Should the EU develop 'European champions' to fend off Chinese competition?

China is distorting world trade through its aggressive industrial policy. But fostering ‘European champions’ in order to compete is premature – and risky.

On February 4th the economy ministers of Germany, France, Italy and Poland sent a letter to competition commissioner Margrethe Vestager asking for a review of EU competition policy. They demanded that the European Commission “introduce more justified and reasonable flexibility” to its decisions about mergers between European companies, to “take better account of third countries’ state intervention”. In 2019, the Commission had blocked Siemens’ attempt to buy Alstom, a French train manufacturer, leading France and Germany to raise concerns that China’s state-subsidised manufacturers, including train manufacturer CRRC, have been distorting global competition. Although they have backed down from their original proposal that the European Council should be able to overrule the Commission’s merger decisions, France and Germany want the Commission to allow more tie-ups of manufacturers if they are facing unfairly subsidised competitors from China and elsewhere. But it is unlikely that this policy would work without cross-subsidising European ‘champions’ through higher prices for European customers.

Should the EU develop European champions to compete with China? Not in the way France and Germany suggest.

A growing consensus is emerging in the EU and the US that China is distorting competition globally in two ways. First, the Chinese government is engaging in ‘import substitution’ in its domestic market. China is accused of sheltering domestic companies from competition through ‘buy Chinese’ public procurement policies; enacting licensing requirements that discriminate against foreign companies; requiring foreign companies to transfer technology to Chinese companies in order to build factories there; and granting Chinese firms stronger intellectual property rights than foreign ones. Second, through the state-directed financial system, the government provides cheap capital to Chinese companies in strategic sectors. The Chinese government hopes that it can more rapidly attain technological parity with developed countries through these policies, moving up the manufacturing value chain and developing world-beating companies. And while these policies are a well-trodden path for developing countries, many Europeans believe China’s size and rapid growth makes the need for swift action all the more pressing, especially because the EU retains a large industrial base compared to the US.

