherlands’ has agreed to “copy the American measures one-to-one”. It has been reluctant to lose sales in the large and growing Chinese market.

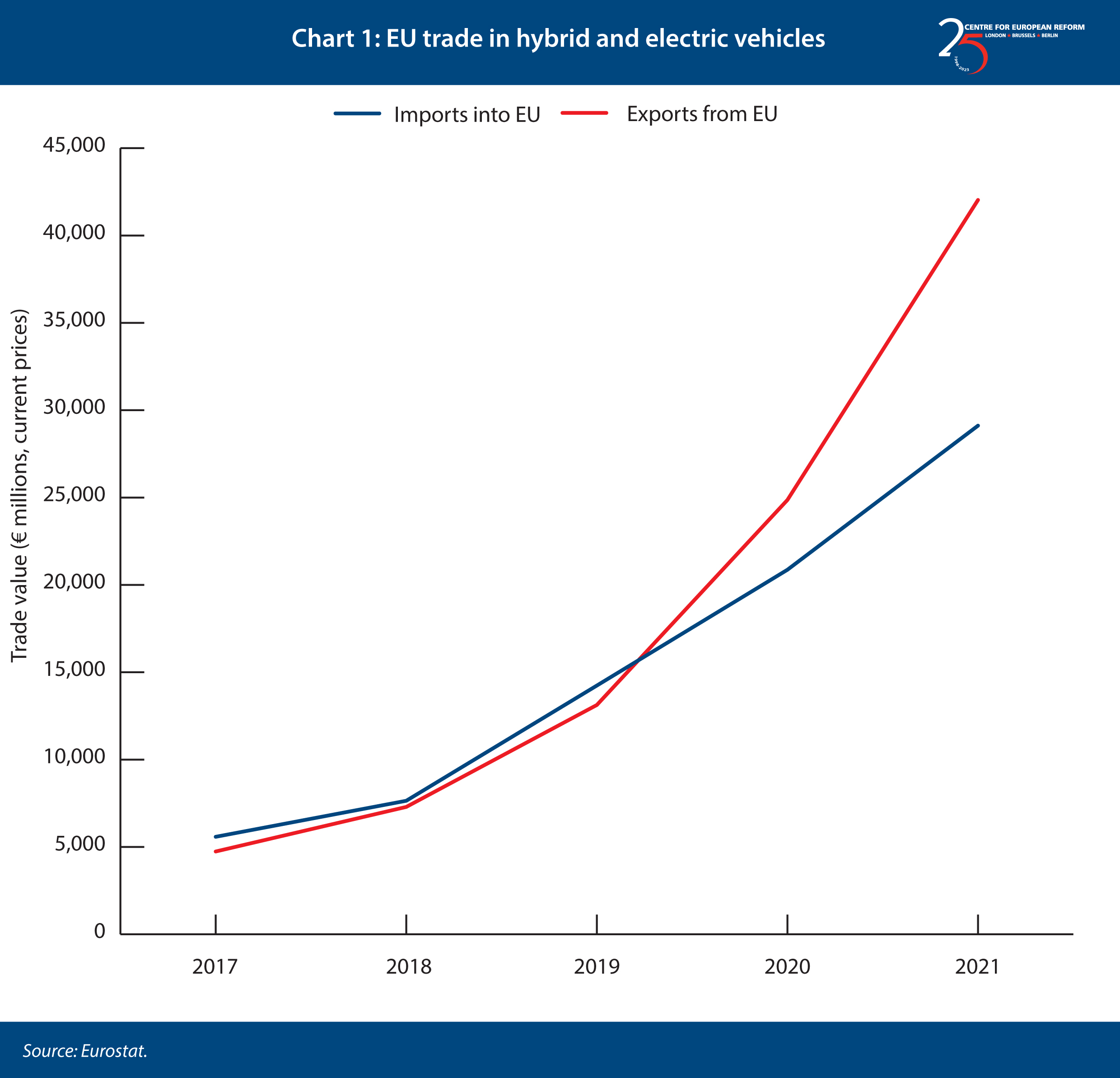

A significant concern in the EU is that US export controls are giving America a leg-up over Europe – for example, because the US insists the Dutch ban high-end chip-making exports while Washington approves the export by American firms of competing equipment. This worry has some basis. Until recently, the West considered Dutch firm ASML’s cutting-edge equipment to be indispensable in building advanced chips and the US pressured the Netherlands to prevent their export. But SMIC has been able to use less-advanced tools to make these chips – tools which American firms produce, and which Washington approved for sale to Chinese customers. Reports that the US had issued licences for more than $100bn of exports to Chinese companies like Huawei have not helped assuage Europe’s worries. More generally, as Chart 2 shows, the leading US and Japanese chip-making equipment firms are more dependent on sales to China than ASML is.

However, the EU should be less concerned that this round of new export controls could throw European industry under the bus.

First, before China’s recent breakthroughs in chip manufacturing, there were legitimate reasons for the US to fret about ASML’s exports. ASML’s machines are far more difficult to replicate than American tools (the US believes foreign equipment firms could remove US software and tools from their supply chains within months, making those firms immune to the current export controls). China’s success in making advanced chips without ASML’s most advanced machines, but with the help of American tools instead, was a genuine surprise. The latest round of US export controls – which damage the US sector even before the Dutch and Japanese have agreed equivalents – will curb the exports of American equipment firms to a far greater extent, proving the US has “skin in the game”.

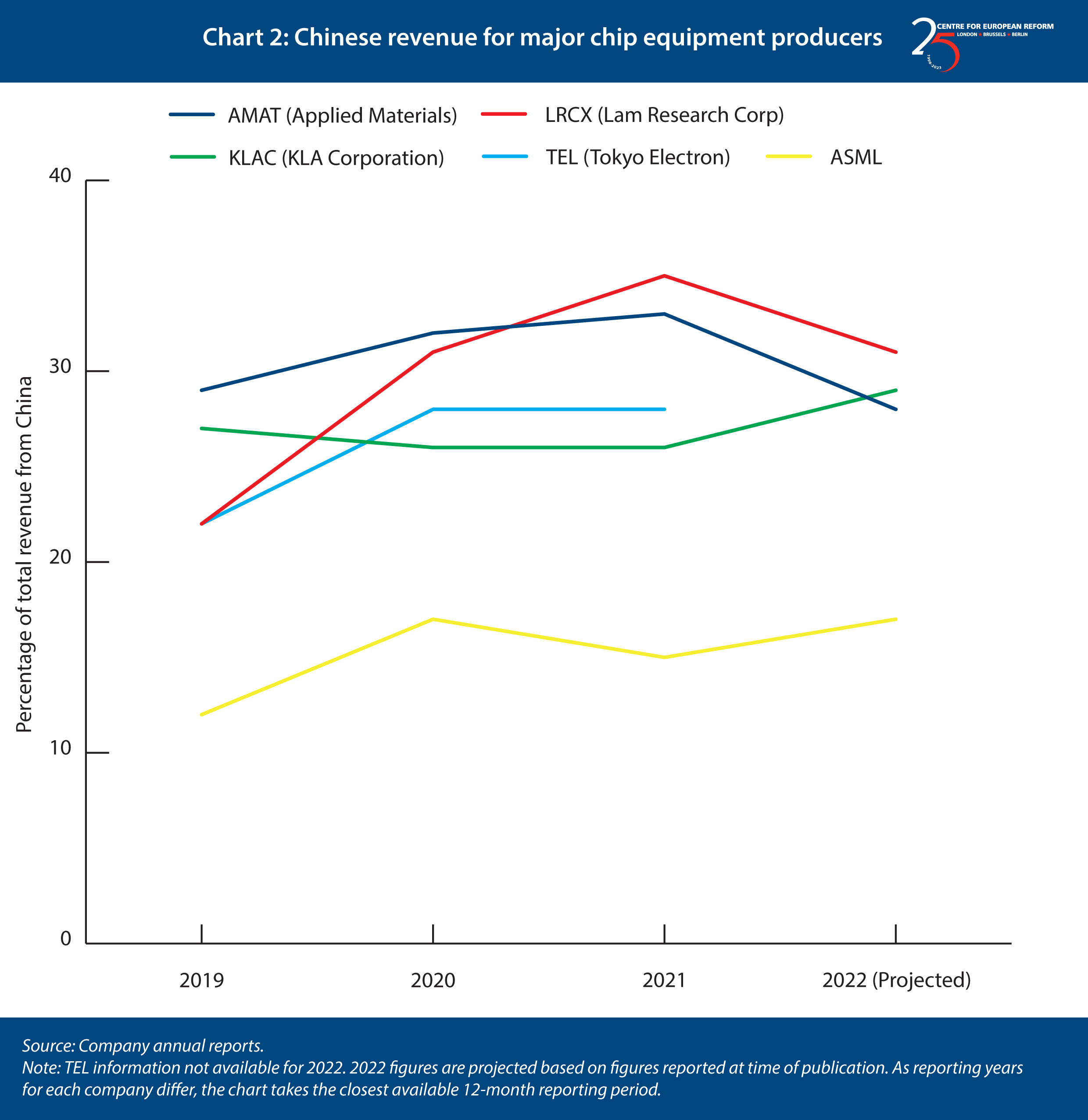

Second, export controls damage chip designers as well as chip-making equipment firms. The US is far stronger than Europe in chip design, so it is wrong to look only at chip-making equipment firms and conclude that the US benefits commercially from its export controls. Intel’s growth in China has flatlined since 2019, for example. And as Chart 3 shows, amidst a broader sell-off, major US chip designers all suffered significant stock price drops in early October 2022 when the export controls were announced. Yet ASML, the largest European chip-making equipment supplier, has rebounded much more strongly than US chip designers.