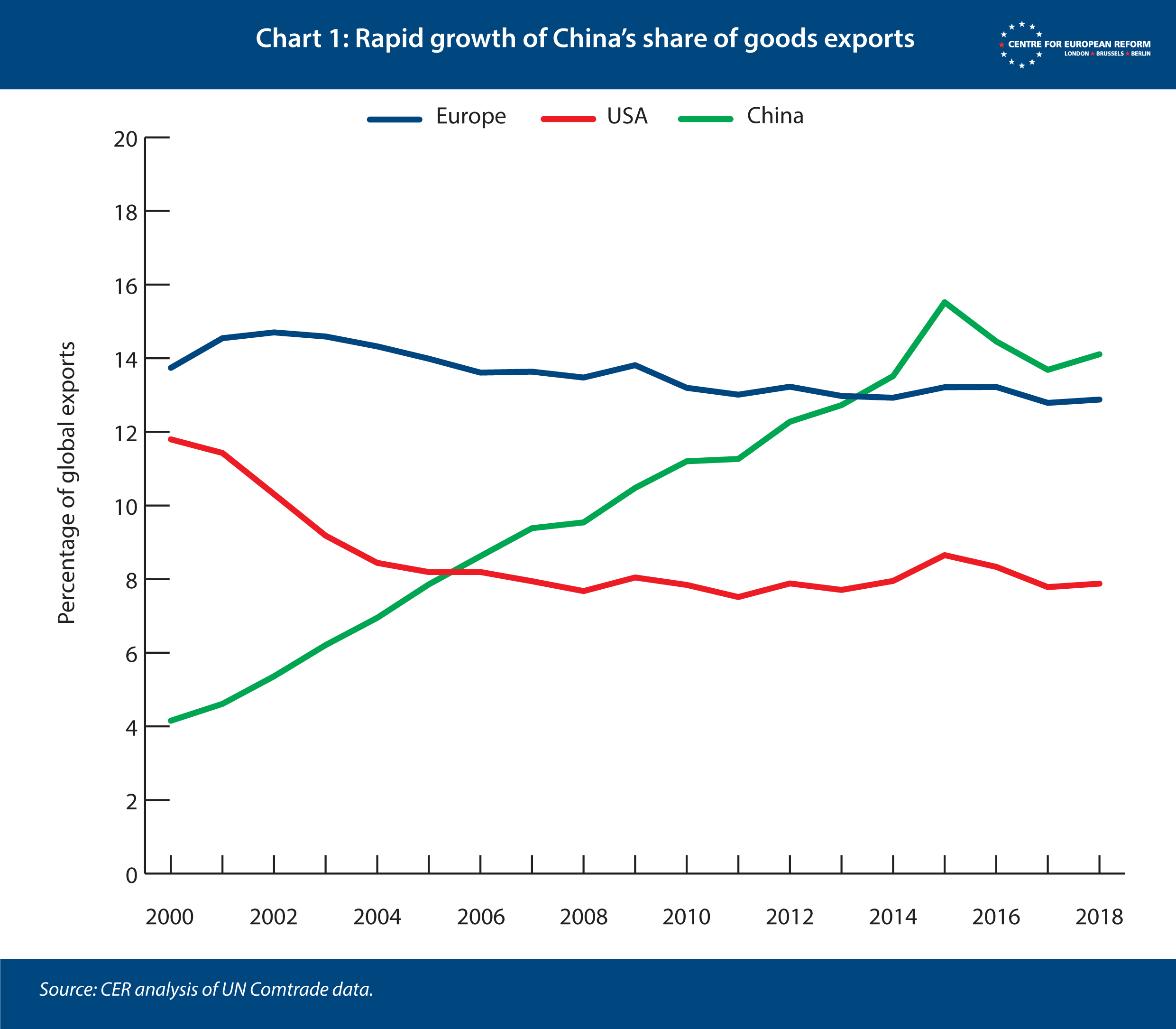

China’s technological prowess has been advancing rapidly, as shown by its high-speed rail network, and investments in science and industrial research and development. China’s share of global goods exports rose very quickly between 2000 and 2015, followed by a marked decline in 2016 and 2017 as the economy stuttered, partly thanks to Donald Trump’s trade war (Chart 1). But that only tells us so much about the degree of Chinese competition EU manufacturers are facing.