Finally, tech decoupling from China offers European chip-making equipment suppliers many new opportunities. While it may reduce European firms’ sales in China, decoupling has unleashed a worldwide rush of subsidies for chip manufacturing plants. Those plants will need European chip-making technology, which (despite China’s advances) remains the most efficient and reliable way to produce highly advanced chips. ASML believes this growth in demand will compensate for loss of business in China.

Tech decoupling from China offers European chip-making equipment suppliers many new opportunities.

The EU is right to have questions about America’s lack of transparency in how it issues export licences, and the appropriateness of licences being granted by an agency of the US Department of Commerce, which is supposed to support US economic growth. But America’s policy change is unlikely to give US chip firms sizeable advantages over European firms. The Dutch were right to agree to close co-ordination with the US about which exports are allowed, rather than letting disagreement upset broader co-operation.

American concerns about Europe

On the American side, concerns are also driven by strong emotions, largely focused on the EU’s digital sovereignty agenda. Former US trade representative Susan Schwab complained about what Brussels is “doing to US companies with half a dozen digital acts”. An influential US-aligned think-tank recently warned its readers that “the Europeans are coming”, planning to target American tech firms with more regulation and lawsuits. Such concerns are mostly misplaced. Many European sovereignty initiatives are essential to respond to growing Chinese tech capabilities. Some may even prove mutually beneficial for both sides of the Atlantic.

Initially, Washington’s ire was focused on the Digital Markets Act and Digital Services Act, which some American politicians believed were attempts to hobble US firms. Yet many US politicians now acknowledge that these laws respond to legitimate concerns and are pursuing similar proposals. These initiatives are essential to maintain the West’s technological leadership over China, which was achieved through intense competition and the ability of superstar firms to disrupt existing markets. Yet, today, many Western digital markets are characterised by one or two incumbents. Smaller firms have little chance to build the scale necessary to be viable challengers. This needs to change – otherwise only Chinese players like TikTok will be able to upend the market: they can build scale at home, protected by China’s internet firewall. Furthermore, the US will probably benefit far more than Europe from open and competitive digital markets. It has big tech players who may rise to the challenge of greater competition and it has many more tech start-ups who may replace the big players if they fail. Washington has therefore come to accept that it is short-sighted to protect today’s incumbents simply because they happen to be American.

Without more competition, only Chinese players like TikTok will be able to upend Western digital markets.

Many US commentators also had a knee-jerk reaction to European proposals to regulate emerging technologies like AI, assuming it was technophobic or would hamstring American firms. Now, the US has come to accept Europe’s position that investors will be more willing to invest in AI, and consumers and businesses will be more willing to adopt and use it, if it is trustworthy. Establishing a joint roadmap for trustworthy AI was an important outcome of the most recent Trade and Technology Council summit.

New EU digital legislation – like proposals to limit the transfer of non-personal, so-called industrial data outside the EU – is still causing concern in Washington. Yet these proposals may prove essential to respond to challenges posed by China, such as theft of intellectual property. The EU proposals are non-discriminatory. They require, for example, European firms to be confident of the quality of the destination country’s legal system and protections for industrial data before it can be transferred. This may cause additional trade friction between the US and the EU – but it will mean far greater friction between the EU and China. These proposals upset US firms which seek to avoid increased trade costs, but their objective is one America ought to support to protect the West’s long-term technological leadership over China. While some EU stakeholders certainly want to pursue more overtly discriminatory proposals that will harm EU-US co-operation – such as preventing US cloud computing firms from obtaining security accreditations to drive business to European cloud providers – it is uncertain that these proposals would succeed, and even if they did they would be less economically disruptive than America’s IRA.

Conclusion

Europe and the US are on different trajectories when it comes to decoupling from Chinese tech supply chains. The US approach is more aggressive – relying on huge subsidies, harsh export controls, political pressure on other Western countries to adopt its approach and disregard for international trade law. The EU’s approach is not just mercantilist but tries to foster competitive markets where smaller players have a chance: it may prove more viable in the long term. Splintering technological supply chains is risky while China still dominates certain critical sectors, such as EV battery production. China’s recent chip-making innovations prove that harsher chip export controls may backfire. And sensible tech regulation may prove essential to maintain the West’s innovation lead in the long run.

Whatever the merits of their respective approaches, EU and US co-operation will be essential to tackle the threats posed by China. Yet the degree of EU-US mistrust is unwarranted. The IRA will not prove as catastrophic as Europeans fear; US export controls are not a form of industrial strategy; and European regulation will help maintain the West’s tech leadership. While the EU and US take different approaches to China, frictions in their relationship will continue. But they ought not overshadow the benefits of co-operation.

Zach Meyers is a senior research fellow at the Centre for European Reform.

Add new comment