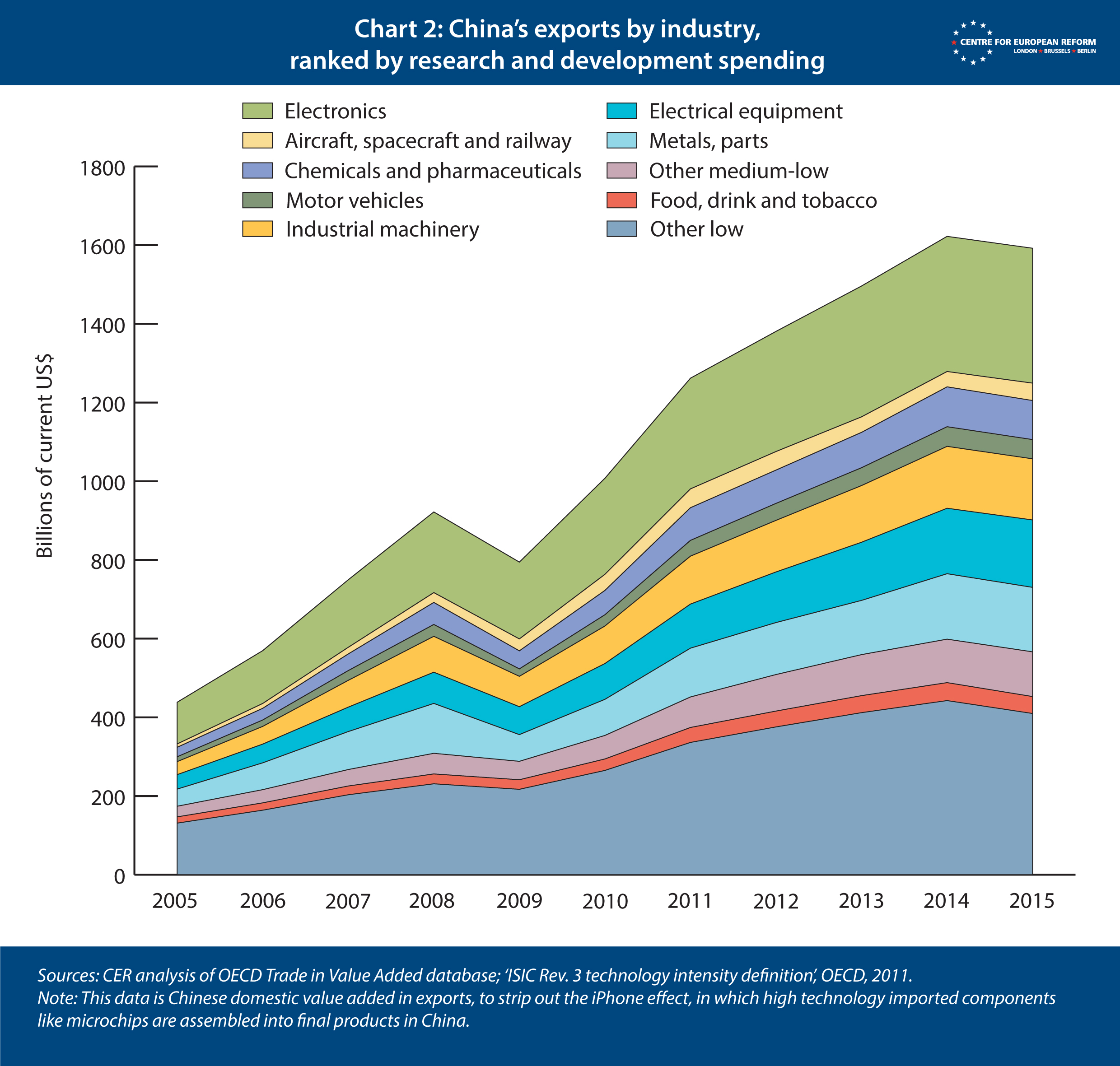

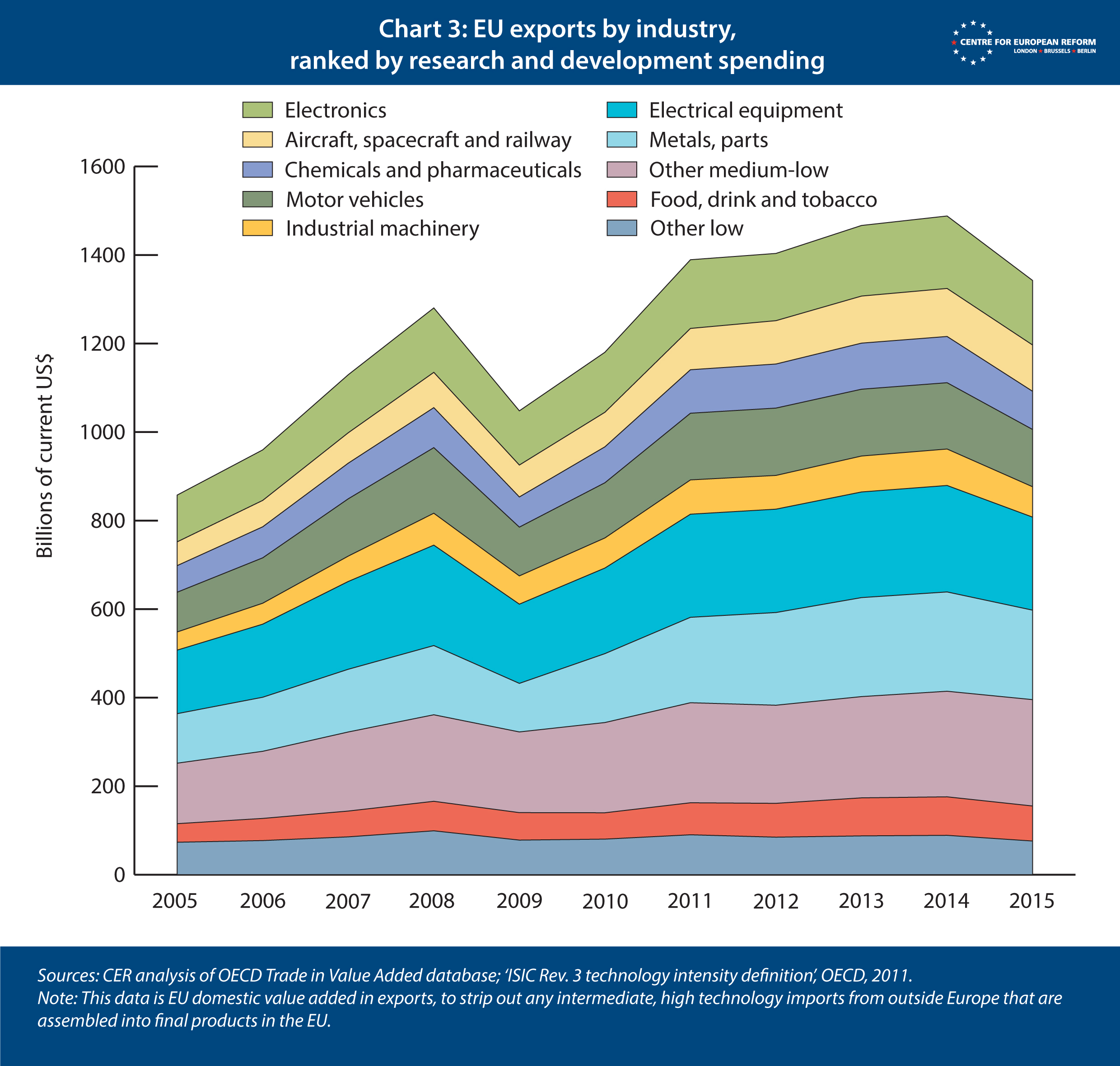

The EU has the world’s most advanced and diversified industrial sector (with Japan a close second). If we compare European and Chinese exports in industries that have been ranked from high to low technology, rather than all exports, the picture is more mixed (Charts 2 and 3). China’s electronics sector grew rapidly between 2005-2015, as has industrial machinery; both sectors have relatively high R&D investment, and the latter is becoming a major competitor to German companies. But China has yet to build a large exporting base in aircraft, trains, chemicals, pharmaceuticals and cars, which make up 45 per cent of the EU’s exports. And China has made slow progress in moving up the value chain: the share of high-technology goods (aside from electronics) in its total exports only grew by about 1 percentage point in that decade, for example.

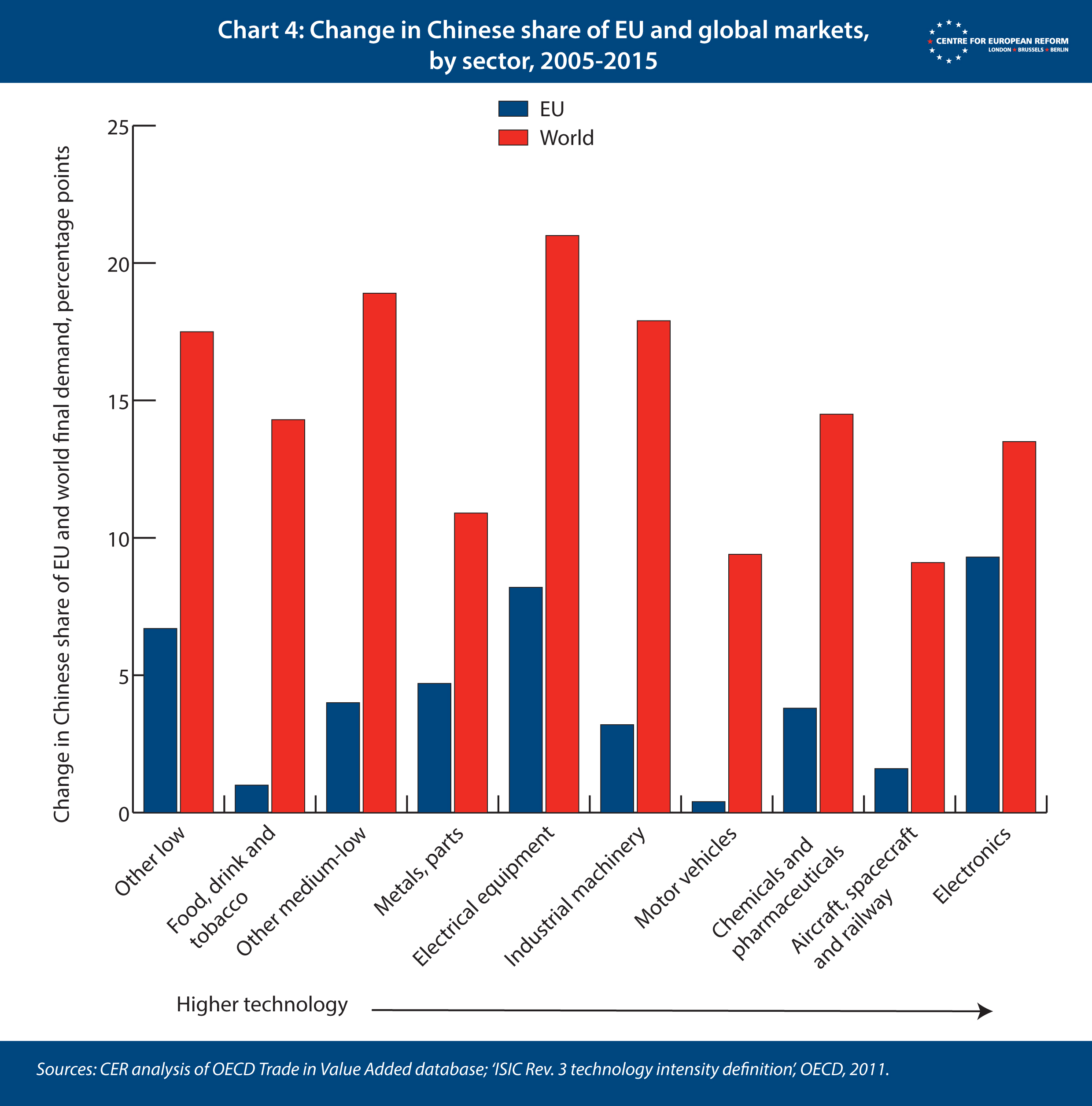

China has found it easier to penetrate high-technology markets outside the EU. And its exporters have performed better in sectors in which the EU is weaker: electronics, electrical equipment and textiles (which is part of ‘Other low’ in Chart 4). They have struggled to dislodge their European competitors in the areas Europe is strong – cars, planes, rail and pharmaceuticals. And the speed of Chinese entry into higher-technology EU markets was no faster than into lower-technology ones. This pattern, in which China has made faster advances into higher technology markets outside the EU than inside it is not altogether surprising: European buyers of high tech manufactured goods are richer and have a greater preference for established brands at the top end of the market.

This analysis suggests that the EU should be cautious about helping create ‘European champions’ to fend off Chinese competition. Chinese companies have so far been less successful in Europe than is commonly thought. And, as I noted last year, dominant companies in high-technology sectors would probably distort competition within Europe. European companies with more domestic market power would raise prices and lower innovation. And there is some evidence that mark-ups (a measure of profitability) have been on the rise in high technology sectors across advanced economies, suggesting that competition has been weakening.

Rather than relaxing domestic competition policy, it makes more sense for the EU to deal with trade distortions by using trade policies. Yet it is obvious that the EU will find it hard to change China’s behaviour. Trump’s strategy – engage in a tariff war in violation of America’s World Trade Organisation (WTO) commitments, in an attempt to force Chinese concessions – is not something that the EU is willing to countenance. That is partly because the EU itself is a multilateral system, with differing interests between its member-states, who would find it impossible to agree how the pain of trade wars should be distributed between them. China remains a large market for German machine tools and other industrial goods. And several southern, central and east European member-states have also received large investments from China, making them unwilling to accept a tougher EU strategy.

The WTO is also a relatively more important institution for EU member-states than for the US, given the larger size of the EU’s industrial base, and the importance of WTO rules for governing global trade in goods. China has refused to agree to reforms to the WTO’s anti-subsidy rules, which are currently relatively light touch: countries may only take defensive measures against subsidised imports if there has been a direct transfer of funds from the state to an exporting company, rather than more hidden forms of aid through the banking system.

There are no easy ways to stop Chinese distorting trade. But weakening competition policy should not be part of the EU’s toolkit.

And the European Commission was surely right to say that China is “a systemic rival promoting alternative models of governance” in its 2019 strategy paper. Now that President Xi Jinping governs the largest economy in the world, it is not surprising that he is seeking to bypass Western multilateral institutions through his Belt and Road Initiative of infrastructure investment, which comes with few of the strings attached to World Bank lending. Xi is also courting 17 southern, central and eastern European countries (which, together with China, make up the ‘17+1’ group), raising concerns China is attempting to sow division within the EU

So what can the EU do? Here are four bases for a strategy.

First, raise investment in R&D. The EU and its member-states could spend more on R&D on early stage technology projects in industries where it is already competitive. Green technology is an obvious place to expand funding: the world will need new forms of renewable energy, construction materials, batteries and energy storage, and digitised, energy efficient household and industrial equipment as climate change starts to bite. The Commission was right to approve state aid in December 2019 for a new consortium of European companies who want to develop the next generation of electric car batteries, as there is a stronger rationale for government aid to early-stage technology than for sectors that are already more mature. The healthcare sector is another promising area for higher R&D support. Many countries across Europe, North America and Asia are ageing rapidly, increasing the demand for new treatments, medical devices and other technologies that will lengthen lifespans and improve healthcare services.

Second, provide alternatives to closer ties with China. The EU could provide more capital for strategic infrastructure, such as ports and railways, to seek to outbid Chinese investment, while maintaining strong oversight to prevent corruption. This could include countries in the EU’s neighbourhood, to provide other options to governments who are being courted by Beijing. And the strategy embodied in the Ukraine-EU association agreement, which offers progressive market opening in exchange for adopting EU rules and standards, could be deployed in other countries in the neighbourhood and elsewhere.

Third, use new investment screening rules effectively. The new rules will come into force in the autumn of this year. While the Commission and Council will have no powers to block foreign direct investment by China or other countries in energy, transport and communications infrastructure, data, or finance, member-states will have to scrutinise these investments in a standardised way, and explain their decision-making in reports to the Commission. The Commission will offer an opinion if an investment poses a risk to more than one member-state, or to common projects such as Gallileo and Horizon 2020. It would be helpful if this dialogue continued about investments that had already been made, rather than simply ending once investments had been approved. f Germany allows Huawei to develop parts of its 5G network, German authorities could share information about any problems that arose thereafter.

Fourth, the EU should undercut China’s arguments about Western hypocrisy. If the EU is serious about tackling veiled Chinese subsidies and safeguarding the WTO, it could offer to put its own subsidies on the table to hold out the prospect of a bargain with China and the US. The EU could propose that China opens its domestic market and reduces subsidised lending and discriminatory regulation in return for the US and EU curbing subsidies to farmers and aircraft manufacturers. The politics of such a deal would obviously be very difficult, but raising it would undermine China’s (not unreasonable) argument that they are not the only side that is preventing reform of the WTO’s rules.

Building ‘European champions’ carries with it considerable risks for European consumers. China is some way from becoming a significant player in European markets for high-technology goods. And any industrial strategy that simply transfers power from Chinese companies to European ones is unlikely, ultimately, to raise the EU’s competitiveness, as incentives to innovate will be weaker if the EU relaxes its merger regime. The EU would do better to tackle distorting Chinese policies using trade and investment defences, however slow and frustrating that may be – while directing aid to early-stage ventures that may turn into the world-beating products in the future.

John Springford is deputy director of the Centre for European Reform.

Add new comment